When you’re navigating the job market or budgeting for your future, knowing what your annual salary translates to in terms of an hourly wage can be incredibly helpful.

In this article, we’ll break down the math and explore what $44,000 a year means on an hourly basis.

We’ll also dive into related topics such as post-tax income, biweekly earnings, monthly income, and whether $44,000 a year can be considered a good salary. Plus, we’ll share tips on how you can potentially increase your hourly wage.

$44,000 a Year is How Much an Hour?

Determining how much an annual salary of $44,000 translates to on an hourly basis can provide a clearer perspective on your earnings. This calculation can be particularly useful when evaluating job offers, budgeting, or understanding the value of your time. To figure out your hourly wage from an annual salary, follow this straightforward formula:

$44,000 (annual income) / 52 (number of weeks in a year) / 40 (standard hours in a workweek) = $21.15 per hour

So, if you earn $44,000 a year, your hourly wage is approximately $21.15 before taxes. This calculation assumes you work a standard 40-hour workweek for all 52 weeks in a year.

Understanding your hourly rate is not just about the numbers; it can help you make informed financial decisions and plan your budget effectively. Whether you’re considering a job change, negotiating a raise, or simply curious about the value of your time, knowing your hourly wage is a valuable piece of financial information.

What is $44,000 a Year After Taxes?

Understanding your take-home pay is crucial when planning your finances. The amount you receive after taxes depends on various factors, including your tax filing status, deductions, and the state you reside in.

On average, individuals can expect to pay around 20-30% or more of their income in federal and state income taxes. Let’s take some data from the IRS website on what your tax rate will be according to your income. This does not account for any of the factors listed above.

- 37% for incomes over $578,125 ($693,750 for married couples filing jointly)

- 35% for incomes over $231,250 ($462,500 for married couples filing jointly)

- 32% for incomes over $182,100 ($364,200 for married couples filing jointly)

- 24% for incomes over $95,375 ($190,750 for married couples filing jointly)

- 22% for incomes over $44,725 ($89,450 for married couples filing jointly)

- 12% for incomes over $11,000 ($22,000 for married couples filing jointly)

So at a $44,000 annual income, we will assume a tax rate of 12%.

$44,000 (annual income) x 12% (tax rate) = $5,280

So, after taxes, you would have approximately $38,720 left as your annual income.

$44,000 a Year is How Much Biweekly?

Many employers pay their employees on a biweekly schedule, which means you receive a paycheck every two weeks. To calculate your biweekly income, you’ll need to divide your annual income by the number of pay periods in a year. Most often, there are 26 pay periods in a year for biweekly paychecks.

So, the calculation would look like this:

$44,000 (annual income) / 26 (biweekly pay periods) ≈ $1,692

At $44,000 a year, you would earn approximately $1,692 before taxes with each biweekly paycheck.

$44,000 a Year is How Much a Month?

If you’re curious about your monthly income at an annual rate of $44,000, you can calculate it by dividing your yearly income by 12 (since there are 12 months in a year):

$44,000 (annual income) / 12 (months) = $3,667

So, at a yearly salary of $44,000, your monthly income before taxes would be approximately $3,667.

Is $44,000 a Year a Good Salary?

Whether $44,000 a year is considered a good salary depends on various factors, including your location, cost of living, and personal financial goals. In some areas with a lower cost of living, $44,000 can provide a comfortable life. However, in more expensive cities, it may not stretch as far.

To determine if it’s sufficient for your needs, consider your monthly expenses, such as housing, utilities, transportation, groceries, and savings goals.

Additionally, factors like job benefits, opportunities for advancement, and job satisfaction play a significant role in evaluating the overall value of your wage.

Let’s take a look at how a $44,000 a year salary compares to others in the United States.

According to data from the US Census Bureau for 2022, the median income for Nonfamily households in the United States was approximately $45,440 – which means that half of all individuals earned more than this amount, and half earned less.

So, if you have a salary of $44,000, you have a salary that is in the bottom 50 percent of all earners in the United States.

How to Increase Your Hourly Wage

If you’re looking to boost your hourly wage, there are several strategies you can consider:

- Skill Development: Enhance your skills or acquire new ones that are in demand in your industry.

- Negotiation: When starting a new job or during performance reviews, don’t hesitate to negotiate your wage.

- Further Education: Consider pursuing additional education or certifications that can increase your market value.

- Job Switch: Sometimes, switching to a different job or company can lead to a significant salary increase.

- Freelancing or Part-Time Work: Explore part-time job opportunities or freelance work to supplement your primary income. Apps like Fiverr or Upwork can be a great spot to post your skills and get hired for part-time work.

- Start a Side Hustle: Look to make more money by starting a side hustle. The folks over at the blog, Financial Panther, have put together a comprehensive list of over 70+ gig economy apps, with strategies and thoughts on each one. A lot of these you can do from your phone. The list includes dog walking/sitting apps, food delivery apps, picture-taking apps, secret shopping apps, and plenty more. It is a great resource to see all the different side hustle apps that are out there.

Will a Salary of $44,000 Help Me Become Rich?

A salary of $44,000 can certainly help you build wealth and achieve financial success, but whether it will make you ‘rich’ depends on various factors, including your financial goals, lifestyle choices, expenses, and savings/investment strategies.

Here are some considerations:

- Financial Goals: The definition of “rich” varies from person to person. For some, it means achieving financial security and having enough to comfortably cover living expenses and retirement. For others, it means accumulating significant wealth. Your specific financial goals will determine what “rich” means to you.

- Lifestyle Choices: Your spending habits and lifestyle choices play a significant role in your ability to accumulate wealth. Even with a high salary, if you spend excessively or accumulate debt, it can hinder your path to becoming rich. Budgeting, practicing mindful spending, and living below your means are essential.

- Savings and Investments: Building wealth often involves saving a significant portion of your income and making smart investments. A high salary provides the opportunity to save and invest more, which can accelerate your wealth-building journey. Consider contributing to retirement accounts, investing in stocks or real estate, and diversifying your investments.

- Debt Management: Reducing and managing debt, such as student loans, credit card debt, and mortgages, is crucial for building wealth. High-interest debt can erode your financial progress, so it’s important to prioritize paying it off.

- Cost of Living: The cost of living in your area can significantly impact your ability to save and invest. In high-cost-of-living areas, it may be more challenging to build wealth, even with a high salary.

In summary, a $44,000 salary provides a solid foundation for building wealth, but it’s not the salary alone that determines your financial success. Becoming ‘rich’ is a subjective goal, so it’s essential to define what it means for you and create a financial plan to pursue it.

Conclusion

In conclusion, understanding what your annual salary translates to on an hourly basis can provide valuable insights into your financial situation. It’s not just about the number, but how it aligns with your financial goals, lifestyle, and location.

Remember, if you’re aiming for an increase in your hourly wage, there are steps you can take to make it happen.

When you’re navigating the job market or budgeting for your future, knowing what your annual salary translates to in terms of an hourly wage can be incredibly helpful.

In this article, we’ll break down the math and explore what $45,000 a year means on an hourly basis.

We’ll also dive into related topics such as post-tax income, biweekly earnings, monthly income, and whether $45,000 a year can be considered a good salary. Plus, we’ll share tips on how you can potentially increase your hourly wage.

$45,000 a Year is How Much an Hour?

Determining how much an annual salary of $45,000 translates to on an hourly basis can provide a clearer perspective on your earnings. This calculation can be particularly useful when evaluating job offers, budgeting, or understanding the value of your time. To figure out your hourly wage from an annual salary, follow this straightforward formula:

$45,000 (annual income) / 52 (number of weeks in a year) / 40 (standard hours in a workweek) = $21.63 per hour

So, if you earn $45,000 a year, your hourly wage is approximately $21.63 before taxes. This calculation assumes you work a standard 40-hour workweek for all 52 weeks in a year.

Understanding your hourly rate is not just about the numbers; it can help you make informed financial decisions and plan your budget effectively. Whether you’re considering a job change, negotiating a raise, or simply curious about the value of your time, knowing your hourly wage is a valuable piece of financial information.

What is $45,000 a Year After Taxes?

Understanding your take-home pay is crucial when planning your finances. The amount you receive after taxes depends on various factors, including your tax filing status, deductions, and the state you reside in.

On average, individuals can expect to pay around 20-30% or more of their income in federal and state income taxes. Let’s take some data from the IRS website on what your tax rate will be according to your income. This does not account for any of the factors listed above.

- 37% for incomes over $578,125 ($693,750 for married couples filing jointly)

- 35% for incomes over $231,250 ($462,500 for married couples filing jointly)

- 32% for incomes over $182,100 ($364,200 for married couples filing jointly)

- 24% for incomes over $95,375 ($190,750 for married couples filing jointly)

- 22% for incomes over $44,725 ($89,450 for married couples filing jointly)

- 12% for incomes over $11,000 ($22,000 for married couples filing jointly)

So at a $45,000 annual income, we will assume a tax rate of 22%.

$45,000 (annual income) x 22% (tax rate) = $9,900

So, after taxes, you would have approximately $35,100 left as your annual income.

$45,000 a Year is How Much Biweekly?

Many employers pay their employees on a biweekly schedule, which means you receive a paycheck every two weeks. To calculate your biweekly income, you’ll need to divide your annual income by the number of pay periods in a year. Most often, there are 26 pay periods in a year for biweekly paychecks.

So, the calculation would look like this:

$45,000 (annual income) / 26 (biweekly pay periods) ≈ $1,731

At $45,000 a year, you would earn approximately $1,731 before taxes with each biweekly paycheck.

$45,000 a Year is How Much a Month?

If you’re curious about your monthly income at an annual rate of $45,000, you can calculate it by dividing your yearly income by 12 (since there are 12 months in a year):

$45,000 (annual income) / 12 (months) = $3,750

So, at a yearly salary of $45,000, your monthly income before taxes would be approximately $3,750.

Is $45,000 a Year a Good Salary?

Whether $45,000 a year is considered a good salary depends on various factors, including your location, cost of living, and personal financial goals. In some areas with a lower cost of living, $45,000 can provide a comfortable life. However, in more expensive cities, it may not stretch as far.

To determine if it’s sufficient for your needs, consider your monthly expenses, such as housing, utilities, transportation, groceries, and savings goals.

Additionally, factors like job benefits, opportunities for advancement, and job satisfaction play a significant role in evaluating the overall value of your wage.

Let’s take a look at how a $45,000 a year salary compares to others in the United States.

According to data from the US Census Bureau for 2022, the median income for Nonfamily households in the United States was approximately $45,440 – which means that half of all individuals earned more than this amount, and half earned less.

So, if you have a salary of $45,000, you have a salary that is in the bottom 50 percent of all earners in the United States.

How to Increase Your Hourly Wage

If you’re looking to boost your hourly wage, there are several strategies you can consider:

- Skill Development: Enhance your skills or acquire new ones that are in demand in your industry.

- Negotiation: When starting a new job or during performance reviews, don’t hesitate to negotiate your wage.

- Further Education: Consider pursuing additional education or certifications that can increase your market value.

- Job Switch: Sometimes, switching to a different job or company can lead to a significant salary increase.

- Freelancing or Part-Time Work: Explore part-time job opportunities or freelance work to supplement your primary income. Apps like Fiverr or Upwork can be a great spot to post your skills and get hired for part-time work.

- Start a Side Hustle: Look to make more money by starting a side hustle. The folks over at the blog, Financial Panther, have put together a comprehensive list of over 70+ gig economy apps, with strategies and thoughts on each one. A lot of these you can do from your phone. The list includes dog walking/sitting apps, food delivery apps, picture-taking apps, secret shopping apps, and plenty more. It is a great resource to see all the different side hustle apps that are out there.

Will a Salary of $45,000 Help Me Become Rich?

A salary of $45,000 can certainly help you build wealth and achieve financial success, but whether it will make you ‘rich’ depends on various factors, including your financial goals, lifestyle choices, expenses, and savings/investment strategies.

Here are some considerations:

- Financial Goals: The definition of “rich” varies from person to person. For some, it means achieving financial security and having enough to comfortably cover living expenses and retirement. For others, it means accumulating significant wealth. Your specific financial goals will determine what “rich” means to you.

- Lifestyle Choices: Your spending habits and lifestyle choices play a significant role in your ability to accumulate wealth. Even with a high salary, if you spend excessively or accumulate debt, it can hinder your path to becoming rich. Budgeting, practicing mindful spending, and living below your means are essential.

- Savings and Investments: Building wealth often involves saving a significant portion of your income and making smart investments. A high salary provides the opportunity to save and invest more, which can accelerate your wealth-building journey. Consider contributing to retirement accounts, investing in stocks or real estate, and diversifying your investments.

- Debt Management: Reducing and managing debt, such as student loans, credit card debt, and mortgages, is crucial for building wealth. High-interest debt can erode your financial progress, so it’s important to prioritize paying it off.

- Cost of Living: The cost of living in your area can significantly impact your ability to save and invest. In high-cost-of-living areas, it may be more challenging to build wealth, even with a high salary.

Conclusion

In conclusion, understanding what your annual salary translates to on an hourly basis can provide valuable insights into your financial situation. It’s not just about the number, but how it aligns with your financial goals, lifestyle, and location.

Remember, if you’re aiming for an increase in your hourly wage, there are steps you can take to make it happen.

When you’re navigating the job market or budgeting for your future, knowing what your annual salary translates to in terms of an hourly wage can be incredibly helpful.

In this article, we’ll break down the math and explore what $46,000 a year means on an hourly basis.

We’ll also dive into related topics such as post-tax income, biweekly earnings, monthly income, and whether $46,000 a year can be considered a good salary. Plus, we’ll share tips on how you can potentially increase your hourly wage.

$46,000 a Year is How Much an Hour?

Determining how much an annual salary of $46,000 translates to on an hourly basis can provide a clearer perspective on your earnings. This calculation can be particularly useful when evaluating job offers, budgeting, or understanding the value of your time. To figure out your hourly wage from an annual salary, follow this straightforward formula:

$46,000 (annual income) / 52 (number of weeks in a year) / 40 (standard hours in a workweek) = $22.12 per hour

So, if you earn $46,000 a year, your hourly wage is approximately $22.12 before taxes. This calculation assumes you work a standard 40-hour workweek for all 52 weeks in a year.

Understanding your hourly rate is not just about the numbers; it can help you make informed financial decisions and plan your budget effectively. Whether you’re considering a job change, negotiating a raise, or simply curious about the value of your time, knowing your hourly wage is a valuable piece of financial information.

What is $46,000 a Year After Taxes?

Understanding your take-home pay is crucial when planning your finances. The amount you receive after taxes depends on various factors, including your tax filing status, deductions, and the state you reside in.

On average, individuals can expect to pay around 20-30% or more of their income in federal and state income taxes. Let’s take some data from the IRS website on what your tax rate will be according to your income. This does not account for any of the factors listed above.

- 37% for incomes over $578,125 ($693,750 for married couples filing jointly)

- 35% for incomes over $231,250 ($462,500 for married couples filing jointly)

- 32% for incomes over $182,100 ($364,200 for married couples filing jointly)

- 24% for incomes over $95,375 ($190,750 for married couples filing jointly)

- 22% for incomes over $44,725 ($89,450 for married couples filing jointly)

- 12% for incomes over $11,000 ($22,000 for married couples filing jointly)

So at a $46,000 annual income, we will assume a tax rate of 22%.

$46,000 (annual income) x 22% (tax rate) = $10,120

So, after taxes, you would have approximately $35,880 left as your annual income.

$46,000 a Year is How Much Biweekly?

Many employers pay their employees on a biweekly schedule, which means you receive a paycheck every two weeks. To calculate your biweekly income, you’ll need to divide your annual income by the number of pay periods in a year. Most often, there are 26 pay periods in a year for biweekly paychecks.

So, the calculation would look like this:

$46,000 (annual income) / 26 (biweekly pay periods) ≈ $1,769

At $46,000 a year, you would earn approximately $1,769 before taxes with each biweekly paycheck.

$46,000 a Year is How Much a Month?

If you’re curious about your monthly income at an annual rate of $46,000, you can calculate it by dividing your yearly income by 12 (since there are 12 months in a year):

$46,000 (annual income) / 12 (months) = $3,833

So, at a yearly salary of $46,000, your monthly income before taxes would be approximately $3,833.

Is $46,000 a Year a Good Salary?

Whether $46,000 a year is considered a good salary depends on various factors, including your location, cost of living, and personal financial goals. In some areas with a lower cost of living, $46,000 can provide a comfortable life. However, in more expensive cities, it may not stretch as far.

To determine if it’s sufficient for your needs, consider your monthly expenses, such as housing, utilities, transportation, groceries, and savings goals.

Additionally, factors like job benefits, opportunities for advancement, and job satisfaction play a significant role in evaluating the overall value of your wage.

Let’s take a look at how a $46,000 a year salary compares to others in the United States.

According to data from the US Census Bureau for 2022, the median income for Nonfamily households in the United States was approximately $45,440 – which means that half of all individuals earned more than this amount, and half earned less.

So, if you have a salary of $46,000, you have a salary that is in the top 50 percent of all earners in the United States.

How to Increase Your Hourly Wage

If you’re looking to boost your hourly wage, there are several strategies you can consider:

- Skill Development: Enhance your skills or acquire new ones that are in demand in your industry.

- Negotiation: When starting a new job or during performance reviews, don’t hesitate to negotiate your wage.

- Further Education: Consider pursuing additional education or certifications that can increase your market value.

- Job Switch: Sometimes, switching to a different job or company can lead to a significant salary increase.

- Freelancing or Part-Time Work: Explore part-time job opportunities or freelance work to supplement your primary income. Apps like Fiverr or Upwork can be a great spot to post your skills and get hired for part-time work.

- Start a Side Hustle: Look to make more money by starting a side hustle. The folks over at the blog, Financial Panther, have put together a comprehensive list of over 70+ gig economy apps, with strategies and thoughts on each one. A lot of these you can do from your phone. The list includes dog walking/sitting apps, food delivery apps, picture-taking apps, secret shopping apps, and plenty more. It is a great resource to see all the different side hustle apps that are out there.

Will a Salary of $46,000 Help Me Become Rich?

A salary of $46,000 can certainly help you build wealth and achieve financial success, but whether it will make you ‘rich’ depends on various factors, including your financial goals, lifestyle choices, expenses, and savings/investment strategies.

Here are some considerations:

- Financial Goals: The definition of “rich” varies from person to person. For some, it means achieving financial security and having enough to comfortably cover living expenses and retirement. For others, it means accumulating significant wealth. Your specific financial goals will determine what “rich” means to you.

- Lifestyle Choices: Your spending habits and lifestyle choices play a significant role in your ability to accumulate wealth. Even with a high salary, if you spend excessively or accumulate debt, it can hinder your path to becoming rich. Budgeting, practicing mindful spending, and living below your means are essential.

- Savings and Investments: Building wealth often involves saving a significant portion of your income and making smart investments. A high salary provides the opportunity to save and invest more, which can accelerate your wealth-building journey. Consider contributing to retirement accounts, investing in stocks or real estate, and diversifying your investments.

- Debt Management: Reducing and managing debt, such as student loans, credit card debt, and mortgages, is crucial for building wealth. High-interest debt can erode your financial progress, so it’s important to prioritize paying it off.

- Cost of Living: The cost of living in your area can significantly impact your ability to save and invest. In high-cost-of-living areas, it may be more challenging to build wealth, even with a high salary.

In summary, a $46,000 salary provides a solid foundation for building wealth, but it’s not the salary alone that determines your financial success. Becoming ‘rich’ is a subjective goal, so it’s essential to define what it means for you and create a financial plan to pursue it.

Conclusion

In conclusion, understanding what your annual salary translates to on an hourly basis can provide valuable insights into your financial situation. It’s not just about the number, but how it aligns with your financial goals, lifestyle, and location.

Remember, if you’re aiming for an increase in your hourly wage, there are steps you can take to make it happen.

Are you on the relentless quest of searching for apartments for rent, yet struggling to find the ideal haven that suits your desires? We comprehend that scouring the rental market can be a formidable challenge, riddled with complexities and tough choices.

When searching for an ideal apartment, anticipate undergoing a tenant background check as well. This is a crucial step in evaluating the trustworthiness and suitability of potential renters. Such checks may delve into areas like your credit score, any criminal past, and previous rental experiences, equipping landlords with the necessary insights to decide wisely.

Yet, with the right strategy, this journey can transform from a tedious chore into an exhilarating adventure. Whether you’re a seasoned renter or a first-timer, our article will equip you with the insights to transform your rental search into a successful and fulfilling venture.

Weighing the Affordability Versus the Quality of the Apartment

As you venture through the diverse range of apartments for rent, striking the right equilibrium between affordability and apartment quality becomes of utmost importance. While a lower rental cost may initially appear enticing, compromising on apartment quality could result in a less than desirable living experience. Evaluating aspects such as the apartment’s condition, available amenities, and its proximity to essential amenities is crucial.

On the other hand, opting for a higher-quality apartment with exceptional features and facilities may necessitate a more substantial budget. It is essential to gauge whether the additional expenses are justified by the enhanced benefits and ultimately contribute to an improved overall lifestyle.

Achieving the perfect match between affordability and apartment quality is pivotal to finding an apartment that genuinely resonates with your lifestyle. Diligent research, thorough comparison, and thoughtful consideration of your preferences will guide you towards making an informed decision that aligns with your unique needs and desires.

Access to Recreational and Outdoor Spaces

As you explore the diverse selection of apartments for rent, giving prominence to the availability of recreational and outdoor spaces becomes paramount. Proximity to parks, trails, and green areas opens a gateway to a plethora of invigorating outdoor activities, ranging from jogging and cycling to leisurely walks and picnics.

Residing in a community that boasts on-site amenities such as swimming pools, fitness centers, and sports courts elevates your lifestyle and fosters a culture of health and well-being. These spaces provide not only physical benefits but also offer opportunities for social interactions and community engagement.

Moreover, access to recreational spaces can enhance your work-life balance, offering moments of relaxation and rejuvenation amidst the serenity of nature.

By prioritizing recreational and outdoor amenities, you create an environment that perfectly aligns with your preference for an active and nature-immersed lifestyle. This enriches your daily experiences and shapes a home where you can flourish and embrace life’s joys to the fullest.

Understanding Tenant Rights

As you explore the multitude of apartments for rent, delving into the complexities of lease agreements and terms becomes crucial. This knowledge empowers you to make informed decisions while safeguarding your rights throughout the rental process.

Comprehending tenant rights entails a comprehensive grasp of essential aspects, including privacy safeguards, adherence to fair housing practices, and an understanding of regulations governing security deposits. Moreover, being well-versed in your rights concerning repairs and maintenance ensures that your living conditions remain optimal during the entire lease duration.

An often overlooked but significant facet is the right to reasonable accommodations for individuals with disabilities, ensuring that your living space caters to your unique needs and comfort.

Weighing the Pros And Cons of Furnished And Unfurnished Options

In the pursuit of unearthing an apartment that seamlessly suits your lifestyle, renters must engage in mindful reflection on the pros and cons of furnished and unfurnished options. This thoughtful consideration ensures that your new living space not only fulfills your practical needs but also aligns with your unique preferences and style.

As you navigate the diverse landscape of apartments for rent, carefully weighing the benefits and drawbacks of furnished and unfurnished choices becomes paramount. Furnished apartments offer the convenience of immediate occupancy, saving you the time and effort of furnishing the place yourself. They are especially appealing for those seeking a temporary living arrangement or embracing a minimalist lifestyle.

On the other hand, unfurnished apartments grant you the liberty to infuse your living space with your personal touch. This option is perfect for individuals with cherished furniture and belongings or those envisioning a long-term residence where they can establish a sense of belonging and individuality.

Taking the financial aspect into account is equally crucia. While furnished apartments may entail higher upfront costs, unfurnished options may require additional expenses for furnishing the space according to your taste.

Considering your current lifestyle and future plans is a key factor in making an informed decision. Frequent movers or those seeking flexibility may find furnished apartments more fitting, while those desiring a stable and personalized environment might lean toward unfurnished options.

Considering the Advantages And Disadvantages of Living With Roommates

As you explore the diverse range of apartments for rent, it becomes crucial to contemplate the benefits and drawbacks of sharing a living space with roommates. The prospect of splitting rent and utilities among occupants can significantly alleviate financial burdens. Additionally, cohabiting can foster companionship and emotional support, creating a sense of community within the apartment.

However, it is essential to recognize that co-living arrangements may also present challenges. Differences in schedules, lifestyles, and habits could lead to conflicts, necessitating effective communication and a willingness to compromise. Maintaining personal space and privacy may require setting clear boundaries and demonstrating mutual respect.

Understanding your own preferences and social dynamics is pivotal in making an informed decision. Some individuals thrive in communal living environments, cherishing the camaraderie, while others value the autonomy of living alone.

Finding the right mortgage lenders is crucial when it comes to buying a home. The best lender for you will offer you the competitive rates and customer service that you’re looking for with a variety of loan options on the table that you can benefit from.

Mortgage lenders work to ensure that you get the very best for your circumstances, and some of the benefits of using a mortgage lender include the following:

Benefits of Mortgage Lenders

Access to Loan Options

Mortgage lenders offer a range of loan options depending on your financial situation and goals for home ownership. Whether you are a first-time buyer or you are experienced in home ownership and want to refinance, mortgage lenders can help.

Excellent Interest Rates

Mortgage lenders will often have better access to competitive interest rates. These can save you money over time, especially over the life of the loan. When you shop around, you can compare rates from various lenders and choose the best one for your situation.

Personal Guidance

A mortgage lender can help you throughout the home-buying process, and it is crucial that you understand your options. They can explain the terms and conditions of a loan to you while answering your questions and providing you with the guidance you need throughout each step.

Faster Loan Approval

Mortgage lenders work to efficiently process the loan and approve it as quickly as possible. They’ll help you move through the process and provide pre-approval, which can strengthen your offer.

How to Find the Best Mortgage Lender

There are many ways to find the best mortgage lender for your needs. Some of those tips include:

Researching Lenders

Look for lenders with positive reviews and a good reputation. These are the ones to watch for, and you should consider asking family and friends for their recommendations.

Compare the Available Rates

You can know that you’re getting the best possible deal by comparing interest rates from multiple lenders. Your rates will depend on the current loan amount, the down payment available, and your credit score, so keep an eye on that.

Think about Your Loan Options

There are plenty of loan options so find a mortgage lender that offers a range of options. This can include everything from fixed-rate mortgages to adjustable-rate mortgages. Choose a lender that can offer you a product that matches your financial goals.

Get Professional Advice

Always consider working with lenders who can offer you advice on the process. You want to feel secure when you are buying your first home, and a mortgage lender can help you through it.

By taking the time to evaluate your mortgage options, you will receive the best possible support when securing your mortgage. The right mortgage lender will ensure that you get the right support throughout, and you will soon be signing on the dotted line for your new home.

Life throws curveballs. While we can plan for many things, unexpected legal issues can arise, causing stress, disrupting our lives, and potentially leading to significant financial burdens. The prospect of legal fees can be daunting, particularly for individuals or families living on a budget. However, by incorporating the possibility of legal expenses into your financial planning and adopting smart strategies, you can be better prepared to weather these storms.

This article explores the challenges of budgeting for unexpected legal expenses and offers practical solutions to ensure you have a legal lifeline in times of need.

Building a Safety Net for Legal Emergencies

A cornerstone of sound financial planning is having a rainy day fund – a financial cushion to cover unforeseen expenses. While emergencies often involve car repairs, medical bills, or unexpected job loss, including a reserve specifically for potential legal issues is crucial.

Understanding Your Risk Profile

Not everyone faces the same legal risks. Consider your lifestyle, profession, and potential vulnerabilities. For example, if you own property, the risk of a legal dispute with a neighbor might be higher compared to someone living in an apartment. Similarly, certain professions might carry inherent legal risks (e.g., construction workers and healthcare professionals), while others are dependent on the securing of licenses, the process of which can be difficult and may require you to hire an attorney to ensure procurement. In the cases such as the latter, hiring a criminal lawyer that focuses on nursing licenses, if you work in this industry, for example, may be the way forward. After all, Nurse criminal lawyers can protect your record and your license, ensuring you remain in work and earn your monthly dues. Assessing your risk profile – taking stock of your personal interests and your employment – allows you to prioritize your legal safety net accordingly.

Calculating Your Reserve

There’s no one-size-fits-all answer for the ideal amount to set aside. Start by researching average legal fees associated with common issues in your area. This could include consultations, document preparation costs, or potential court filing fees. Factor in your risk profile and consider a realistic starting point. Even a modest amount saved consistently can provide a valuable buffer when legal issues arise.

Savings Strategies

Integrate saving for your legal safety net into your regular budgeting routine. Automatically transfer a small portion of your paycheck or set aside a fixed amount each month. Consider utilizing a separate savings account specifically earmarked for legal expenses. This will make it easier to track your progress and resist the temptation to dip into this reserve for other purposes.

Building a legal safety net is a marathon, not a sprint. Start small and gradually increase your reserve as your financial situation allows. Every dollar saved brings you closer to having a legal lifeline when you need it most.

Prioritizing Legal Needs

When faced with a legal issue, the first step is to assess its urgency and potential cost implications. Not all legal battles require the same level of resources or legal representation.

Here’s how to prioritize your legal needs:

- Immediate Threats to Your Safety or Well-Being: Issues that pose immediate danger to your physical safety or security (e.g., restraining order violations, domestic violence) should be addressed as quickly and decisively as possible. Seek legal representation immediately to ensure your safety and explore legal options to protect yourself.

- Financial Threats or Loss of Property: Legal issues affecting your finances or property rights (e.g., debt collection, contract disputes, property damage) require prompt attention but may allow for some exploration of options before taking legal action. Consider mediation or negotiation before resorting to litigation, which can be a lengthy and expensive process.

- Preventive Measures and Long-Term Benefits: While not urgent, investing in preventive legal measures like a will or power of attorney can save significant time, money, and emotional stress for you and your loved ones down the road.

By prioritizing your legal needs based on urgency, potential costs, and long-term impact, you can allocate your resources effectively and make informed decisions about how to approach each situation.

Exploring Legal Insurance Options

Legal insurance plans offer a potential solution for managing legal expenses. These plans typically involve paying a monthly or annual premium in return for access to a network of lawyers who provide legal services at pre-negotiated rates.

Here’s a closer look at legal insurance:

- Benefits of Legal Insurance: Legal insurance plans can provide peace of mind by offering readily available legal help for a predictable monthly cost. Covered services may include consultations, document review, and representation in certain legal matters.

- Limitations of Legal Insurance: Legal insurance plans often have limitations in coverage. Pre-existing legal issues might be excluded, and specific types of legal cases (e.g., criminal defense) might not be covered. Additionally, there may be caps on covered legal fees or limits on the number of consultations allowed per year.

- Choosing a Legal Insurance Plan: Carefully research different legal insurance providers before purchasing a plan. Compare coverage details, network of lawyers, and associated costs. Ensure the plan aligns with your specific needs and risk profile.

Legal insurance is not a one-size-fits-all solution, but it can be a valuable tool for budgeting for legal expenses. Consider it a safety net for common legal issues, but remember that you might still need to navigate exclusions or limitations in coverage for complex legal matters.

Finding Affordable Legal Help

While a legal safety net or insurance plan offers a good starting point, legal costs can still add up. Here are some creative strategies to manage these expenses effectively.

Numerous government agencies and non-profit organizations offer free or low-cost legal advice and representation in various areas. Local bar associations might also have legal aid programs for qualifying individuals. Alternatively, look online for affordable law firms (More here regarding this) on the Web or pro bono (free legal services) programs in your area. These resources can be invaluable for navigating legal issues without breaking the bank.

Consulting with a lawyer for a single session can also be highly beneficial. This allows you to understand your legal options, identify potential risks and cost implications, and develop a course of action. Armed with this knowledge, you can negotiate more effectively with the other party or decide if pursuing legal action is the best approach, potentially saving you money in the long run.

Instead of the traditional court system, consider alternative dispute resolution (ADR) options like mediation or arbitration. These processes involve a neutral third party who helps guide the parties toward a mutually agreeable solution. ADR can be significantly less expensive and time-consuming compared to litigation.

Building Peace of Mind on a Budget

Life’s legal curveballs can be challenging, but with a well-planned budget and some proactive strategies, you can be better prepared to face them. Building a legal safety net, exploring affordable legal resources, and taking preventive measures can significantly reduce the financial burden and stress associated with unexpected legal issues.

Remember, legal expertise doesn’t have to be a luxury. By planning your budget and seeking help strategically, you can ensure that legal expenses don’t derail your financial security. Having a legal lifeline in place can provide invaluable peace of mind and empower you to navigate life’s challenges confidently.

If you want to boost your economic financial savings, understanding just how beneficial bonus saving accounts work can be a game-changer. These accounts use an enticing method to make a higher rate of interest on your cost savings under specific problems. This post clarifies the essentials of benefit interest-bearing accounts just how they vary from typical interest-bearing accounts plus exactly how you can optimize your income by utilizing them properly.

What Are Bonus Savings Accounts?

Bonus saving accounts are a kind of interest-bearing account that financial institutions supply to incentivize clients to conserve even more cash. They generally use a greater interest rate contrasted to normal interest-bearing accounts.

Key Features of Bonus Savings Accounts

Below are some usual functions that specify bonus offer interest-bearing accounts:

- Greater Interest Rates: These accounts typically have a base rate of interest and also a perk interest rate. You gain the bonus price when you fulfill particular problems.

- Problem Requirements: You could be required to transfer a minimal quantity month-to-month and also make no withdrawals to make the bonus.

- Minimal Access: To dissuade withdrawals some financial institutions may limit accessibility to funds or web link high withdrawal charges with these accounts.

Understanding How These Accounts Work

Bonus interest-bearing accounts work with an easy concept: award savers forever conserving actions. Below’s just how they usually function:

- Open up an Account: You begin by opening up a bonus interest-bearing account with a financial institution that provides one.

- Fulfill the Conditions: You follow the details of problems like minimal down payments as well as no withdrawals.

- Gain Interest: If you satisfy these problems you make a greater rate of interest for that month.

Maximizing Your Interest Earnings: Tips and Strategies

To take advantage of your perk interest-bearing account think about the complying with approaches:

Regular Deposits

- Establish Automatic Transfers: Automate your regular monthly down payments to guarantee you constantly fulfill the minimal down payment demand.

- Enhance Your Deposits: Whenever feasible down payment greater than the minimum needed to speed up your cost savings development.

Minimal Withdrawals

- Emergency Situation Fund: Keep a different emergency situation fund to stay clear of withdrawals from your bonus interest-bearing account.

- Strategy Major Expenses: If you understand you’ll require cash in the future, strategy as necessary coupled with perhaps making use of an additional kind of representation of this function.

Keep Track of Account Rules

- Keep Informed: Always understand any kind of adjustments to the account problems or prices.

- Schedule Reminders: Set suggestions for the days through which you are required to make down payments or stay clear of withdrawals.

Review and Compare

- Search: Compare various incentive savings accounts to locate one with the most effective prices as well as problems that you can reasonably fulfill.

- Routine Reviews: Periodically assess your account to see if it still provides the very best ROI for your financial savings.

Benefits of Using Bonus Savings Accounts

Bonus savings accounts offer several advantages that can help you grow your savings effectively:

Higher Savings Potential

- Faster Growth: These accounts normally provide greater rates of interest contrasted to routine interest-bearing accounts. This suggests your cash can expand much faster gradually, enabling you to reach your economic objectives earlier.

- Making Best Use Of Returns: With perk interest-bearing accounts you can gain even more passion on your cost savings without taking on extra danger making it a clever option for making the most of your returns.

Encourages Saving Discipline

- Establishing a Habit: The requirements to qualify for the bonus interest rate often include actions like making regular deposits or maintaining a minimum balance. These conditions encourage a disciplined approach to saving, helping you build healthy financial habits.

- Motive to Save: Knowing that you can gain a perk interest rate by fulfilling specific standards can work as inspiration to continually conserve plus handle your funds properly.

Flexible Savings Option

- Ease of access: Unlike a few other financial investment choices like Certificates of Deposit (CDs), bonus interest-bearing accounts provide even more adaptability. You can access your funds whenever you require them without encountering charges for very early withdrawals.

- Stabilizing Accessibility plus Growth: While there are limitations to get the bonus price perk, interest-bearing accounts strike an equilibrium in between making affordable passion together with preserving accessibility to your cost savings for unpredicted costs or monetary objectives.

Incentive interest-bearing accounts give a chance to expand your financial savings quicker, imparting self-control, coupled with deal adaptability in accessing your funds when required. By capitalizing on these advantages plus fulfilling the account needs you can reconcile your cost savings approach plus job in the direction of accomplishing your economic purposes.

Common Pitfalls to Avoid

While bonus interest-bearing accounts provide benefits there are particular mistakes you need to watch out for:

Penalty for Non-Compliance

- Threat of Lower Interest: If you do not fulfill the demands established by the financial institution, such as preserving a minimal equilibrium or making normal down payments you might wind up making a substantially reduced rate of interest.

- Loss of Potential Earnings: Failing to adhere to the account problems can lead to missing out on the bonus passion lowering the general development of your financial savings.

Managing Multiple Accounts

- Intricacy: Having several bonus interest-bearing accounts can make it testing to monitor each account’s needs and also advantages.

- Streamline for Efficiency: Instead of spreading your cost savings throughout various accounts, think about settling them right into a couple of accounts using the most effective returns. This streamlines administration as well as guarantees you can satisfy the standards quicker.

Ignoring Changes in Terms and Rates

- Threat of Decreased Returns: Banks might change the terms plus the rate of interest of perk interest-bearing accounts with time. Failing to remain educated concerning these adjustments can cause your account to no longer supply affordable returns.

- Remain Informed: Regularly look for updates from your financial institution concerning any type of modifications to the account terms or rate of interest. This permits you to make educated choices concerning whether to proceed with the account or check out various other alternatives.

Understanding these typical mistakes related to bonus offer savings accounts can assist you optimize your revenues and also prevent possible problems. By remaining educated, streamlining your technique as well as sticking to account demands you can take advantage of your cost savings technique while decreasing threats.

Conclusion

Perk interest-bearing accounts can be an effective device for boosting your cost savings if made use of properly. By recognizing just how they function plus sticking to their problems you can optimize your passion incomes dramatically. Bear in mind the vital to success with these accounts is discipline, making normal down payments lessening withdrawals plus remaining educated concerning your account’s terms and conditions. Whether you’re conserving for a certain objective or simply seeking to expand your reserve these accounts give an useful source for handling and also expanding your funds efficiently

Selecting the ideal SEO services is crucial for enhancing your business’s visibility online. In this blog, we’ll explore the key steps and indicators known as Key Performance Indicators (KPIs) that you need to monitor to assess how effectively your SEO strategies are working. Understanding these indicators and recognizing them can ensure that the time and money you invest in SEO contribute positively to your business growth.

We’ll guide you on how to track and analyze these metrics so you can determine whether your SEO investment is paying off. It’s not just about attracting more visitors to your website; it’s about attracting the right kind of visitors who are more likely to convert into customers. By the end of this blog, you should have a clear understanding of what to look for in a high-quality SEO service, similar to SEO services in Brisbane, and how to tell if it’s effectively meeting your specific business needs.

What is SEO?

SEO stands for Search Engine Optimization. It is a means to make your website a whole lot much more noticeable when people look for points on the web making use of online search engines like Google. The objective of SEO is to obtain your website to show up greater on the search results page. This is required because the greater your website prices the more likely individuals are to see it when they look for subjects concerning your website.

To achieve this, SEO implements various strategies, such as selecting the right keywords, optimizing website navigation, and ensuring fast loading times. These methods help search engines understand what your website is about and show it to users interested in your content. As a result, businesses across various industries leverage SEO to improve their online presence. For instance, law firms often seek out the best lawyer SEO companies to improve their search rankings and increase client inquiries.

Building on this approach, local service providers, like plumbers and electricians, use SEO techniques tailored to their specific needs, aiming to rank higher in regional searches. This targeted strategy drives more traffic to their websites by connecting them with potential customers in their area. So, with the help of this tool, businesses like yours can attract more visitors organically without relying solely on paid advertisements, ultimately enhancing your online visibility and potential customer base.

Introduction to SEO Metrics and KPIs

Before delving into particular metrics, it’s essential to comprehend that SEO success must straighten with your general service purposes. Whether it’s boosting brand name understanding, enhancing sales, or driving even more web traffic to your internet site your objectives must determine which metrics are essential to you.

Key SEO Metrics and KPIs to Track

1. Organic Traffic

What It Is: Organic web traffic describes site visitors that land on your website as an outcome of an overdue (natural) search results page.

Why It Matters:

- Sign of Visibility: Increases in natural website traffic indicate that your website is ending up being much more noticeable on online search engines.

- Top quality of SEO Work: Consistent development in natural website traffic is an excellent indication that SEO methods work.

2. Keyword phrase Rankings

What It Is: This metric tracks the positions of your website’s keywords on online search engine result web pages (SERPs).

Why It Matters:

- Efficiency Indicator: Improvements in keyword positions can cause enhanced natural web traffic.

- Targeted Visibility: This helps you see if you show up for the appropriate keywords that straighten your service objectives.

3. Conversion Rate

What It Is: Conversion price is the portion of site visitors to your website that finishes a wanted objective (a conversion) out of the overall variety of site visitors.

Why It Matters:

- Effectiveness of Traffic: High conversion prices show that your website not only brings in site visitors but likewise convinces them to act.

- Straight Business Impact: Provides a straight web link between SEO initiatives and also service results.

4. Bounce Rate

What It Is: Bounce price is the portion of site visitors that browse away from the website after checking out just one web page.

Why It Matters:

- User Engagement: A high bounce price may suggest that the web page isn’t appropriate to what site visitors are seeking or that the web page isn’t easy to use.

- Top quality of Traffic: Helps analyze the high quality of website traffic originating from natural search.

5. Backlinks Quality plus Quantity

What It Is: Backlinks are web links from one internet site to a web page on an additional internet site. Google as well as various other significant internet search engines take into consideration backlinks to enact support of a detailed web page which can enhance a website’s position on SERPs.

Why It Matters:

- Online Reputation Builder: More premium backlinks usually indicate greater credibility in the eyes of online search engines.

- SERP Boost: Helps in enhancing positions as well as by expanding natural web traffic.

6. Web Page Load Time

What It Is: Page lots time is the complete time considered a website to pack totally.

Why It Matters:

- Customer Experience: Faster web pages develop pleased individuals as well as can substantially decrease bounce price.

- SEO Ranking Factor: Page rate is additionally a ranking aspect for Google impacting your website’s exposure.

7. Click-Through Rate (CTR)

What It Is: CTR in SEO terms is the portion of individuals that click your web link after seeing your entrance in the search results page.

Why It Matters:

- Indicates Relevance: A greater CTR can show that your web page title plus summary relate to the target market.

- Influences SEO: Google thinks about CTR as a variable when establishing where to rate your web page.

Executing SEO Evaluation Strategies.

To properly gauge these KPIs take into consideration the complying with techniques:.

- Usage Comprehensive Tools: Utilize devices like Google Analytics, SEMrush, or Ahrefs to track and also evaluate these metrics.

- Normal Reporting: Create routine SEO reports to keep an eye on development and also change techniques as required.

- Straighten SEO Goals: Ensure that your SEO objectives are straightened with your total service goals for purposeful evaluation.

Conclusion

Determining the success of Search Engine Optimization services exceeds simply taking a look at just how high your website rates on the search results page or the number of individuals who see your website. It’s truly concerning seeing just how these numbers assist your service to make even more cash. To truly recognize if your SEO is functioning you are required to concentrate on the best Key Performance Indicators (KPIs) like sales numbers, the portion of site visitors that purchase something, or the amount of return clients you have.

Additionally, you must have a solid strategy to regularly inspect these signs to make certain that the cash you’re investing in SEO is aiding your organization’s expansion. If tracking these metrics and managing SEO feels overwhelming or time-consuming, don’t hesitate to partner with a trusted SEO company. They can provide the expertise and support needed to help your business thrive while handling the complexities of SEO for you.

SEO isn’t a fast solution; it’s a lasting method to making your website far better. This indicates you should not anticipate instant outcomes. SEO success ought to be checked out over a longer time, like numerous months or a year. This provides you a clearer photo of exactly how well your methods are functioning. By making the effort to gauge your outcomes very carefully you can make certain that your SEO initiatives work.

Power Grid Corporation of India Limited is a Schedule ‘A’, ‘Maharatna’ Public Sector Enterprise of the Government of India, founded on October 23, 1989, under the Company Act, 1956. Power Grid is a listed company, with 51.34% held by the Government of India, and the rest held by institutional investors and the public.

Power Grid has caught the attention of many discerning investors. As one of India’s leading power system companies, Power Grid Corporation of India Limited (Power Grid Corp) stands tall in power generation and distribution.

Power Grid Financial Analysis

For the quarter ending December 31, 2023, the firm reported a Consolidated Total Income of Rs 11,819.70 Crore, up 2.51% from the previous quarter’s Total Income of Rs 11,530.43 Crore and up 2.51% from the same quarter last year at Rs 11,530.22 Crore. In the last quarter, the company earned a net profit after tax of Rs 4,028.25 crore. The company spent 21.14% of its operational revenues on interest charges and 5.5% on labor costs in the fiscal year ending March 31, 2023.

In the following table, we have included the financial stats of the company for the year 2023. You can take a look and compare the stats on a quarter-by-quarter basis.

| Category | March 2023 | June 2023 | Sep 2023 | Dec 2023 |

| Sales | Rs. 11,494.90 Crores | Rs. 10,436.11 Crores | Rs. 10,419.41 Crores | Rs. 10,676.59 Crores |

| Expenses | Rs. 4573 Crores | Rs. 4497 Crores | Rs.4352 Crores | Rs. 4433 Crores |

| Operating Profit | Rs. 7,713.98 Crores | Rs. 6,584.28 Crores | Rs. 6,851.85 Crores | Rs. 7,033.02 Crores |

| Basic Earning per Share | 4.27 | 5.08 | 4.12 | 4.27 |

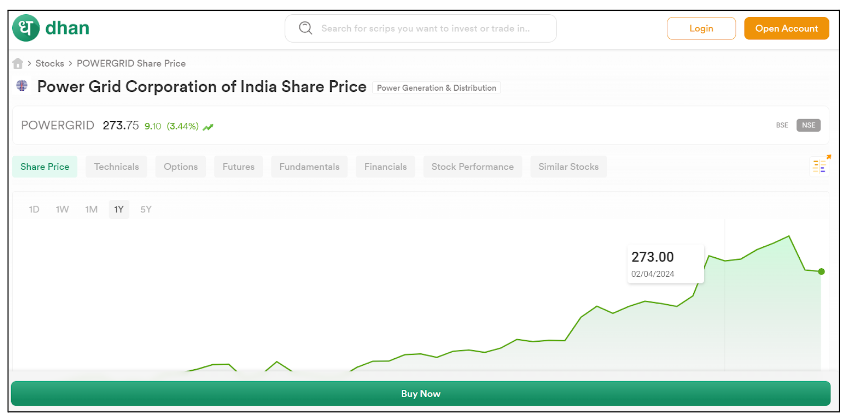

Power Grid Price Analysis

Compared to the last closing price, As of April ‘24 Power Grid share price is trading around Rs. 270+. Go through the following Power Grid share price chart for a better idea of its recent market trends.

Power Grid Corporation Of India’s TTM P/E ratio is 14.03, compared to the sector’s P/E of 12.45.

Should You Invest in Power Grid Stocks?

Over the last year, PowerGrid has outperformed its benchmark index. Power Grid Corporation of India Ltd. share price moved up by 0.20% from its previous close of Rs 279.55. Power Grid Corporation of India Ltd. stock last traded price is 280.10. Daily Power Grid’s MACD crossover appeared yesterday and its average price gain of 3.34% within 10 days of this signal in the last 10 years gives a buy signal to the investors.

However, you should always consider a company’s financial health, leadership, and industry position to decide. With the company’s history and performance, you can make an informed decision.

Conclusion

Investors looking for exposure to India’s developing energy infrastructure may want to consider investing in Power Grid Corp. Power Grid has a solid financial performance, excellent growth potential, and a favorable market position, making it an interesting investment opportunity. Investors should undertake due research before making any investment selections, analyze their risk tolerance, and engage with investment professionals.

Visit the Dhan website to start your investing journey now and stay up to speed on the stock market.

Corporate governance might sound like a term reserved for boardrooms and executives, but its importance permeates every aspect of a company’s operations. Whether it’s a small startup or a multinational corporation, having effective corporate governance practices is crucial for success and sustainability. But navigating the complexities of corporate governance isn’t always a walk in the park. Here is a look at the challenges companies encounter in maintaining these practices, particularly in the context of multinational corporations, and how the Legal Entity Identifier (LEI) can be a game-changer in streamlining corporate governance processes.

What is Corporate Governance?

At its core, corporate governance is a set of rules, practices, and processes that direct and control a company’s operations. It entails balancing the interests of multiple stakeholders, including shareholders, management, customers, suppliers, financiers, the government, and the community.

The Challenges of Multinational Corporate Governance

Transparency and Accountability Across Borders

Operating across different countries means contending with diverse legal systems, cultural norms, and regulatory frameworks. This complexity can lead to inconsistencies in governance practices, making it difficult to ensure alignment with the company’s overall objectives and values. Lack of transparency undermines trust among stakeholders and exposes the company to legal and reputational risks.

Coordination of Governance Structures

Multinational corporations often have subsidiary companies in various countries, each with its own board of directors and management team. Coordinating these entities to ensure consistency in decision-making and strategic direction requires careful planning and communication.

Cultural Differences

Cultural differences can cause significant challenges to effective corporate governance. Bridging these divides and fostering a cohesive corporate culture that upholds ethical standards and integrity can be an ongoing struggle.

Regulatory Compliance

Navigating different regulatory environments in each country can be a daunting task. Multinational corporations must stay abreast of regulatory changes and ensure compliance with laws and regulations spanning multiple jurisdictions. Failure to do so can result in penalties, legal disputes, and damage to the company’s reputation.

Language and Communication Barriers

Operating in multiple countries means dealing with language barriers and communication challenges. Misinterpretation or misunderstanding of governance policies and procedures due to language differences can lead to conflicts and inefficiencies within the organisation.

Currency and Financial Reporting Challenges

Fluctuating exchange rates and varying accounting standards across countries can complicate financial reporting for multinational corporations. Ensuring accuracy and consistency in financial statements becomes a challenging task, requiring robust systems and processes to address these complexities.

The Role of Legal Entity Identifiers (LEIs)

Amid these challenges, the Legal Entity Identifier (LEI) emerged as a beacon of hope. LEIs are unique identifiers assigned to entities engaging in financial transactions. They provide a standardised method for identifying legal entities, helping to streamline regulatory reporting and improve transparency in financial markets.

How LEIs Address Corporate Governance Challenges

Enhanced Entity Identification and Verification

LEIs simplify the process of identifying subsidiaries, affiliates, and counterparties across different jurisdictions, reducing administrative burden and minimising the risk of errors.

Facilitate Regulatory Compliance

LEIs provide a common language for reporting entities, simplifying regulatory compliance and ensuring consistency in reporting standards.

Improved Risk Management and Transparency

By linking entities to their ultimate parent companies, LEIs help stakeholders gain a clearer picture of a company’s ownership structure and risk exposure, thereby enhancing transparency and building trust.

Navigating the complexities of corporate governance, especially in the context of multinational corporations, is a challenging feat. From grappling with diverse regulatory environments to bridging cultural differences, companies face many challenges in upholding effective governance practices. However, with the right tools and approach, companies can mitigate many of these challenges and pave the way for more transparent, accountable, and resilient governance processes. As the business sphere continues to evolve, leveraging technology and standardised practices will be vital to navigating the ever-changing terrain of corporate governance.