Corporate giveaways have become a staple in business marketing strategies, as they offer a tangible way to leave a lasting impression on clients, customers, and employees. Handing out branded items at events like trade shows, customer appreciation days, and employee recognition programs not only promotes your brand but also builds goodwill and loyalty among those who receive the items. Each time potential clients use the branded pens, tote bags, or fabric wristbands they’ve acquired from you, they’re reminded of your brand and their experiences with it.

However, careful budgeting is necessary to realize the full benefits of any corporate giveaway. Without meticulous planning, the costs of giveaways can quickly spiral out of control, diminish the return on investment, and even potentially hurt your bottom line. Think of every dollar you spend on giveaways as an investment in your brand’s future, as your main objective with every giveaway is to enhance the company’s visibility and reputation.

This article will guide you through the key considerations that are necessary for creating an effective budget for corporate giveaways. By the end, you’ll have a clearer understanding of the factors to account for, which in turn will ensure that your promotional efforts are both impactful and financially sound.

Type and Cost of Items

If you want your giveaway to make a lasting impact, you’ll need to choose the right items. Consider your target audience, the occasion, and the relevance of the items. For instance, tech gadgets might find favor with a younger, tech-savvy crowd, while classic items like pens and tote bags can have a broader appeal. Don’t forget to estimate the cost per item and determine the appropriate quantity. Bulk orders often come with discounts, but be sure to balance quantity with quality to avoid compromising on your brand’s image.

Design and Development

The design phase is where your giveaway items start to come to life. It’s often a good idea to invest in professional graphic design to improve your items’ appeal. As such, customized designs that incorporate your logo and company colors can make your giveaways stand out. Just make sure to budget for prototype samples to ensure the final product meets your expectations. This phase is vital for refining the design and avoiding costly mistakes in mass production.

Production Expenses

Manufacturing costs can vary widely depending on the materials and the complexity of your custom design. High-quality materials might cost more upfront but can also enhance the perceived value of your giveaways. It’s also important to consider the manufacturing process itself. Have stringent quality control checks done on each item to verify that they meet your standards. Though this might seem like an additional expense, the funds you allocate will help safeguard the integrity of your brand and guarantee a more positive reception from your recipients.

Packaging

Good packaging will do more than protect your items in transit since they also create a memorable unboxing experience, which can enhance the presentation and perceived value of your giveaways. Consider individual packaging that highlights your branding, such as custom boxes or bags with your logo and company colors. Showing attention to detail here can leave a lasting impression on recipients. It’s also wise to budget for bulk packaging for storage and shipment purposes.

Shipping and Handling

You can expect shipping and handling to take up some substantial room in your budget, especially if you’re distributing giveaways to a wide audience. Domestic shipping costs can add up quickly, and international shipping introduces additional expenses like customs and duties. Plan for these costs and choose reliable shipping methods to achieve timely and secure delivery. Consider negotiating rates with shipping carriers or using fulfillment services that offer bulk shipping discounts.

Event-Specific Costs

If you’ll be distributing your giveaways at specific events, such as trade shows or conferences, there are additional costs to account for. These can include booth space, event registration fees, and any additional staffing required to manage your booth and hand out the items. Consider also allocating funds for event-specific promotional materials that complement your giveaways, such as banners, flyers, and interactive displays. After all, events are prime opportunities for brand exposure, so it’s crucial to present your company in the best light. Approach any events you attend as comprehensively as you can, and you’ll find that your giveaways become more impactful and your presence more memorable.

Contingency Fund

No matter how well you plan, unforeseen expenses can still arise. Set aside a contingency fund in your budget to help manage unexpected costs without compromising the quality or quantity of your giveaways. This fund can cover a range of miscellaneous fees, such as last-minute design changes, rush order fees, or additional shipping costs. Think of this contingency fund as a financial safety net that can keep your giveaway campaign running smoothly even when you encounter unexpected challenges.

At the end of the day, you can think of a well-planned budget as the cornerstone of any corporate giveaway campaign—without it, you can’t succeed. Consider all associated costs carefully and you’ll soon learn how to strike the balance between promoting your brand widely and securing a solid return on investment. The ultimate goal is to make your promotional efforts work as hard for you as possible so that every giveaway item you hand out functions as a valuable brand ambassador.

Lump sum investing is a strategic financial approach that can significantly impact your investment journey.

Whether you’ve received a windfall, an inheritance, or have simply saved up a substantial sum, the decision of whether to invest it all at once or gradually deploy it can be daunting.

In this article, we’ll explore the concept of lump sum investing, its advantages and disadvantages, and provide insights into making an informed decision that aligns with your financial goals.

What is Lump Sum Investing?

Lump sum investing is a strategic financial approach that entails allocating a substantial sum of money across diverse asset classes in a single transaction, as opposed to the gradual investment method known as dollar-cost averaging.

This approach captures attention due to its potential to generate amplified returns within a relatively condensed timeframe.

Unlike dollar-cost averaging, where funds are trickled into investments over a series of intervals, lump sum investing capitalizes on the immediate deployment of funds.

The allure of lump sum investing lies in the prospects of achieving higher returns. By entering the market with a lump sum, investors position themselves to capitalize on potential market upswings more swiftly.

This acceleration can be attributed to the full deployment of resources, allowing for a greater extent of market exposure from the outset.

This approach, however, is not without its considerations, as it necessitates a thoughtful evaluation of one’s risk tolerance and market insights before making the bold move.

An Example of Lump Sum Investing

An example of lump sum investing could involve an individual who receives a sizeable inheritance following the passing of a family member.

Let’s consider someone who inherits a substantial sum of money. Instead of gradually investing the funds over time, as one might do with dollar-cost averaging, this person decides to pursue lump sum investing.

After conducting thorough research and seeking advice from financial experts, they identify a diverse range of investment opportunities, including stocks, bonds, real estate, and mutual funds. Then, they allocate the entire inheritance into these various assets all at once.

By taking this bold step, this They to maximize the potential for higher returns over the long term. She acknowledges that markets can be volatile, but they also believe in the historical trend of markets generally experiencing growth over extended periods.

By entering the market with her lump sum, they seek to benefit from potential market upswings without missing out on potential gains.

Can You Time the Market?

Guessing exactly what will happen in the market is super hard. Most experts say it’s not a good idea to try and “time the market” because it’s really tough to get it right.

But if we look at the past, we can see that usually, putting your money in sooner rather than later is better for making more money over a long time.

Even though it’s tricky, history shows that if you keep your money in the market for a long time, you usually end up with more money. The market tends to go up over time, so if you try to guess exactly when to buy or sell, you might miss out on the times when it’s going up.

Instead of trying to guess the short-term changes, it’s often better to make a plan for the long term, do some research, spread out your investments, and be patient to reach your money goals.

Assessing Risk Tolerance

When it comes to lump sum investing, it’s really important to figure out how comfortable you are with taking risks. This is called your “risk tolerance.”

Since the market can sometimes go up and down a lot, you need to think about whether you can handle the idea of maybe losing money in the short term but having the chance to make more money in the long run.

Think about it like this: imagine you’re on a roller coaster. Some people love the excitement and twists, while others get really nervous.

Your risk tolerance is a lot like that feeling. If you’re okay with the ups and downs of the roller coaster, you might have a higher risk tolerance. But if the idea of the drops and turns makes you really uncomfortable, your risk tolerance might be lower.

It’s all about knowing yourself and what you’re okay with.

If you’re someone who can handle the ups and downs without getting too stressed, lump sum investing might be a good fit for you. But if you’re the type who worries a lot about losing money, you might prefer to take a more gradual approach.

The key is to find a strategy that matches your feelings about risk and helps you achieve your financial goals.

Potential for Higher Returns

Looking at historical data, lump sum investing has the potential to yield better results than dollar-cost averaging. If the market is steadily rising, investing a lump sum upfront could result in more substantial returns.

Comparatively, lump sum investing is akin to climbing a ladder all at once, while dollar-cost averaging is akin to climbing it step by step.

If the ladder (market) is ascending, being invested from the outset can lead to more significant growth.

Similarly, envision a dice game at a fair; rolling the dice once (lump sum) could lead to a big win if the outcome is favorable.

In contrast, multiple dice rolls (dollar-cost averaging) might yield smaller wins, although they are more probable.

Consequently, if the market is performing well and experiencing an upward trend, placing all funds into investments at once could be a judicious decision.

However, it’s crucial to understand the risk involved and conduct thorough research before making such a commitment, considering that markets can also experience downturns.

Dollar-Cost Averaging as an Alternative

While lump sum investing has its advantages, there’s another approach called dollar-cost averaging that might catch your interest. This strategy is all about managing the effect of the market’s ups and downs in a structured way.

Here’s how it works: instead of putting all your money into investments in one go, you spread it out over time. It’s like making a series of small deposits instead of one big deposit.

By doing this, you buy more shares or units when prices are low and fewer when prices are high. This averages out the cost of your investments, which can help reduce the impact of sudden market swings.

Think of it like buying shoes when they’re on sale. Sometimes they cost less, and sometimes they cost more.

By purchasing them at different times, you end up paying an average price. Similarly, with dollar-cost averaging, you’re investing at various points, which can help smooth out the impact of market volatility.

This approach is particularly useful when markets are unpredictable. If you’re worried about the market suddenly dropping right after you invest a large sum, dollar-cost averaging might ease your concerns. It helps reduce the risk of making a big investment just before the market takes a downturn.

This strategy is all about patience and consistency, and it’s designed to help you navigate the market’s twists and turns with more confidence.

Psychological Considerations of Lump Sum Investing

Putting a lump sum of money into investments isn’t just about numbers and strategy; it’s also about how you feel. Emotions can play a big role, especially when the market gets a bit wild.

It’s like a roller-coaster ride for your feelings!

When the market goes up and down quickly, it can make you feel nervous or excited. You might worry that your investment will suddenly lose value, or you might get super hopeful when it’s doing well. These emotional ups and downs can make it hard to make smart decisions.

But here’s the thing: emotions can sometimes lead us astray, especially in the world of investing. That’s why it’s important to keep a clear head.

Staying informed about what’s happening in the market is a great start. Understanding that markets have their ups and downs and that it’s all part of the game can help you keep your cool.

Don’t let short-term changes in the market trick you into making rushed decisions.

Instead, maintain a long-term perspective and remember why you started investing in the first place.

This way, you can make decisions based on solid information rather than just following your feelings in the moment. It’s all about finding a balance between logic and emotions to help you make the best choices for your financial future.

Common Mistakes to Avoid When Investing a Lump Sum

Investing a lump sum of money can be both exciting and nerve-wracking.

However, to make the most of your investment, it’s essential to steer clear of some common mistakes that many people fall into.

1. Letting Emotions Take the Wheel

Imagine if you bought a car based on how it looks instead of how well it runs. Emotions can cloud your judgment when it comes to investing, just like they would when choosing a car.

Making impulsive decisions driven by fear or excitement can lead to choices that don’t align with your long-term goals. It’s crucial to stay rational and avoid letting emotions dominate your investment choices.

2. Skipping the Homework

Think of investing like planning a vacation. You wouldn’t go to a new place without researching first, right? Neglecting proper research and due diligence when investing is similar to heading into the unknown without a map.

Understand the assets you’re investing in, their potential risks, and historical performance. Solid research helps you make informed decisions, increasing your chances of success.

3. Putting All Eggs in One Basket

Imagine if all your meals consisted of only one type of food – it wouldn’t be very balanced or healthy.

Investing all your money in a single investment is like relying on one type of food for all your nutrition. Diversification is key. Spreading your investment across different assets helps lower the impact of a poor-performing investment on your overall portfolio. It’s a way to manage risk and potentially improve returns.

4. Ignoring Tax Consequences

When you make a big purchase, you consider the price and any added costs like taxes, right? Ignoring tax implications when investing is like ignoring the extra costs that come with a purchase.

Different investments have different tax implications, and these can impact your returns. Consider consulting a tax professional to ensure your investment strategy is tax-efficient and aligns with your financial goals.

Avoiding these common mistakes can significantly improve your chances of success when investing a lump sum. Just like any endeavor, investing requires careful planning, informed decisions, and a clear understanding of your goals.

By staying rational, doing thorough research, diversifying wisely, and considering tax implications, you’re taking steps toward maximizing the potential of your lump sum investment.

Conclusion

Lump sum investing can be a bold move that has the potential to yield substantial returns over time.

By understanding your risk tolerance, conducting thorough research, and seeking professional advice, you can make an informed decision that aligns with your financial aspirations.

Remember, the key is to stay focused on your long-term goals, rather than getting caught up in short-term market fluctuations.

Living below your means is a financial strategy that involves spending less than what you earn. This practice might seem simple, but its impact on your financial health and overall well-being can be profound.

In this article, we’ll explore the benefits of living below your means and provide practical tips for incorporating this approach into your lifestyle.

Living Below Your Means: A Pathway to Enhanced Financial Security

Financial security is a cornerstone of a stable and stress-free life. Living below your means is a strategy that offers a powerful route to achieving this security. This approach involves consistently spending less than your income, creating a financial buffer that safeguards you from unexpected expenses and emergencies.

Imagine having a safety net that cushions you against life’s financial curveballs. When you live below your means, you’re essentially building this safety net with every dollar you save. This fund becomes your shield, protecting you from the stress and anxiety that often accompany unforeseen financial challenges.

Building a Safety Net: By consistently saving a portion of your income, you’re actively creating a safety net that can catch you during times of need. Whether it’s a medical emergency, car repair, or sudden job loss, having funds set aside provides a sense of preparedness and control.

Reducing Financial Uncertainties: Financial uncertainties can wreak havoc on your overall well-being. When you’re living paycheck to paycheck or spending beyond your means, the slightest financial hiccup can trigger a spiral of stress. In contrast, living below your means empowers you to weather these uncertainties with greater ease, knowing that you have resources to fall back on.

Embracing Peace of Mind: The psychological impact of financial security should not be underestimated. When you know you’ve made the conscious choice to live below your means, you’re cultivating a mindset of control and responsibility. This, in turn, cultivates peace of mind, allowing you to focus on other aspects of your life without the constant weight of financial worry.

Ultimately, living below your means is more than just a financial strategy; it’s a powerful step toward achieving lasting peace of mind. By taking control of your financial situation and creating a safety net, you’re proactively shaping your future and ensuring that you’re prepared for whatever comes your way.

A Gateway to Financial Freedom from Debt

In today’s consumer-driven society, the allure of credit and loans is ever-present. However, living below your means presents a powerful antidote to the debt trap that can ensnare individuals and families. This practice entails spending less than you earn, effectively minimizing your reliance on credit and loans and safeguarding your financial well-being.

Fending off the Debt Trap: Living within your means serves as a protective shield against the perils of debt accumulation. By consciously spending less than your income, you create a financial cushion that reduces the need to turn to credit for everyday expenses. This proactive approach prevents you from falling into a cycle of borrowing that can burden your finances for years.

Breaking Free from Debt: If you’re already grappling with debt, living below your means becomes a strategic lifeline to regain control. By directing a significant portion of your income towards debt repayment, you accelerate the process of becoming debt-free. This not only lightens your financial load but also frees up resources for savings and investments that can shape your financial future.

The Power of Responsible Credit Use: While credit isn’t inherently harmful, its misuse can lead to financial distress. If you do utilize credit, the principle of living below your means continues to guide your actions. Paying off your credit card balance in full each month is a pivotal practice that prevents the accumulation of high-interest charges. This not only preserves your financial health but also contributes to building a stronger credit history.

Fostering a Healthier Financial Picture: Living below your means isn’t solely about scrimping and sacrificing—it’s about making conscious choices that align with your long-term financial well-being. By avoiding unnecessary debt and managing existing debt responsibly, you’re crafting a financial landscape that offers stability, flexibility, and the freedom to pursue your goals.

Empowerment Through Debt Reduction: Imagine the feeling of liberation that comes from shedding the weight of debt. Living below your means empowers you to make consistent progress towards this goal. The discipline and dedication required to achieve debt reduction set the stage for a future where your income can be directed towards building wealth, rather than servicing debts.

A Gateway to Mental and Emotional Peace

Financial stress can severely impact your mental and emotional well-being, casting a shadow over every aspect of your life. The constant worry about making ends meet, the weight of mounting debt, and the anxiety of unexpected expenses contribute to an ongoing state of unease. Conversely, adopting the principle of living below your means offers a transformative solution, reducing stress and promoting overall well-being.

Living below your means demands financial discipline, resulting in a unique form of confidence rooted in informed decision-making and future-oriented planning. This newfound financial confidence extends beyond money matters, positively influencing various aspects of your life. As the mental burden of financial stress is alleviated, your mental clarity improves. Freed from constant money-related concerns, you can redirect your mental energy towards pursuing passions, advancing in your career, and nurturing relationships.

Furthermore, financial stability is a cornerstone of emotional resilience. With the capacity to manage financial challenges, you’re better equipped to handle life’s inevitable ups and downs with composure. The resultant emotional resilience reaches far beyond financial matters, improving your ability to cope with a wide range of stressors. As financial worries diminish, you experience an elevated quality of life. You’re able to focus on meaningful connections, personal growth, and cherishing life’s moments, enriching your overall well-being.

Ultimately, the journey of living below your means is a pathway to liberating financial freedom. Shedding the weight of financial burdens reveals the joy of making choices based on aspirations rather than limitations. This transition not only restores your mental and emotional well-being but also generates a positive ripple effect across all spheres of life. By nurturing a sense of control, fostering financial confidence, and promoting mental clarity, the transformation towards reduced stress and enhanced well-being becomes a driving force in shaping a fulfilling and harmonious life.

Examples of Living Below Your Means

These examples showcase how living below your means involves conscious choices to spend less on non-essential items and prioritize financial stability and future goals. By implementing such practices, you can free up resources for saving, investing, and pursuing experiences that truly matter to you.

- Budgeting for Necessities: Creating a budget that prioritizes essential expenses such as housing, utilities, groceries, and transportation before allocating funds for discretionary spending.

- Cooking at Home: Opting to cook meals at home rather than dining out frequently, which can save a significant amount of money over time.

- Using Public Transportation: Choosing public transportation, biking, or walking instead of owning and maintaining a costly car, especially in areas with reliable public transit systems.

- Frugal Shopping: Seeking out discounts, using coupons, and buying items on sale, while avoiding impulse purchases and focusing on necessary items.

- Minimalist Lifestyle: Embracing a minimalist approach to possessions, reducing clutter, and avoiding unnecessary purchases that contribute to both financial and mental clutter.

- Downsizing Housing: Opting for a smaller, more affordable living space that fits your needs instead of overspending on a larger home.

- Emergency Fund: Building an emergency fund to cover unexpected expenses, reducing the need to rely on credit cards or loans in times of crisis.

- DIY Projects: Tackling do-it-yourself projects for home repairs and maintenance instead of hiring professionals, saving money on labor costs.

- Carpooling or Ride-Sharing: Sharing rides with colleagues or using ride-sharing services to split transportation costs, particularly for daily commutes.

- Prioritizing Quality over Quantity: Investing in quality items that last longer, even if they have a higher upfront cost, rather than buying cheaper items that need frequent replacements.

- Buying Used Items: Purchasing gently used or second-hand items such as clothing, furniture, and electronics to save money while still meeting your needs.

- Cutting Cable and Subscriptions: Canceling cable TV and unnecessary subscription services, opting for more affordable streaming options that align with your viewing habits.

- Renting Instead of Owning: Renting tools, equipment, or recreational items instead of purchasing them outright, especially if they’re only needed occasionally.

- Negotiating Bills: Negotiating with service providers (like cable, internet, or insurance companies) to lower bills or switch to more cost-effective plans.

- Entertainment Alternatives: Exploring free or low-cost entertainment options such as community events, parks, libraries, and cultural activities.

Practical Tips for Living Below Your Means

Here are some actionable steps to help you implement the “living below your means” philosophy:

1. Create a Detailed Budget: List your sources of income and all your expenses. Allocate funds to essentials like housing, utilities, groceries, and transportation before considering discretionary spending.

2. Trim Unnecessary Expenses: Identify non-essential spending and cut back on luxuries like dining out, entertainment subscriptions, and impulse purchases.

3. Build an Emergency Fund: Set aside a portion of your income into an emergency fund. This safety net will provide peace of mind in case of unexpected financial challenges.

4. Save Before Spending: Prioritize savings by setting aside a percentage of your income before allocating funds for discretionary spending.

5. Avoid Lifestyle Inflation: As your income increases, resist the urge to immediately raise your spending. Instead, allocate the additional funds to savings and investments.

6. Invest Wisely: As your financial situation improves, consider investing to grow your wealth. Consult with financial professionals to make informed investment decisions.

Conclusion

Living below your means is a transformative financial strategy that brings numerous benefits to your life. It offers financial security, supports goal achievement, and reduces stress. By adopting this approach and making intentional choices, you can cultivate a healthier financial outlook and pave the way for a brighter and more fulfilling future.

Though it may not be as well-known in the United States, Islamic financing and banking is considered to be one of the most established and well-renowned in the world. Following Shariah laws, which forbid traditional mortgages, Muslims have an alternative for financing the purchase of a home.

It is important to know what an Islamic mortgage is, what it entails, and how customers can borrow the money necessary to finance their home. There are also inherent advantages to Islamic or Halal mortgages, notably below.

What is an Islamic Mortgage?

To discover the benefits of Islamic mortgage options, one must know what an Islamic mortgage is. In Islam, money is thought to have no inherent value. Personal finance and wealth are only permissible through fair trade. Making profit from money goes directly against Shariah Law.

An Islamic mortgage, compliant with Shariah law, isn’t technically a mortgage as much as it is a home purchase plan (HPP). Consider it a lease agreement between the customer and the lender, with no payable interest. The HPP allows customers to purchase their homes while keeping their faith.

A Growing Industry

The Islamic finance industry continues to grow by leaps and bounds. In 2023, Islamic banking’s share of total financing was roughly 45.6 percent. The market is expected to reach $5.9 trillion USD by 2026.

An Islamic mortgage is a fantastic option for buyers looking to adhere to Shariah law while finding a cost-effective means of financing their home. Tremendous growth within the market only stands to create more options for Islamic buyers in the coming years. Not all mortgages are created equally, and Islamic mortgages make it possible for those who aren’t able to take out a conventional mortgage.

Lower Penalty Fees

An Islamic mortgage is generally less expensive in a few ways. One of the primary benefits of an Islamic mortgage is the lower penalty fee for property disposal within the lock-in period. For conventional loans, the penalty fee for an early settlement or prepayment is a set fee.

With an Islamic mortgage, the bank will charge a penalty fee based on the bank’s prevailing cost of funds. That said, the penalty fees can differ between Islamic banks. Check with the lenders you’re considering to understand the details of any penalty fees.

Cost of Stamp Duty

Stamp duty is the land tax that must be paid when buying a property over a particular value. One significant benefit of an Islamic mortgage is that the cost of stamp duty can be as much as 20% lower. Those are no small savings to the buyer.

Islamic financing agreement documents must be filed to gain these benefits. When refinancing from a conventional loan to an Islamic home loan, stamp duty can also be waived for the redeemed amount. That kind of savings isn’t commonly available on conventional loans, another major benefit in addition to adherence to Shariah law.

Base Financing Rate (BFR)

Conventional loans operate under the Base Lending Rate. Islamic loans, however, are based instead on the Base Financing Rate (BFR). The bank can adjust depending on prevailing market conditions but cannot do so more than the ceiling rate.

That ceiling rate is the maximum profit an Islamic finance provider can earn. Compared to conventional home loans, buyers save mightily. Moreover, there is a fixed monthly repayment option so property owners can easily adjust their monthly budget.

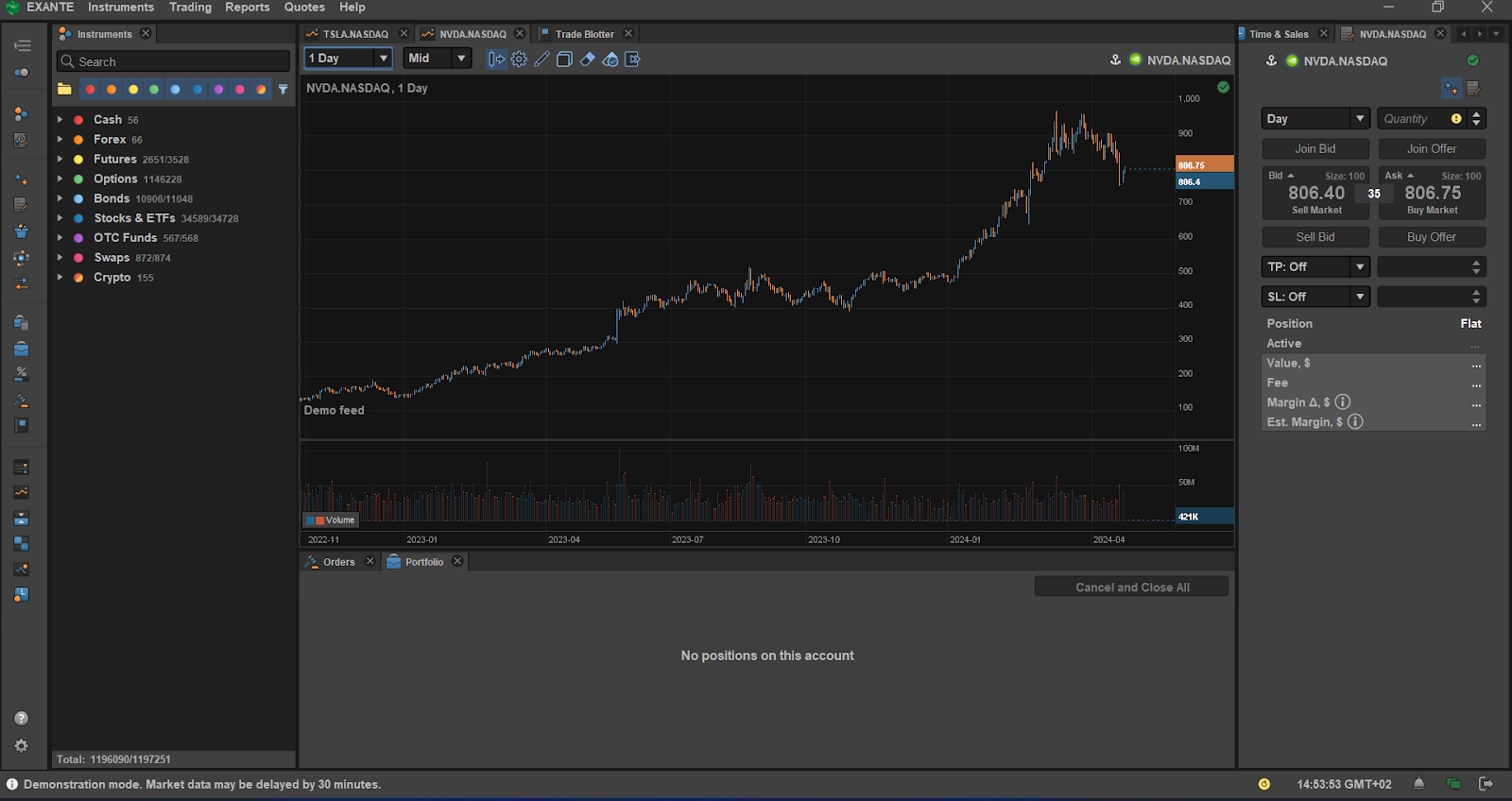

The EXANTE trading platform allows traders to trade over a million financial instruments with access to over 50 global markets. The platform is ideal for experienced traders and is available to clients on mobile, web, and desktop platforms.

Clients using the EXANTE platform include banks, wealth managers, and private investors. This review looks at the trading platform features and how EXANTE stays on top of international sanctions.

About EXANTE

EXANTE is a trademark owned by XNT Ltd, a regulated investment firm.

Staying on top of international sanctions

Owned by a regulated investment firm, EXANTE, as part of its commitment to regulatory compliance, does not accept clients from any sanctioned country or region and respects all sanctioned lists. EXANTE, through the investment firms offering the platform to their clients, cooperates with any regulator concerning sanction-related requests.

In addition to applying new sanctioned lists from respective authorities, EXANTE remains compliant by regularly screening for sanctioned instruments on its trading platform.

EXANTE complies with the Markets in Financial Instruments Directive (MiFID II) as a measure to safeguard investor funds. As such, EXANTE implements asset segregation and holds company funds separate from client funds, which are held by trusted custodians (respected European banks and other financial institutions).

The trading platform

The EXANTE trading platform is designed for experienced investors and offers numerous customization options. It is accessible on desktop, mobile, and web, providing clients with a dependable trading platform featuring cutting-edge technology.

With the EXANTE platform, traders can set price alerts, access over a million financial instruments, and have real-time charts with historical data and multiple timeframes.

The desktop platform has many features, including the Bond Screener module, which allows traders to easily find promising bonds. Traders also have detailed information on various instruments, such as overnight rates, margin requirements, and more.

The web version allows clients to trade without having to download any software. For traders on the move, the mobile app is a good option and allows for convenient trading abilities.

Mobile app

EXANTE’s mobile app is available for Android and iOS users and gives traders access to all trading instruments from a single account. It has a user-friendly interface and provides portfolio management, real-time market data, and the ability to execute trades in a few taps.

The app also has a range of technical indicators and charting abilities and places a high priority on security. Like the desktop version, it uses Two-Factor Authentication (2FA) and automatic logouts to protect sensitive data.

Fees

EXANTE has a transparent fee structure and only charges fees for actual trades.

The maximum trading fee for stocks and ETFs on main U.S. exchanges is USD 0.02 per share and ranges from 0.02% to 0.18% on European exchanges. Asian exchanges have a fee range of 0.1% to 0.1927%.

In terms of futures and options, fees for US exchanges start at 1.5 USD while fees for European exchanges start at 1.5 EUR. For currency pairs, there is a conversion fee of 0.25% on all major currency pairs and a 0.4% fee for all other pairs.

Please note that these fees are up to date as of 2024 and the latest fees can be found on their website (exante.eu).

The minimum opening deposit is 10,000 EUR for individual professionals and 50,000 EUR for corporate accounts. New clients can choose to start with a demo account with €1,000,000 in virtual currency so they can practice their trading skills and learn how to use the platform.

Conclusion

EXANTE is a trading platform used by experienced traders worldwide. It provides a comprehensive range of trading instruments and has a very transparent fee structure.

Even though it has a high minimum deposit requirement and lacks certain automation features on its platform, EXANTE is a reliable trading platform with an impressive client base that includes banks, wealth managers, and professional investors.

It remains compliant with updates to local and international sanctions and employs numerous measures to safeguard investor assets and personal information.

EXANTE Trading Platform, Features, and Sanctions

DISCLAIMER:

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication. Costs mentioned herein may increase or decrease as a result of currency and exchange rate fluctuations and are subject to change.

Too many Financial markets can seem really hard with changing trends and ups and downs. To do well here you need to know a lot about how markets work and make quick smart choices. Huge amount of data and the need to analyze it fast makes it tough for both new and experienced traders. Finding a trustworthy tool that makes this easier while giving accurate info can feel almost impossible. But platforms like Techberry try to help by using advanced tech and easy-to-use features to help traders succeed.

Techberry’s Start and Growth

Techberry started in 2015 aiming to change trading for everyone. Made by traders for traders it makes advanced trading strategies available through AI and the know-how of over 100,000 skilled traders. The cool thing about this method is that Techberry’s AI can now tell the difference between good and bad trades. It keeps learning from live data picking out useful info and focusing on positive trends. This smart system helps users get the best insights for their trades. Using this high-tech approach Techberry offers a powerful tool to help traders improve their strategies and make more money. Since it started it has shown strong results gaining more users and respect in the trading world. The platform’s easy-to-use interface and strong AI features make it good for both new and experienced traders wanting to get better at trading.

BlackRock May Buy Techberry

There are talks that BlackRock might acquire full or partially Techberry in near future. This could greatly affect Techberry’s future operations and growth. While no official news has been given the market is full of speculation and excitement. If BlackRock goes ahead with the purchase experts suggest that it might increase Techberry’s user profits by 1.5x to 2x.

Features and Unique Offering of Techberry

Simpler Bitcoin Investment

If you want to make money from Bitcoin’s price changes without dealing with blockchain Techberry’s BTC membership plans are a good option. These plans let users profit from Bitcoin’s price changes without the tech and security worries of direct crypto investments. Techberry supports many payment methods like bank transfers credit cards and wire transfers and users can withdraw money at current BTC rates. This makes investing easy and safe even for those new to crypto.

Try Techberry with Demo Mode

The platform’s demo mode is a great way to get to know it without risking real money. The demo account lets users try out the platform’s tools and trader cabinet fully. Easy to access from the homepage the demo account can be set up in three steps. This feature gives practical experience and helpful insights into the trading world helping users understand the platform before spending any money.

Live Trading Data Insights for Transparency

Having access to real-time data is very important and Techberry does well in providing live stats on its website. This feature lets users check performance gains and market trends giving them the knowledge they need for effective trading. By offering up-to-the-minute stats Techberry helps users make smart decisions based on the latest market data.

Strong Security Measures for User Safety

Security is very important in trading and Techberry takes this seriously with strict measures. The platform has regular security checks by top independent firms like FX Audit FX Blue and MyFxBook ensuring transparent and reliable operations that meet the highest security standards. Techberry uses advanced encryption to protect user data and transactions from unauthorized access. The platform also uses multifactor authentication to make sure only authorized users can access their accounts. To protect user funds Techberry keeps them in separate accounts apart from the company’s operating funds making sure user money is safe even if the company has problems. The platform also offers insurance for user funds adding extra protection. Ongoing monitoring and regular security updates are part of Techberry’s commitment to a secure environment quickly finding and fixing potential threats. These thorough security measures give users peace of mind knowing their data and money are well protected.

Integrated AI-Driven Analytical Trading

Having a lot of data is key for effective AI in trading. Many platforms have trouble managing data but Techberry has solved this with a smart AI algorithm. This algorithm filters out bad data and focuses on positive trends making it very efficient. Techberry’s success comes from data from over 100,000 traders. This big data pool supports 90% of the platform’s successful trades giving accurate and reliable insights that improve trading results.

Automated Trading for Easy Income

Many traders want passive income and Techberry makes this possible with its AI-driven automated trading. With a 90% success rate Techberry’s automated system has let users earn an average monthly return of 11.2% since it started. This system allows users to make money from the markets without actively managing their trades making it perfect for those looking for easy income. The automated feature uses AI to handle trades well ensuring steady profits for users.

Diverse Membership Plans for Traders of All Levels

Techberry has different membership plans to fit various trading needs and experience levels making sure every trader finds a plan that matches their goals. The platform offers plans from the basic White plan to more advanced ones like Green Silver Gold Platinum Diamond and Infinite each with unique benefits and pricing. Furthermore, it features an Exclusive VIP Elite Membership plan for top and professional traders designed to maximize investment returns. VIP Elite members get dedicated support including one-on-one sessions a personal manager custom trading strategies and real-time market monitoring with timely insights. This plan has a 10% service fee on profits making it a good option for serious traders. A special perk of VIP Elite Membership is an invite to VIP Annual Exclusive Global Event where members can network with industry leaders and join exclusive discussions. Photos and videos of the 2023 event are on official site.

Bright Future for Techberry

Based on research experts believe Techberry has a promising future ahead. The platform’s use of advanced AI technology and extensive trader data puts it in a good position to stay a market leader. Plans to expand membership options, improve AI algorithms and add more advanced features to support traders at all levels are set to shape the future of trading offering great opportunities for traders worldwide.

In the sprawling labyrinth of modern finance, few dangers lurk as ominously as identity theft. As swift and invisible as a shadow, it can strike anyone, anywhere. A financial fortress, painstakingly built over years of hard work and dedication, may crumble in mere moments under the insidious siege of a skilled identity thief.

In a world increasingly interconnected, where money and personal information flow across digital streams, guarding one’s financial fortress has become paramount. But how does one do it? What are the hidden risks, the unseen pitfalls? And more importantly, how can one recover if the unthinkable happens?

Understanding Identity Theft

We might be too focused on building wealth that we end up ignoring other important aspects. A prime example of the latter is identity theft, which can crash your dreams in an instant once you become a victim.

Identity theft is a crime that steals and uses a person’s private information, often for financial gain. It’s a crime that might seem distant or abstract, something that happens to other people, but not to you. Truth is, this is one thing that anyone can experience.

But what makes identity theft so perplexing? You might be familiar with a phishing attack. The latter happens when criminals pretend to be trustworthy entities. In turn, they lure individuals into revealing personal information. These schemes can range from deceptive emails to intricately disguised websites, each one more cunning than the last.

Identity theft can also manifest in the form of credit card fraud. This is when criminals acquire your credit card information to make unauthorized purchases. It sounds simple, but the techniques are manifold and ever-evolving. Therefore, it can be challenging to detect and prevent. The need for enhanced solutions for identity theft is apparent in this evolving landscape, where traditional defenses may no longer suffice.

Even more harrowing is the case of medical identity theft. It happens when thieves use your name or health insurance numbers to see a doctor, get prescription drugs, file claims with your insurance provider, and more. Its effects go beyond your finances.

And let’s not overlook tax-related identity theft. In these cases, your social security number might be used to falsely file tax returns. You may only discover this when you go to file your taxes, only to find that a return has already been filed in your name.

Financial Impact

The initial shock of discovering identity theft is often followed by a worse realization: the financial toll it takes. At first glance, you might think of immediate losses, such as drained bank accounts or unauthorized credit card purchases. The theft may seem contained, limited to mere numbers on a screen. But the reality is a sprawling, tangled mess of consequences that reach far deeper. Therefore, guarding against identity theft must form a part of your money management strategy. Doing so can protect your savings and investments.

Immediate Losses

The financial impact of identity theft is immediate and visceral. Unauthorized transactions might be a mere annoyance if rectified quickly, but if left unchecked, they can lead to significant financial distress. Empty bank accounts, maxed-out credit cards, bounced checks – these are just the superficial scratches on the surface of a much more profound wound.

But the complexity doesn’t stop there. The immediate losses from identity theft extend beyond simple monetary values. Your investments may be affected, your hard-earned savings depleted, and even your ability to secure loans or mortgages might be compromised. The ripple effect is swift and expansive, turning a seemingly isolated incident into a financial maelstrom.

Long-term Consequences

While grappling with the immediate aftermath, the long-term consequences of identity theft begin to take shape. The wound deepens; the infection spreads. Damage to your credit score, once a minor concern, becomes a haunting specter. Recovering from a significant drop in credit ratings can take years, affecting everything from car loans to housing applications.

Perhaps more insidious is the potential harm to retirement funds or long-term investments. Identity theft can lead to misinformation in your financial records, causing lingering confusion and potential loss over time. What might have been a comfortable retirement can be thrown into uncertainty.

And what about the emotional toll? The constant anxiety, the lingering doubt, the fear that your financial fortress is forever breached? These unseen scars may not have a monetary value, but they are a lasting part of the identity theft landscape.

Prevention and Protection

The foundational layer of defense in guarding against identity theft comprises a series of simple but essential steps, often overlooked yet crucial in their effectiveness.

At the core of these basic measures is password management, ensuring that all passwords are strong, unique, and regularly updated. Implementing two-factor authentication (2FA) adds another layer of security, requiring an additional form of verification alongside the traditional password.

Regularly updating software, being vigilant against phishing emails, securing your Wi-Fi network, and even simple acts like locking your mobile devices all contribute to a robust first line of defense. These measures might seem elementary, but they provide a vital barrier against common threats, setting the stage for more advanced strategies. They are the bricks and mortar in the construction of a financial fortress, the necessary groundwork for a holistic approach to prevention and protection.

More so, the use of identity theft protection software has become an essential part of a comprehensive strategy. For example, Aura is accredited by the Better Business Bureau (BBB), offering tools designed to monitor and alert users of any suspicious activities related to their personal information. It can detect early signs of identity theft, allowing for swift action before significant damage occurs.

But the options don’t end with monitoring. Many software solutions also offer recovery assistance, fraud alerts, dark web scanning, and more. The tools are varied and sophisticated, reflecting the complexity of the world in which we live.

Beyond technological solutions and legal measures, personal responsibility plays a crucial role in safeguarding against identity theft. Regularly reviewing financial statements, setting up account alerts, and maintaining a well-organized record of financial documents can add another layer of protection. Sound financial planning, coupled with vigilant personal practices, complements the technological and legal defenses, adding another layer to the fortress of security.

Wrapping Up

From basic steps like robust password management to the embrace of comprehensive tools such as identity theft protection software, the path to security is both intricate and essential. Keeping our wealth safe in this digital world isn’t just about one solution or approach. It’s about weaving together different strategies, tools, and ideas. We’re all part of this effort. We must work together with the shared goal of stopping identity theft.

Dealing with debt can be overwhelming, but with the right approach, you can regain control of your financial situation. One effective strategy for managing and eliminating debt is the Avalanche Method for Debt Repayment. This method offers a structured and strategic way to pay off your debts, allowing you to achieve financial freedom sooner.

In this article, we’ll explore the ins and outs of the Avalanche Method, how it works, and why it’s a powerful tool for achieving debt-free status.

What is the Avalanche Method?

The Avalanche Method, a strategic approach to debt repayment, hones in on tackling debts with the highest interest rates as a top priority. Unlike the Snowball Method, which directs attention towards clearing smaller debts irrespective of interest rates, the Avalanche Method takes a more calculated route.

Its core objective is to significantly reduce the overall interest payments over the course of repayment, thus ultimately leading to substantial savings and a faster journey to debt freedom.

Imagine your debts as a series of slopes, each with its own interest rate representing the incline. The Avalanche Method focuses on conquering the steepest slopes first, where the interest rates are the highest.

This targeted approach makes financial sense because high-interest debts are often the ones that accumulate the most substantial interest charges over time. By knocking out these high-interest debts at the outset, you’re effectively preventing the accumulation of additional interest costs that could otherwise weigh down your financial progress.

This method’s strength lies in its mathematical precision. As you pay off high-interest debts early on, your overall debt load decreases more efficiently, enabling you to allocate more funds towards principal payments rather than interest payments.

With each high-interest debt you eliminate, you’re essentially freeing up more resources to tackle the remaining debts in a cascading effect.

How to Use the Avalanche Method to Pay Down Debt

The Avalanche Method offers a well-structured plan for conquering your debts with finesse. Using the Avalanche Method is easy – follow the steps below to knock out your debt:

- Gather Debt Information: The first step in effectively utilizing the Avalanche Method is to gather a comprehensive list of all your debts. This includes not only the outstanding balances of each debt but also their respective interest rates. This information forms the foundation upon which you’ll build your strategic debt repayment plan.

- Order by Interest Rate: With your debt information in hand, it’s time to arrange your debts in a specific order. The key here is to prioritize debts based on their interest rates, placing those with the highest rates at the top of the list. This strategic ranking is what sets the Avalanche Method apart—it’s all about targeting the financial fires that burn the hottest.

- Minimum Payments: While you’re focusing extra resources on the high-interest debts, it’s crucial not to neglect your other financial obligations. Continue making the minimum required payments on all your debts. This ensures that you’re fulfilling your commitments and maintaining a solid credit history.

- Extra Payments: Now comes the crux of the Avalanche Method—allocating your extra funds where they’ll make the most impact. Direct any additional money you can spare toward the debt that boasts the highest interest rate. This is where the avalanche effect comes into play. By channeling your resources towards the debt with the steepest interest, you’re essentially chipping away at the foundation of accumulated interest that could otherwise hinder your progress.

- Roll Over Payments: As you watch your high-interest debt diminish and eventually disappear, it’s time to harness that momentum. Once the highest-interest debt is triumphantly paid off, take the monthly payment that you were dedicating to it and roll it over to the next debt on your list. This tactic ensures that the payment snowball keeps rolling, growing in size and strength as it moves down your list of debts.

Picture it as a snowball gaining momentum and size as it rolls downhill, gathering more snow and power. Similarly, your debt payments become a powerful force, gaining more and more strength as you eliminate each debt in succession.

The Avalanche Method is not just about repayment—it’s about optimization. It’s about using every resource you have to your advantage, cutting through the financial underbrush to clear a path to financial freedom. It’s a method that makes you the architect of your financial journey, leveraging the power of mathematics and strategy to achieve your goals.

By following these steps and focusing on high-interest debts, you’re not just paying off balances; you’re minimizing the weight of interest on your shoulders and fast-tracking your way to a debt-free future.

The Avalanche Effect in Action

The term “avalanche” conjures up images of immense snowslides cascading down mountainsides with unstoppable force, transforming the landscape in their wake. Just as nature’s avalanches hold immense power, the financial world has its own version of this phenomenon—the “Avalanche Effect.”

This effect lies at the core of the Avalanche Method for debt repayment, and understanding its mechanics can empower you to take control of your financial journey like never before.

Visualizing the Avalanche Effect

Imagine standing at the peak of a mountain, looking down at a series of slopes adorned with varying amounts of snow.

Each slope represents a different debt in your financial landscape, while the snow symbolizes the interest charges that accumulate over time. At the base of these slopes lies your ultimate goal: debt freedom.

Now, envision starting your descent by taking on the steepest slope first—the one adorned with the most snow. This slope mirrors the debt with the highest interest rate. As you make payments and steadily chip away at this debt, you’re not only reducing its balance but also diminishing the accumulating interest.

This is the Avalanche Effect in action.

The Power of Prioritization

The Avalanche Effect operates on the principle of strategic prioritization. Just as an avalanche targets the most vulnerable points on a mountainside, the Avalanche Method homes in on high-interest debts—the areas of your financial landscape where the interest accrues most rapidly.

By tackling these debts head-on, you’re effectively preventing a snowballing effect of interest buildup that could otherwise slow your progress.

The Momentum Multiplier

As you successfully conquer the highest-interest debt, something remarkable happens—the momentum you’ve built begins to amplify. Picture the rolling snowball in a traditional debt snowball method.

Now imagine that snowball gaining momentum, transforming into a boulder, and barreling down the slopes with even more vigor. This amplification occurs as the funds that were previously allocated to the paid-off debt are redirected to the next highest-interest debt on your list.

A Cascade of Financial Gains

With each debt you eliminate, the Avalanche Effect continues to gather force. You’re essentially freeing up more resources—previously locked into interest payments—to directly attack your debts’ principal balances. This cascade effect propels you toward your goal of becoming debt-free at an accelerated pace.

The Avalanche Effect is meticulously crafted strategy that harnesses the power of prioritization, focus, and momentum.

By targeting high-interest debts and diligently adhering to the Avalanche Method, you’re positioning yourself to conquer your financial landscape with the precision of an expert mountaineer.

The Avalanche Effect ensures that your journey to debt freedom is not only efficient but also empowering, allowing you to sculpt a financial landscape that aligns with your goals and aspirations.

Just as an avalanche reshapes the terrain it touches, the Avalanche Effect reshapes your financial future, paving the way for a brighter, more liberated tomorrow.

Advantages of the Avalanche Method

When it comes to repaying money you owe, the Avalanche Method has some great advantages. Let’s break down these benefits in simple terms to see how this method can really help you.

Saving Money on Interest

The Avalanche Method works like a smart money saver. Imagine you borrow money and you have to pay extra money on top of it – that’s called “interest.” Some debts make you pay a lot of interest, and the Avalanche Method helps you avoid paying too much.

Think of it this way: If you have a credit card debt with high interest, and you take a long time to pay it off, the interest makes your debt bigger.

But with the Avalanche Method, you start by paying off the debts with the highest interest. This stops the interest from making your debt grow too much, so you end up saving more of your money.

Faster and Easier

Imagine you have a bunch of debts that you want to get rid of. Some debts are bigger troublemakers than others. The Avalanche Method gives you a clever way to deal with the biggest troublemakers first.

Being efficient means doing things in a smart and quick way. The Avalanche Method is super efficient because it helps you finish paying off all your debts faster.

By focusing on the debts that make you pay a lot of interest, you’re getting rid of the pesky ones first. This frees up more money that you can use to pay off the other debts, making your journey to being debt-free quicker and smoother.

Staying Motivated

Paying off debt can sometimes feel like a long journey. The Avalanche Method adds an interesting twist that keeps you motivated. Imagine if you could see your debts getting smaller and smaller. When you pay off the debts with high interest rates, you feel great because you’re making real progress.

This positive feeling doesn’t just disappear—it stays with you and keeps you going. It helps you stick to your plan and feel more confident. Every time you say goodbye to a high-interest debt, you’re not only reducing what you owe, but you’re also building a strong sense of achievement that pushes you forward.

The Avalanche Method isn’t like a superhero, but it does have three great benefits: it saves you money by avoiding high interest, helps you pay off debts faster, and keeps you motivated by showing your progress.

By using this method, you’re not just getting rid of debts; you’re paving the way for a better financial future.

Alternatives to the Avalanche Method

While the Avalanche Method is a powerful strategy for paying off debts, it’s not the only road to financial freedom. Let’s take a closer look at some alternative methods that can also help you conquer your debts and regain control of your finances.

Snowball Method: The Small Wins Approach

The Snowball Method is another popular debt repayment strategy that takes a different approach.

Instead of focusing on interest rates, it prioritizes paying off the smallest debts first. This method aims to provide quick wins by clearing away small debts, which can be motivating and create a sense of accomplishment.

The idea is simple: as you pay off smaller debts, you gain momentum and motivation to tackle larger ones.

While you may end up paying more in interest compared to the Avalanche Method, the emotional boost from crossing debts off your list can be a strong motivator.

Debt Consolidation: Streamlining Your Debts

Debt consolidation involves combining multiple debts into a single loan. This can make managing your debts simpler, as you’ll only have one monthly payment to worry about.

Consolidation can also potentially lower your interest rate if you qualify for a loan with better terms. It’s worth noting that while consolidation can make your financial life more organized, it doesn’t inherently address the interest savings focus of the Avalanche Method.

Balance Transfer: Shifting High-Interest Debt

Balance transfer involves moving high-interest credit card debt to a new card with a lower or 0% introductory interest rate. This can provide temporary relief from high interest, allowing you to focus on paying down the principal balance.

However, these promotional rates often expire after a certain period, so it’s important to have a repayment plan in place.

Hybrid Approach: Combining Strategies

You don’t have to pick just one method—sometimes a hybrid approach can work best.

For example, you might start with the Avalanche Method to tackle high-interest debts that drain your wallet, and then transition to the Snowball Method to gain psychological wins. Or, you could consolidate debts and then use the Avalanche Method to pay off the consolidated loan faster.

Professional Help: Financial Guidance

If managing your debts feels overwhelming, seeking help from financial experts or credit counseling agencies is a viable option. They can assess your situation and recommend a strategy tailored to your needs, which might combine elements from various methods. This personalized guidance can provide clarity and a clear path forward.

The Avalanche Method is a strong contender in the realm of debt repayment strategies, but it’s important to explore different paths to find what works best for you. Each alternative has its own strengths and considerations, and your choice should align with your financial goals, personality, and circumstances.

Whether you opt for the Avalanche Method, the Snowball Method, or a unique blend of strategies, the key is to take proactive steps toward a debt-free future and achieve lasting financial well-being.

Conclusion

The Avalanche Method for Debt Repayment is a powerful strategy for regaining control of your finances and achieving freedom from debt.

By prioritizing high-interest debts and following a structured plan, you can save money on interest and reach your debt-free goals sooner.

Investing is a powerful way to grow your wealth, but it can also be daunting, especially for newcomers to the financial world. One strategy that has gained immense popularity and is often touted as a beginner-friendly approach is dollar cost averaging (DCA).

In this article, we’ll delve into the concept of dollar cost averaging, how it works, its benefits, and whether it’s the right strategy for you.

What is Dollar Cost Averaging?

Dollar Cost Averaging is a savvy investment approach that empowers investors to navigate the ever-changing landscape of financial markets with poise and intelligence.

Picture this: rather than attempting to time the market’s highs and lows, this strategy champions the idea of consistency and steadfastness.

In practical terms, it involves committing a fixed sum of money into a chosen investment at regular intervals, irrespective of the current market price of the asset.

This method seizes the reins of market volatility and transforms it into a powerful tool for wealth accumulation.

Imagine for a moment that you’re investing a set amount, say $500, at predetermined intervals, be it monthly or quarterly.

Here’s where the beauty of Dollar Cost Averaging shines through: when the investment’s price is experiencing a dip, your fixed amount can snag more shares, amplifying your position.

Conversely, when the price surges, your fixed amount acquires fewer shares, ensuring that you don’t overextend during peak moments.

What truly sets Dollar Cost Averaging apart is its steadfast dedication to consistency. In a world often characterized by financial roller coasters, this strategy stands as a pillar of stability.

In essence, Dollar Cost Averaging is not merely a technique; it’s a philosophy. A philosophy that champions the power of consistency, resilience, and patient growth in the realm of investing.

It’s the antidote to impulsive decision-making, the remedy for the allure of market timing, and the blueprint for a financial future that’s as secure as it is prosperous.

How Dollar Cost Averaging Works

To understand how Dollar Cost Averaging operates, let’s explore a simple money-saving approach.

Imagine you’re setting aside $500 every month to invest in something valuable. Sometimes, the price of that valuable thing is high, so your $500 only gets a small portion of it.

Other times, the price is lower, and your $500 can secure more of it.

Over time, this method evens out the overall cost. It’s similar to calculating your average score from different school subjects. Even if you did really well in some subjects and not as well in others, your average score gives a fair sense of your performance.

Likewise, with Dollar Cost Averaging, the times when the valuable thing’s price is high don’t have a huge impact. And the times when it’s lower allow you to get more of it for your money.

As a result, your total cost becomes more stable, and you’re not overly influenced by the ups and downs of the valuable thing’s price fluctuations. The beauty of this approach is that you don’t need to be an expert or predict when the best time to invest is.

You simply keep putting away the same amount of money each month.

This steady strategy helps you accumulate more of the valuable thing without being overly concerned about its price constantly changing.

Benefits of Dollar Cost Averaging

The benefits of adopting the Dollar Cost Averaging strategy are indeed noteworthy.

Let’s delve into these advantages and shed light on how they can significantly shape your investment journey:

1. Reduced Impact of Market Volatility

Financial markets are notorious for their ups and downs, resembling a roller coaster ride at times.

One of the significant perks of Dollar Cost Averaging is its ability to cushion you from the jolts of these wild market swings. Imagine you’re on a boat in a sea with unpredictable waves.

Instead of being tossed around by each wave, Dollar Cost Averaging provides you with a sturdy sail that helps you navigate these fluctuations more smoothly.

2. Elimination of Timing Pressure

Timing the market is often seen as a daunting task, even for seasoned investors.

Trying to predict the perfect moment to buy or sell can be akin to catching lightning in a bottle.

Dollar Cost Averaging liberates you from this high-pressure game, offering you the tranquility of investing without the need to forecast market highs and lows.

3. Disciplined Approach

Investing is often as much about behavior as it is about numbers.

Developing a disciplined investment habit can make a world of difference in the long run.

Dollar Cost Averaging acts as your trusty guide, nudging you to stick to your investment plan regardless of external market noise.

4. Potential for Lower Average Costs

One of the remarkable aspects of Dollar Cost Averaging is its inherent potential to help you buy more when prices are lower.

Think of it as a savvy shopper who waits for a sale before making a purchase. When the market offers discounted prices, your fixed investment amount fetches you more shares, leading to a lower average cost per share over time.

To sum up, Dollar Cost Averaging is more than a strategy; it’s a toolkit that equips you to weather market storms, sidestep the anxiety of market timing, nurture financial discipline, and optimize your investment potential.

It’s a testament to the power of steady commitment and the art of making your money work for you over time.

Comparing Dollar Cost Averaging to Lump Sum Investing

Navigating the investment landscape often involves making choices that can impact your financial outcomes.

Two prominent approaches, Dollar Cost Averaging (DCA) and lump sum investing, stand at the crossroads of decision-making.

Let’s explore these methods with a practical example to illuminate their differences and potential benefits.

Dollar Cost Averaging (DCA)

Imagine you have $12,000 that you’re eager to invest in a stock market fund.

Instead of investing the entire sum all at once, you opt for Dollar Cost Averaging. Over the course of a year, you decide to invest $1,000 every month.

During this year, the market experiences both ups and downs.

Some months witness significant gains, while others display modest declines.

As a result, your monthly investments yield varying amounts of shares, corresponding to the fluctuating prices.

Lump Sum Investing

On the other hand, if you were to pursue lump sum investing, you’d deploy the entire $12,000 into the market at once.

This approach requires a confident prediction of an opportune moment to invest—a feat that even seasoned experts find challenging.

Let’s review the performance of both strategies over the year:

At the end of the year, the market has experienced moments of soaring highs and temporary dips.

With Dollar Cost Averaging, your monthly investments ensured that you bought more shares during price troughs and fewer shares during peaks.

This steady approach protected you from the full impact of market volatility.

Meanwhile, in the lump sum scenario, your initial investment of $12,000 was subject to the unpredictable timing of your entry into the market.

Depending on whether the market was on an upswing or downturn when you invested, your gains or losses could vary significantly.

Why Dollar Cost Averaging Can Be Better Than Lump Sum Investing

The beauty of Dollar Cost Averaging shines in its ability to counteract the uncertainty inherent in lump sum investing.

Instead of placing all your bets on a single moment, DCA disperses your investments over time, reducing the risk of entering the market at an inopportune juncture.

In a volatile market, such as the one in our example, Dollar Cost Averaging not only offers potential financial gains but also provides peace of mind.

It’s akin to taking measured steps through a rocky path instead of attempting a risky leap.

By adopting Dollar Cost Averaging, you not only stand a chance to potentially reap the rewards of market upswings but also mitigate the blow of market downturns.

This strategy underscores the significance of consistency and gradualism, shielding you from the turbulence of the financial world and increasing your likelihood of achieving your long-term investment goals.

Getting Started with Dollar Cost Averaging

Beginning your journey with Dollar Cost Averaging (DCA) is like laying the foundation for a sturdy financial house. This methodical approach to investing offers a roadmap to turn your aspirations into reality.

As you take your first steps, these carefully crafted steps will guide you toward successful implementation:

- Set Clear Financial Goals: Imagine you’re embarking on a cross-country road trip. Before you hit the road, you need to know where you’re headed and why. Similarly, define your financial goals. Are you saving for a future home, a comfortable retirement, or your child’s education? Having clear goals provides direction to your investments, ensuring that every dollar you put in has a purpose.

- Determine Investment Amount: Just as you budget for daily expenses, determine an amount you can consistently contribute to your investment journey. Think of this amount as the fuel that propels your financial vehicle forward. Choose a sum that comfortably fits within your budget, allowing you to remain consistent over time without compromising your other financial commitments.

- Select Investment Accounts: Think of investment accounts as the tools in your financial toolbox. Different goals require different tools. Whether it’s a retirement account, a brokerage account, or a combination of both, align your chosen accounts with your financial objectives. This step ensures that your investments are optimized to cater to your long-term plans.

- Choose Investments: Just as a chef curates ingredients for a recipe, research and select assets that align with your risk appetite and goals. Investigate different investment options such as stocks, bonds, or mutual funds. Diversification is like seasoning in a dish—it adds flavor and balance. Choose a mix of investments that reflects your desired level of risk and potential returns.

- Set Investment Intervals: Consider investment intervals as regular pit stops on your financial journey. Whether you’re driving cross-country or navigating investments, consistency is key. Choose how often you’ll contribute to your investments—monthly, quarterly, or semi-annually. Align these intervals with your financial rhythm and objectives, ensuring that your contributions are regular and steadfast.

- Stay Consistent with Your Investing: Just as a well-tuned engine keeps a vehicle running smoothly, consistency keeps your investment journey on track. Commit to your chosen investment intervals, regardless of market conditions. This steadfast approach ensures that your investments benefit from the ebb and flow of the market over time.

By following these steps, you’re setting the stage for a successful Dollar Cost Averaging strategy.

Remember, this approach is a dynamic one that can be tailored to fit your unique financial circumstances. Like a skilled navigator, Dollar Cost Averaging will guide you toward your financial destination, making each step a purposeful stride toward your financial aspirations.

Dollar Cost Averaging for Retirement Planning

Imagine crafting a masterpiece, stroke by stroke, over the course of your lifetime. Such is the artistry of Dollar Cost Averaging (DCA) when applied to retirement planning. This approach, akin to patiently building a mosaic, can serve as a powerful tool for cultivating a robust retirement nest egg.

The Power of Consistency

Retirement planning is a journey that requires meticulous preparation. Just as a skilled gardener tends to their plants, nurturing them over time, DCA enables you to consistently nurture your retirement savings. It’s not about rapid growth, but rather steady progress. Every contribution you make, whether it’s weekly, monthly, or annually, plays a role in cultivating the lush garden of your retirement fund.

Weathering the Market Seasons

Financial markets can be as unpredictable as the changing seasons. With DCA, however, you don’t need to predict which season will bring the best harvest. Instead, you’re equipped to navigate through various market conditions without being at the mercy of a single entry point. Your investments are like a diversified orchard, yielding fruit at different times, ultimately contributing to a bountiful retirement harvest.

Mitigating the Impact of Market Volatility

Picture this: as you sail towards retirement, you encounter turbulent market waters. DCA acts as a steady rudder, helping you navigate through market ups and downs without capsizing. It’s like having a safety net woven from consistent contributions. When prices are high, you acquire fewer shares, and when prices are low, you amass more. This gradual approach cushions the impact of market volatility, ensuring that your retirement plans stay on course.

The Compounding Effect