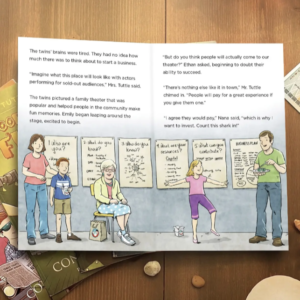

Do your kids complain whenever they have to go with you to the grocery store? What if you could transform a weekly chore into regular special moments with your kids? Any parent can do this. It’s so easy! In fact, Tom from Atlanta, Georgia did created a moment with his nine-year-old son without even trying.

His son had a light-bulb moment while standing in front of all the chips. He told his father that he suddenly understood why there are 15 kinds of potato chips, correctly recalling the term “spontaneous order” from the Tuttle Twins books. And just like that, Tom realized that everything he’d been reading to his son had been sinking in!

PHOTO: Tuttle Twins

Start with Books

You can be part of the growing movement of parents like Tom who are learning how to teach kids about money while their children are still young. Doing this is as easy as finding the right books. The Tuttle Twins series includes books that teach kids about inflation, central banking and the Federal Reserve, the economic system, entrepreneurship, and much more.

Books will help you lay the foundation you need as you learn how to teach kids about money. That’s right. Teaching kids free market economics is a snap! And the basis of understanding finance lies in realizing how the economic system works, something many kids wouldn’t normally be exposed to until high school.

Books that teach kids about inflation and the free market are essential for laying the groundwork for understanding the real world. The Tuttle Twins books break down these complex topics into easy-to-understand ideas in an exciting, engaging way that will help them retain what they learn. All the books in the Tuttle Twins series transform learning into a fun adventure through a magical journey of discovery, both for the twins and for readers!

PHOTO: Tuttle Twins

Heading to the Grocery Store

The next step in teaching your kids free market economics is to take them to the grocery store. You may face some whining at first, but once you start explaining how what they’re reading in the Tuttle Twins books and other titles like them, your kids will quickly start paying attention. While at the grocery store, ask them questions like:

- If you could buy just three items today, which ones do you actually need to stay alive and which are wants that would simply be nice to get?

- When we pay for our items, why are both we and the cashier happy with the trade?

- If there aren’t many boxes of your favorite cereal left on the shelf, but it’s a very popular cereal, what do you think will happen to the price?

- Why do you think watermelon is cheaper and easier to buy in the summer but more expensive during the winter?

- Why do you think better-tasting products or more-attractive packaging is important for sales?

- Where would you choose to shop if two stores sell the same brand of milk, but one store charges $5 and the other only charges $3.50?

- How do you decide whether to purchase a less expensive brand of a product and save the rest of our money or buy the more expensive brand?

- How many people had to work to get a single box of cereal to the store shelf?

Your kids will always remember when their mom or dad took them to the grocery store and took the time to ask them questions like these. Grocery store trips don’t have to be nothing but a chore. They can become the times your kids remember the most when they get older!

Image credit: Unsplash

Many people have a lot of their money tied up in things they rarely think about. Beyond your home or investments, you might own unique items with a lot of hidden value. Things like family heirlooms, collectibles, old electronics, or classic cars can all be turned into cash if you know how to figure out what they’re worth and where to sell them.

This guide will show you how to find, value, and sell your unique assets to unlock their financial potential.

Identifying Hidden Value

First, make a list of everything you own. Look past everyday items and think about things that might appeal to a specific group or have historical importance. This could be anything from rare comic books in your attic to a piece of art you inherited. Many assets have value that isn’t obvious, even things we don’t think of as physical property.

Some collectibles and specialty items can even become great investments when they are rare, well-preserved, and in strong demand.

Consider these types of items:

- Collectibles: Stamps, coins, trading cards, and memorabilia.

- Vintage Items: Classic cars, antique furniture, retro clothing, and old electronics.

- Art and Jewelry: Paintings, sculptures, and fine jewelry.

- Intellectual Property: Royalties from a book, song, or patent.

To understand the potential of these items, you need to look at them not just for sentimental reasons but for their market value. Different intangible asset valuation methods can help you start to understand what something might be worth, even if you can’t physically hold it.

Specialized Valuation Methods

Unlike stocks or real estate, unique assets don’t have a simple, fixed price. Their value depends on how rare they are, their condition, how much demand there is for them, and their provenance. Getting an accurate appraisal almost always means you need a specialist. For example, an appraiser for fine art uses different standards than someone who values vintage watches.

The same goes for classic cars. A regular mechanic can’t give you an accurate market price for a collector’s vehicle. Getting an expert Porsche valuation, for instance, requires deep knowledge of specific model years, how well a car has been restored, and current auction trends. For any high-value item, find a certified appraiser or a reputable dealer who specializes in that exact category. They can give you a formal appraisal document, which is important for insurance and for selling the item.

Connecting with Buyers

Once you have a reliable valuation, the next step is finding the right buyer. The best place to sell depends entirely on the asset. General marketplaces like eBay might work for lower-value collectibles, but they aren’t ideal for high-end items where trust and security are key.

For more valuable assets, think about these options:

- Auction Houses: Places like Sotheby’s or Heritage Auctions serve serious collectors and can often get the highest prices for rare items.

- Specialized Dealers: Businesses that focus on a specific niche, such as antique furniture stores or classic car buyers, already have a network of interested clients.

- Consignment Shops: A good choice for designer clothing, jewelry, and high-end accessories. The shop handles the sale and takes a percentage of the final price.

- Online Marketplaces: Niche websites for specific collectibles, like Reverb for musical instruments or Chrono24 for watches, connect you directly with enthusiasts.

Navigating the Sales Process

Selling a unique, high-value asset involves more than just agreeing on a price. A smooth and secure transaction needs careful planning and paperwork. First, gather all relevant documents, including the appraisal, certificates of authenticity, and any maintenance or history records. High-quality photos from different angles are also essential.

When you find a potential buyer, be ready to negotiate. Use your formal appraisal as a starting point and be clear about the lowest price you’ll accept. For the transaction itself, always use a secure payment method. For very large amounts, an escrow service protects both you and the buyer by holding the money until the item has been delivered and checked. Finally, figure out how the item will be shipped or delivered. For fragile or large items, professional packing and insured shipping are a must.

Taking the time to properly value and market your unique assets can give you a surprising financial boost. It all starts with recognizing the potential value sitting in your own home.

Baggage problems can turn a well-planned journey into a stressful experience, especially when essentials are missing after landing. Many travellers assume the airline will take care of every loss, delay, or damage issue.

However, airline compensation and baggage claims under insurance work differently. Understanding this difference helps travellers know whom to approach, what documents to keep, and how to make a smoother claim after an unexpected baggage issue.

What Is Airline Compensation for Baggage Loss or Delay?

Airline compensation is the amount an airline may pay when checked-in baggage is lost, delayed, or damaged while under its responsibility. The process usually begins with reporting the issue at the airport and getting written acknowledgement from the airline.

Situations Covered by Airlines

Airlines generally handle baggage concerns that occur after check-in and before the bag is returned to the passenger. This support depends on the airline’s policy, route, ticket conditions, and applicable aviation rules.

Common situations may include:

- Checked-in baggage not arriving at the destination

- Baggage reaching later than the passenger

- Damage caused while the bag was in airline custody

- Missing contents reported as per airline procedure

- Reasonable essential expenses during baggage delay

Compensation Limits Imposed by Airlines

If your checked baggage is delayed, damaged, or lost during a trip, the airline’s compensation may not always cover the full inconvenience or additional expenses you face. This is where travel insurance may offer wider support, subject to the policy terms, coverage limits, and claim approval.

Airline limits may consider:

- Whether the baggage is delayed, lost, or damaged

- Depreciated value of belongings

- Receipts or purchase proof

- Restricted categories under airline rules

- Claim timelines mentioned by the airline

Rules Governing Airline Liability

Domestic and international flights may follow different standards. For overseas travel, international conventions and airline conditions of carriage can influence how compensation is assessed.

Key factors include:

- Route and destination

- Airline terms and conditions

- Type of baggage issue reported

- Proof submitted by the traveller

- Time taken to report the concern

What Is a Baggage Claim under Travel Insurance?

A baggage claim under travel insurance is a request made to the insurer for covered baggage-related losses during a trip. It may apply when baggage is delayed, lost, or damaged, depending on the plan chosen and the policy wording.

Coverage for Lost, Delayed, or Damaged Baggage

If you are travelling to the USA with checked luggage, even a short baggage delay can affect your plans, especially when essentials are not immediately available. While choosing travel insurance for the USA, check whether the policy includes baggage delay, baggage loss, or baggage damage benefits, along with the claim limits and required documents.

Coverage may include:

- Loss of checked-in baggage

- Delay in receiving checked-in baggage

- Damage to covered baggage

- Reimbursement for approved essential purchases

- Support based on the policy schedule

Additional Protection beyond Airline Responsibility

Airline compensation focuses mainly on the airline’s responsibility. Insurance, on the other hand, may provide broader trip-related protection.

Insurance may offer added support for:

- Trip-related inconvenience caused by baggage delay

- Covered purchases made during the waiting period

- Documentation-based reimbursement

- Assistance during international travel

- Claims handled as per policy terms

Policy Terms and Coverage Limits

Every travel insurance policy has defined benefits, limits, conditions, and claim requirements. A traveller should not assume that every baggage issue will be treated the same way.

Important points to review include:

- Covered baggage benefits

- Claim limits for each benefit

- Required documents

- Reporting timelines

- Terms linked to unattended items or valuables

Key Differences Between Baggage Claims and Airline Compensation

Both options help travellers deal with baggage issues, but they differ in payer, scope, limits, documents, and settlement process.

Who Pays the Compensation?

Airline compensation is paid by the airline when the baggage issue falls under its responsibility. The insurer pays a baggage claim under insurance after reviewing the claim against the policy terms. In some cases, both processes may be relevant, but they remain separate.

Difference in Coverage Scope

Airlines usually focus on baggage handled during air travel. Insurance may consider wider travel-related situations covered under the policy. This is why travellers should review both airline rules and insurance benefits before starting an international trip.

Variation in Claim Limits

Airline liability usually follows defined limits and may not reflect the complete inconvenience faced by the traveller. Insurance claim limits depend on the plan selected. A policy with suitable baggage benefits can help travellers prepare better, provided the claim meets policy conditions.

Documentation Requirements

Airlines usually ask for a baggage report, baggage tag, ticket details, and proof of loss or expenses. Insurers may ask for these along with a claim form, identity proof, boarding pass, receipts, and airline communication. Keeping documents organised improves clarity during assessment.

Time Taken for Settlement

Airline resolution may depend on tracing the bag, reviewing responsibility, and verifying supporting documents. Insurance settlement may depend on claim submission, document review, and policy terms. Travellers should report the issue quickly and follow the required process to avoid unnecessary delays.

Conclusion

Airline compensation and baggage claims under insurance serve different purposes. Airlines address baggage issues linked to their handling responsibility, while insurance may support travellers through covered benefits under the chosen policy. For Indian travellers going abroad, understanding both processes can reduce confusion during stressful moments. The practical approach is simple: report the issue immediately, collect documents, read the policy wording, and submit claims with complete information.

Image Credit: Unsplash

When a financial emergency hits, most people immediately think of using a credit card or getting a personal loan. These can give you quick cash, but they often cost a lot in the long run. The good news is you have many other ways to get financial help without getting stuck with high-interest debt. Looking into options like community support or direct negotiation can protect your financial future while solving your immediate problem.

The Traps of High-Interest Debt

High-interest debt, like credit cards and payday loans, can quickly become a huge burden. The main issue is how interest builds up, making it hard to pay off the original amount you borrowed. Many people find their monthly payments barely cover the interest, while the main debt stays high. This often leads to what experts call the debt trap cycle.

Imagine you have a $2,000 emergency car repair and put it on a credit card with a 24% annual percentage rate (APR). If you only make the minimum payment, it could take years and cost thousands in interest to pay off just that one expense. The quick relief of fixing your car is then replaced by the constant stress of growing debt.

This cycle can really hurt your overall financial health. It can affect your credit score, your ability to save, and your mental well-being. Understanding this risk is the first step to finding better solutions. Learning how to escape the debt spiral means realizing that borrowing isn’t the only answer when you’re in a tough spot.

Exploring Debt-Free Alternatives

Before you borrow, take time to look for debt-free ways to get money. You might be surprised by how many programs are out there to help during hard times. These options won’t add to your financial stress and are made for people facing temporary difficulties.

- Government Assistance Programs: Federal, state, and local governments offer many support services. Programs like the Low Income Home Energy Assistance Program (LIHEAP) can help with utility bills, and the Supplemental Nutrition Assistance Program (SNAP) can help with groceries. You can often find a full list of available aid on your state’s Department of Health and Human Services website.

- Non-Profit and Charitable Organizations: Many non-profits and local charities offer emergency financial help. Groups like The Salvation Army, Catholic Charities, and local community action agencies often have funds to help people with rent, medical bills, or other essential costs. A quick search for “emergency financial assistance” in your area can bring up many options.

- Generating Quick Income: Don’t forget about what you already have. Selling things you no longer need on sites like Facebook Marketplace or Poshmark can get you cash fast. You could also try a temporary side job, such as pet-sitting, delivering food, or freelance work related to your skills. While this isn’t outside help, it lets you solve the problem yourself without taking on debt.

Leveraging Community Support

Sometimes, your community is your most powerful resource. Friends, family, and even strangers are often willing to help when they understand your situation. In today’s digital world, it’s easier than ever to ask your network for support through crowdfunding. This lets many people contribute small amounts that together solve a bigger financial problem.

Crowdfunding works especially well for specific, one-time needs, like unexpected medical bills, emergency home repairs after a storm, or covering income gaps after losing a job. The key to a successful campaign is being open and honest. Clearly explaining your situation, what the money is for, and how it will help build trust with potential donors. Many people find it easier to ask for help this way than face-to-face. For those in a crisis, a practical step is to start an online fundraiser and let their community help.

Unlike a loan, money raised through community support doesn’t need to be paid back. This means you can handle your immediate financial need without creating future debt. It’s a method built on goodwill and strengthens community ties by letting people support each other in meaningful ways.

Negotiating Payment Plans Effectively

If you have a big bill from a hospital, a utility company, or even your landlord, don’t assume you have to pay the full amount. Many organizations have hardship programs and are open to setting up a payment plan that fits your budget. The important thing is to be proactive and talk to them before your account becomes overdue.

When you call, be ready to discuss your situation calmly and honestly. You don’t need to share every detail, but a simple explanation like, “I’ve had an unexpected loss of income and am having trouble paying the full amount right now,” can open the door to a solution. Instead of just saying you can’t pay, suggest a plan. For example, you could ask, “Would it be possible to pay $100 a month for the next six months to catch up?”

Here are some tips for a successful negotiation:

- Call Before the Due Date: This shows you’re acting in good faith and gives you more options.

- Be Polite and Patient: The person on the phone is more likely to help if you stay courteous.

- Know Your Numbers: Understand what you can realistically afford to pay each month.

- Get it in Writing: Once you agree on a new plan, ask for an email or letter confirming the terms. This protects you from future misunderstandings.

Negotiating directly with creditors is a powerful way to get out of debt or avoid it completely. These arrangements often don’t charge interest and are one of the most effective ways to pay off debt faster because every dollar goes toward the main debt.

Facing a financial shortage is stressful, but it doesn’t have to lead to long-term debt. Taking time to explore alternatives, ask for support, and communicate with creditors can help you manage the situation without adding financial strain. Every challenge is different, but making informed decisions now can protect your finances, reduce stress, and give you a stronger foundation for the future.

Image credit: Unsplash

When you run a service business, your profits depend directly on the value you offer and how efficiently you operate. While getting more clients is always good, real financial success comes from truly understanding your business model. This means setting the right prices, keeping costs down, and making sure your quality of work keeps clients coming back. Making your service business more profitable isn’t about chasing every new lead; it’s about making your core processes stronger.

Understanding Your Service Value

The first step to earning more is to clearly define and price what your service is worth. Many business owners charge too little because they’re afraid of losing customers. But your pricing should cover not just the time you spend, but also your expertise, convenience, and the results you deliver. Add up all your direct and indirect costs, include your desired profit, and see what competitors are charging. Don’t just try to be the cheapest. Instead, explain clearly why your service is valuable enough to justify your rates. If your service is better and more reliable, clients are often willing to pay more for it.

Optimizing Operational Costs

Profit isn’t just what you make; it’s also what you manage to keep. Tracking and controlling your operating costs is crucial for increasing your profit margins. Regularly reviewing expenses, from supplies and transport to software subscriptions and marketing, is a key part of managing your business finances well. It helps you spot where money is being wasted, which costs can be reduced, and which expenses are actually helping the business grow.

For instance, a landscaping company could plan its daily routes better to save on fuel, or a consulting firm might switch to cheaper project management software. Small, consistent savings add up over time and directly boost your profits.

Quality Control as a Profit Driver

In a service business, mistakes cost a lot. They lead to rework, wasted materials, and damage to your reputation. A strong quality control system isn’t just an expense; it actually drives profit. By making your service delivery consistent, you ensure quality and reduce errors. This is especially important for businesses with many employees or teams, like cleaning services, maintenance crews, or field technicians.

For example, using a detailed checklist on a janitorial app for property inspections makes sure every task is done to the same standard each time. This proactive approach prevents client complaints and avoids the expensive process of fixing problems later.

Client Satisfaction and Retention

Happy clients mean more profit. It can cost five times more to get a new customer than to keep an existing one. High-quality service directly leads to happier clients, which then improves retention rates. When clients trust you to do the job right every time, they’re more likely to sign long-term contracts, refer others, and be less concerned about price increases. Make it easy for clients to give feedback and act on their suggestions. This not only helps you improve your service but also shows them you value their partnership, strengthening the relationship and their loyalty.

Leveraging Technology for Growth

Modern technology offers powerful tools to streamline operations and help your business grow. Beyond quality control, technology can automate administrative tasks, improve communication, and expand your marketing reach. Customer Relationship Management (CRM) systems help you track interactions with clients and potential clients, while scheduling software can optimize your team’s time. These tools free you up to focus on high-value activities that directly bring in revenue.

Ultimately, building a more profitable service business is about constantly improving. Start by focusing on one area, whether it’s tightening your budget or using a new quality checklist, and build from there.

As global investing and international banking evolve, GIFT City has emerged as a key financial hub for Non-Resident Indians. A gift city account allows NRIs to use international banking services while being connected to India’s financial ecosystem.

Understanding how this account works, along with its features and benefits, can help NRIs make more informed decisions about managing global income.

What is a GIFT City account?

A gift city account is a foreign currency savings account offered through India’s International Financial Services Centre (IFSC) at GIFT City. It allows NRIs to hold, manage, and transact in prominent foreign currencies such as USD, EUR, GBP without converting funds into Indian rupees. This sets it apart from traditional NRE/NRO accounts, which need to be maintained in Indian rupees.

Key features of a GIFT City account

The GIFT account offered by IDFC FIRST Bank is known as First Global Savings account and it comes with a range of features designed for global banking needs:

| Feature | Details |

| Foreign currency holding | Maintain funds in USDEUR & GBP without conversion |

| Competitive interest rates | Earn interest in foreign currency(e.g. approx. 4.50% on USD Savings account) |

| Interest credits | Interest is credited monthly |

| Freely repatriable funds | Transfer money abroad without restrictions |

| Zero-fee banking | No account maintenance charges |

| No minimum balance | Zero average monthly balance requirement |

| Tax advantages | Interest earned is presently not taxable in India |

| Multicurrency support | Supports major global currencies like USD , EUR, GBP |

| Single app access | Manage NRI and GIFT City accounts in one app |

| Fully digital experience | Open foreign currency fixed deposit online by debiting your First Global Savings account |

These features position the GIFT city account as a global banking solution as opposed to a traditional savings account.

Benefits of opening a GIFT City account

Beyond just features, a gift city account provides some really useful benefits for NRIs, making things more convenient and straightforward.

- Global banking from India: Access international financial services

- Better returns on foreign currency: Interest rates may be more competitive compared to some international banks.

- No currency conversion loss: Funds remain in foreign currency, avoiding exchange rate fluctuations.

- Tax efficiency: Interest earned would be tax-exempt in India

Seamless international transfers: Send money globally with facility of transferring funds abroad via mobile app. These benefits make it particularly useful for NRIs who earn and invest internationally.

How can an NRI open a GIFT City account with IDFC FIRST Bank?

You can open a GIFT City savings account by logging into your IDFC Bank Mobile banking application* or by contacting your dedicated relationship manager assigned to your NRE/NRO Account.

What NRIs should know before opening

Before opening a Gift City account, it is useful to consider the following:

- It is available only to eligible non-residents and overseas citizens of India

- Funds are maintained in foreign currency, not INR

- Tax treatment may differ based in your country of residence

Understanding these aspects helps in using the account effectively.

Why GIFT City accounts are gaining importance

A Gift City account provides a welcoming step towards global banking for NRIs. It offers the convenience of foreign currency access, tax benefits, and easy digital management, helping to smoothly connect the domestic and international financial worlds. As GIFT City continues to expand, these accounts are becoming increasingly important for NRIs to manage, invest in, and build their wealth worldwide.

Choosing a family health plan without first studying medical needs can turn a sensible purchase into a stressful decision later. Every household has different routines, health histories, medicines, preferred doctors, and future expectations.

A plan that looks suitable on paper may feel limited during actual use. Before buying health insurance, families should slow down, compare details, and match coverage with real healthcare habits rather than assumptions.

Why Understanding Family Medical Needs Matters

Family medical needs are not limited to hospitalisation. They include regular consultations, diagnostic tests, maternity planning, child care, senior care, ongoing medication, and preventive check-ups. A thoughtful review helps you choose coverage that supports everyday realities, not only rare emergencies.

- List existing conditions and regular prescriptions.

- Note how often family members visit doctors.

- Consider age, lifestyle, and family health history.

- Review whether dependants need specialised care.

- Think about preferred hospitals and treating doctors.

Financial Costs of Choosing the Wrong Plan

A poorly matched plan may lead to avoidable strain through higher personal payments, repeated reimbursements, or benefits that do not fit actual usage.

Higher Out-of-Pocket Expenses

Out-of-pocket expenses can rise when the plan structure does not match how your family seeks care. Frequent consultations, recurring tests, or specialist visits may feel manageable individually, but together they can affect the household budget. Families reviewing broader protection may also consider critical illness insurance for serious diagnosed conditions, subject to policy terms.

- Review what you may need to pay yourself.

- Check limits linked to hospital rooms or procedures.

- Understand how deductibles affect claims.

- Compare benefits with your usual medical spending pattern.

Unexpected Medical Bills

Unexpected bills often appear when families assume every medical situation will be handled in the same way. Coverage terms can differ for daycare procedures, pre-hospitalisation tests, post-hospitalisation care, ambulance services, home care, and specific treatments. Reading the policy wording may not be exciting, but it can prevent confusion during stressful moments.

- Check which services are included under the plan.

- Review claim processes before treatment is needed.

- Keep records of consultations, prescriptions, and reports.

- Ask clear questions when a term seems unclear.

Insufficient Coverage Limits

Some plans may look adequate at purchase, yet feel restrictive when multiple family members need care within the same year. Coverage limits, sub-limits, and disease-specific conditions can influence how useful a plan feels during treatment. Families should look at the overall protection amount, not just the premium, while keeping affordability in mind.

- Look at the sum insured in relation to family size.

- Check whether limits apply to specific treatments.

- Review restoration or recharge benefits carefully.

- Consider future medical needs, not only current comfort.

How to Assess Your Family’s Medical Needs before Choosing a Plan

Assessment should be practical and honest. Start with current health realities, then consider what may reasonably arise over the next few years.

Review Current Health Conditions

Write down diagnosed conditions, regular medicines, allergies, previous surgeries, and ongoing therapies for every family member. This helps you compare waiting periods, coverage terms, and claim requirements with more clarity. It also reduces the chance of overlooking health details during proposal submission.

Consider Expected Healthcare Needs

Families should think about planned treatments, maternity expectations, children’s health needs, dental or vision-related concerns, and care for ageing parents. These needs may differ across life stages, so the plan should suit both present responsibilities and likely future healthcare use.

Evaluate Healthcare Usage Patterns

Look at how often your family consults doctors, undergoes tests, buys medicines, or visits hospitals. A family with frequent outpatient needs may value different features than one that mainly wants protection for hospitalisation. Usage patterns make comparison more realistic.

Compare Coverage Features Carefully

Do not compare plans only by premium. Review inclusions, waiting periods, claim support, cashless options, renewal conditions, add-ons, and wellness benefits. A balanced comparison helps you see whether the policy design suits your family’s medical priorities and comfort level.

Check Provider Networks

A useful plan should give access to hospitals and healthcare providers that your family can realistically visit. Check whether preferred hospitals are in the cashless network, especially near your home, workplace, children’s school, or parents’ residence. Convenience matters during urgent situations.

Conclusion

Choosing a health plan before understanding your family’s medical needs can affect both care and finances. The right approach begins with a careful review of conditions, habits, preferred providers, and expected requirements. Families that compare plans with these details in mind usually make more confident decisions. Insurance should support real life, not just look suitable on paper, so take time to assess before you choose.

If you feel as though your life isn’t quite where it should be, or if you know that you are struggling to deal with things regularly, then it may be time for you to start practicing some self-care. This guide will help you to do just that, so you can get things back on track in no time at all.

Source: Pexels

Get in Shape

One of the main things you can do is try to get in shape. Strong bodies and strong minds often go hand-in-hand, so make sure that you forget about how your gym routine is making you stressed and how it’s something extra to have in your day, and instead focus on how it makes you feel when you have done it. If you can do this then you will find it easier to not only make sure that you’re dedicated, but also making sure that you are reminding yourself that you are capable of way more than you once were. Fitness isn’t about doing push-ups; many people find it to be a way to reclaim their power, and this is great to say the least.

Get out a Bit

Sometimes you may feel as though you need to get out of town for a little bit. If this is the case, then try to make sure that you take a day, or even a week, and escape your usual town. If you can do this, then you may find that there is a whole world of things to explore, right on your doorstep. Sometimes a change in scenery helps you to breed a change in mindset, and being away from home gives you the chance to feel a bit of tranquility, but on your own terms. You may also find that it breaks the cycle that you are in, which is a good way for you to start feeling like you are able to enjoy yourself once more.

Take Control of Your Story

Taking control of your story is one of the best things you can do. The past is simply a story that you will repeat time and time to yourself. If you can take the time to understand it, then you may find that it is very liberating. Visit a therapist who can help you to reframe the experience you have had or even take the time to journal it, as this is a good way for you to gain a better understanding of what has happened to you. If you can learn to pinpoint the opportunities you have for growth, then this will help you in more ways than one.

Invite New People

Sometimes, inviting some new people into your life is the best thing to do. The positive effect that people have on others can sometimes be immeasurable. Sometimes the best thing you can do to try and heal from the toxicity of people is to try and make sure that you find new relationships that help you to flourish. Make sure that you do not hide or even downplay anything that feels like it is important to you, and again, do not apologize for where you have been in your life.

Seek Professional Help

Sometimes, if you have been in a bad situation, you need to find ways to try to break out of it. One way you can do that would be for you to seek professional help. Professional help can be speaking to a counsellor, or it can be trying to open up to someone who can help you with your debt or your financial situation. If you have been involved in a criminal offense, then seeking the help of a professional lawyer could be a good way to get the legal support you need. DCD LAW is a great option if you feel you need proper representation, and when you go through their service, you will find it easier than ever to not only feel content that you are in good hands, but that you are also able to get the outcome you want.

Be Disciplined

Another good thing to do would be for you to make sure that you are disciplined about your self-care. When you are sick, you may find that you have to take time to rest and to put your feet up. The issue is that if you don’t do this, then you end up burning yourself out even more. If you take this same approach to your mental health, then you will find that it is easier than ever for you to make sure that you are not harming yourself without even realizing it.

Change your Appearance

Changing your appearance is sometimes the best thing you can do. It may be that you need a more deliberate change to reflect your internal change. By altering your style, your make-up, or even your hair, you may find that you can welcome an even nigger change in your life, which is great. It’s also a good idea for you to change what you don’t feel is working for you. When the stakes are high and your life is a little down, it’s a good idea to make sure that you are taking steps to not only try to make sure that you are taking care of yourself but also to make sure that you are acknowledging the things that you are finding hard.

Connect with People

Another thing to do would be for you to try to connect with people who have been through something similar to what you have been through. Get some works of wisdom and also try to read their stories. Now would also be the time for you to try to use the wisdom you have gained over the years to try to support your own journey. Sometimes you need to try to find other people who have been through what you have so you feel less alone. Sometimes unplugging from your device can help too. Take a full week of your life and try to spend as much time outdoors. If you can do this, then you will find it easier not only to make sure that you’re able to connect with the natural world but also to make sure that you’re not running yourself into the ground by trying to be everything to everyone around you.

Buying your first home is an exciting experience. However, it is also a major legal and financial commitment. When added to the impact that it will have on your daily life over the years to come, it is understandably a stressful moment too.

With the right approach, though, it is possible to stay in control throughout the process. Here are some of the most effective ways you can do this in style.

Timing: Focus On Your Circumstance

There has been a lot of talk about the timing of buying a home in recent months. Debates on whether 40 is actually the right time have become increasingly common as a result of statistical trends. Meanwhile, the market itself has been a little less stable in the post-covid era. As such, there have been doubts whether buying is smarter than renting at all.

Ultimately, the advice should be clear: do what works for you. It is far more important to weigh up your finances and current life status, including relationships and career, than worry about your age. Whether you’re 20 or 60, the right time for you is the right time for you.

Legalities: Protect Yourself With The Right Support

As well as being a major legal process, it’s one you have not experienced before. Therefore, it is vital that you get the very best professional support. A dedicated solicitor can guide you through the whole process. As well as understanding the admin and conveyancing fees, it ensures that compliance needs are met at all times. This prevents future repercussions.

Protecting yourself on a legal front isn’t just about money. It also ensures that the process is completed on time, meaning you can move in as expected. Without the right support, you could be left homeless between ending your current tenancy and exchanging on your home.

Finances: Manage Short & Long-Term Matters

Keeping your finances in good health should be a priority throughout the process. When thinking about the costs, you need to look beyond the purchase and legal fees. The logistics of moving and issues like redecorating should be accounted for. Crucially, you should always research mortgage rates and deals to get the very best outcome for your situation.

When looking at properties, it can be worth focusing on fixer-uppers or homes with growth opportunities. It shouldn’t necessarily be the driving factor of your decision. Still, long-term financial prospects make life far less stressful. You should not underestimate its impact.

Preparation: Know What You Need

Finally, the process can become stressful when it feels like you’re taking forever to find the right home. You can make life a lot easier on yourself by conducting advanced research in advance. A clear list of your non-negotiables and desirable extras will narrow your search. This can include the location as well as property features. After all, this will impact your lifestyle.

A little preparation goes a long way to helping you find the home of your dreams. Not least because the wrong choices can be ruled out far sooner. And when you are able to enter this environment with confidence, stress levels will naturally fall.

Image of Grand Blvd in Spokane

Even thinking about moving already causes stress and anxiety, because most often something unpleasant happens during this process. Something can break, someone can forget something, or someone can be late — there are many possible scenarios. That is why city residents, when changing their address, increasingly choose a Spokane moving service as a way to save time, nerves, and property.

This is actually a great idea, because professional services take care of the most difficult stages of the move and allow you to focus on more important moments.

What other advantages does Spokane moving service offer

People often choose to move on their own because it seems cheaper. In reality, such a decision can turn out to be more expensive, as it requires many resources and carries the risk of damage to belongings (especially expensive ones).

So what are you paying professionals for? Spokane moving service provides safe packing of belongings, proper loading and unloading, strict adherence to the schedule, and minimizes your physical effort. This approach truly simplifies the process and reduces the number of unexpected situations.

Moving service Spokane WA for comfortable moves

Moving in suburban areas has its own specifics — larger houses, more furniture, appliances, and expensive or fragile items. Moving service Spokane WA is often ordered for full process support, because it is about comfort, saving time, and often saving money.

Services usually include:

- packing and labeling boxes

- transportation of furniture and household appliances

- careful placement of items in the new space

In this case, packing and unpacking are done by professionals with extensive experience, who know how to do it properly to avoid damaging any details.

Commercial moving service Spokane WA for businesses

Commercial moves are often associated with large volumes of bulky equipment and furniture. Commercial moving service Spokane WA can offer different crew sizes and vehicle options so that the move is fast and comfortable.

Professional services take into account the type of commercial space, safety requirements, timelines, and stages of the move.

Office moving service Spokane WA: when time matters

An office move is about clear process organization, because every hour of downtime costs a business money. Office moving service Spokane WA usually saves businesses a lot of time and eliminates unnecessary headaches.

Teams know what to do in order to:

- avoid damaging equipment and documents

- minimize work interruptions

- preserve the logic of workspace layout

How to choose a reliable moving service

When moving, it is important to choose a company that fits not only in terms of price, but also by other criteria. Here is what we recommend paying attention to.

| Criterion | Why it matters |

| Work experience | Guarantees professional move organization without damage to belongings or unexpected situations. |

| Insurance | Property protection means safe packing, transportation, and the service’s responsibility for your belongings. |

| Clear schedule | Time control allows adherence to a clear schedule and helps avoid delays. |

| Real reviews | Customer trust is built through transparent company operations and real feedback from people who have already used the services. |

Moving service Spokane WA will not only help organize the process quickly and safely, but will also make moving day a pleasant memory rather than a terribly stressful day.