Roof systems in Long Beach face steady exposure to coastal conditions that gradually wear down protective materials. Damage rarely begins as a visible leak. Instead, early deterioration appears through small surface changes such as loose shingle edges, granule buildup in gutters, or minor gaps around flashing that allow moisture to move beneath the outer layer.

Preventive maintenance focuses on identifying those early indicators and correcting them with limited labor and materials. Clearing debris, resealing exposed joints, and securing loose fasteners stabilize vulnerable areas of the roof surface. Regular observation from the ground and periodic professional inspections help maintain predictable repair costs and reduce the likelihood of interior moisture damage over time locally.

Early Warning Signs

Cracked or curled shingles, popped nail heads, and missing granules in the gutters are early clues that the roof surface is wearing out. Brown ceiling spots or peeling paint near vents can point to slow moisture entry that hasn’t turned into a steady leak yet. Even a slight dip along a roofline can signal trapped water or soft decking that needs attention before it spreads.

Attic checks can confirm what the exterior cannot show, since damp insulation, faint water trails on rafters, or a musty smell often appear before visible leaks. Catching these signs early usually limits the work to sealing, patching, or replacing a few shingles instead of opening larger sections. Keeping a quick photo record after storms helps track changes. If deterioration moves beyond small maintenance fixes, scheduling professional roof repair in Long Beach becomes a practical next step before structural damage develops.

Seasonal Coastal Stress

Salt in Long Beach ocean air settles on metal flashing, vent boots, and exposed fasteners, and it can speed up corrosion even when the roof looks fine from the street. Harbor winds add another strain by nudging shingles upward along eaves and ridgelines, which weakens the seal over time. After a few breezy days, it helps to look for lifted corners, wavy shingle lines, or new gaps around pipe penetrations.

Seasonal changes tend to reveal these weak points because cooler mornings and warmer afternoons make materials expand and contract, loosening already stressed areas. A roofer can confirm trouble spots with close-up checks around chimneys, valleys, and drip edges, where wind-driven mist likes to travel. Scheduling that inspection before the first fall rain keeps repairs small and makes storm prep feel straightforward.

Low Cost Maintenance

Routine roof upkeep in Long Beach usually centers on small tasks that control moisture movement. Valleys often collect leaves, sand, and roofing granules that slow drainage during rain. Removing that buildup allows water to exit quickly instead of pushing sideways beneath shingle edges or under flashing seams during heavier coastal storms and winter fronts nearby.

A second focus involves exposed sealants and metal fasteners. Sealant around vents, chimneys, and wall transitions can dry, crack, and separate after years of sun exposure. Replacing brittle sealant and tightening loose fasteners restores water resistance and helps extend the working life of the surrounding roofing materials across multiple seasonal weather cycles in coastal neighborhoods.

Drainage System Care

Gutters packed with leaves, roofing grit, and windblown sand can slow runoff and make water creep back under the first row of shingles. When downspouts clog or discharge too close to the house, overflow often shows up as dark staining on fascia boards or damp spots near eaves. After a storm, look for water marks, sagging sections, or soil washed out below the outlet.

Good drainage protects more than the gutter line because steady overflow can rot roof decking at the edge and invite termites into soft wood. Splashback can wear down paint and raise moisture levels around attic vents, which adds to ventilation problems. A simple hose test can verify flow from each downspout and confirm that runoff is being carried well away from the foundation.

Property Value Protection

Inspection notes often mention roof condition because it affects safety, moisture risk, and future repair needs, and that matters in Long Beach sales. Buyers and appraisers look at the age of the roof, visible wear at edges, and any signs of past leaks in ceilings or attic spaces. Clear records of maintenance visits and small repairs can make those conversations easier and keep the focus on the home’s strengths.

Real estate deals can slow down when a roof is flagged, since lenders and insurers may ask for repairs or proof the roof still has service life left. A roof that’s been kept in good shape signals responsible homeownership and reduces the chance of last-minute credits or renegotiations. Keeping invoices, photos, and a simple maintenance log ready helps support a clean inspection report when timing matters.

Consistent maintenance plays a direct role in extending roof service life in Long Beach conditions. Salt exposure, wind movement, and seasonal rain steadily impact shingles, flashing, and fasteners, making early correction of minor issues important. Clearing drainage paths, maintaining sealant integrity, and monitoring exposed metal components reduce moisture intrusion risk. Regular observation supported by basic records such as photos and service notes allows accurate tracking of roof condition. This approach supports timely repairs, stabilizes long-term performance, and reduces the likelihood of higher costs associated with advanced deterioration.

In 2026, finding the right car insurance has become easier than ever, thanks to numerous insurers offering quick and convenient online access. Many digital platforms now provide real-time comparison of policies to ease this process. While the selection, purchase and renewal of car insurance have become easier, choosing the right coverage still requires thoughtful evaluation.

Here’s a quick guide that looks at the crucial components you need to keep in mind to choose the right car insurance online that meets your needs and is within your budget.

Understanding the Types of Car Insurance

There are mainly three types of motor insurance, which are as follows:

- Third-Party Car Insurance

As per the Indian Motor Vehicles Act 1988 (as maybe amended from time to time), every vehicle on Indian roads must have third-party car insurance. This insurance policy only provides financial protection to third-party damage caused by your vehicle.

- Own Damage Car Insurance

An own-damage car insurance plan is used as additional protection for vehicles among car owners. It protects your car from natural calamities, accidents and thefts. However, you should have a separate third-party insurance plan.

- Comprehensive Car Insurance

A comprehensive plan combines both third-party and own damage cover in a single policy. It provides vehicle owners protection against accidents, thefts, and natural calamities like floods, in addition to third-party coverage. This policy also allows you to get the benefit of No Claim Bonus (NCB) and options to add multiple add-ons.

Assess Your Personal Insurance Needs

Every driver has unique insurance requirements. Understanding your specific requirements can help you choose the most appropriate protection within your budget.

Some of the main factors to consider are as follows:

- Vehicle age and current market value

- Driving record

- Additions of add-ons

- Residential location (urban, suburban, or rural)

- Financial comfort with higher or lower deductibles

Factors Connected with Car Insurance

There are multiple factors that represent the actual value of your car insurance. It helps you compare quotes and understand acronyms mentioned on policy papers. Some of them are as follows:

- Insured Declared Value (IDV): The IDV is the current market value of your vehicle after adjusting for depreciation.

- Add-ons*: These bring additional coverage over your standard own-damage or comprehensive coverage. Some popular add-ons include engine protection cover, zero depreciation cover, and roadside assistance cover.

- Voluntary Deductibles: At the time of claims, you may need to pay some amount upfront, which is called the deductible. Note that lower deductibles may reduce your claim amount, but they may increase your premium.

- Cashless vs. Reimbursement Claims: With cashless claims, the insurer directly pays the amount to the garage for repairs to your car. On the other hand, in reimbursement claims, you first pay the repair cost to the garage, and later, the insurer reimburses the amount to you. In both cases, the insurer pays the remaining repair costs of your vehicle after the deductibles are taken care of.

- Policy Wording: The policy wording mentions complete details about the inclusions and exclusions of the motor insurance policy. While purchasing car insurance, carefully read this document to get clarity on what your coverage entails.

Check the Insurer’s Customer Support

Look for how reliable the customer service is across insurers. In 2026, many insurers have the following customer service options:

- Verified customer feedback

- Claims processing efficiency

- Availability of 24/7 support

- Mobile claim filing options

Compare Quotes the Smart Way in 2026

In order to compare insurance policies, there are multiple steps to be followed. Let’s have a look at them one by one:

- Vehicle Details: Collect the accurate details of your vehicle. This includes your vehicle’s make and model, along with its physical condition.

- Browse Insurers: Compare 3-4 insurers by checking their offerings, availability of add-ons, and accessibility to cashless garage access, amongst other things.

- Revision of Voluntary Deductibles: When you are creating the quote, put a deductible amount you will be comfortable paying during a claim. This helps ensure that you get the right value from your car policy without it over-stretching your budget.

Final Thoughts

The selection of the right car insurance online requires the evaluation of multiple factors. Some of them include your IDV, deductibles, availability of add-ons, network of garages, and type of claims (cashless or reimbursement). Check all of these elements from multiple insurers online and get a quote from each of them. While checking the pricing, also look for customer feedback, availability of round-the-clock customer support, and ease of claims filing. By being clear on these factors, you can choose the right car insurer digitally and enjoy overall financial protection for your car.

*Add-ons are subject to payment of an additional premium.

The above information is for educational purposes only. For more details on the risk factor, terms and conditions, please refer to the Sales Brochure and Policy Wordings carefully before concluding a sale. Policy terms and conditions apply.

Thinking about changing careers can feel like standing at the edge of something big. It’s exciting, but it can be nerve wracking, especially if you’re looking to make a full change and start again in another industry. There are plenty of questions that start with what if, but the truth is that many people reach a point where they wonder if there’s something better suited to their skills, interests or lifestyle. Let’s also remember that the career that you may have chosen in your 20s may not suit you by the time you get to your late 30s and early 40s because you may have outgrown it, and that’s OK.

It’s important to start with what’s pulling you. Sometimes the desire to switch pathways comes from curiosity. Maybe you’ve come across roles like CDL hazmat jobs and thought of something different. These moments are worth paying attention to. They can reveal what kind of work stimulates you and what type of environment, pace, or challenge you’re actually drawn to. Even if you’re ready to make the jump, not quite yet. You then have to check in with your current situation before you make any big moves.

It helps to reflect on where you are now. Are you feeling stuck, bored, or ready for growth? Or is it just a temporary phase? Understanding your reasons can help you to determine whether a full career change is the answer or if small adjustments could make your current role more satisfying. It’s OK not to have everything figured out just yet, because one of the biggest myths about career changes is that you need a perfect plan. But there’s no perfection here. In reality, most people just figure things out as they go. You might try something new, learn new skills, and adjust along the way. It’s less about getting it right immediately and more about moving in a direction that feels better for you.

You need to think about your lifestyle as well, not just the job title. A new career isn’t just about a different work life, it’s about a different way of living entirely. You have to consider your schedule, your income expectations, your work environment, and how much flexibility you want. Do you have children? They might be a factor in your decision making too. Sometimes the biggest benefit of a career change isn’t the job itself, but how it fits into your current life. There may be a learning curve in the new job, and that often comes with a salary drop. Switching careers often means starting fresh in some ways. You may need new certifications, training, or time to build your confidence, and it can feel uncomfortable in the beginning, but it’s also where your growth is going to happen. Being a beginner again isn’t a step backwards, but a part of moving forward in general.

If you can talk to people who have already done it, Hearing real experiences can make a huge difference, especially if you talk to people in the industry you’re looking to move into. What’s going to matter the most is whether the change aligns with what you want your life to look like. And if it does, then it might just be worth taking that first step.

Living in a metro city changes the way you experience healthcare. Hospitals are more specialised, treatment choices are wider, and billing is often structured around packages and premium facilities. If you are looking for the best health insurance plan in India, zone-based rules and zone upgrades are worth understanding because they can influence your final claim payout.

In this article, you will explore how zones work, when upgrades matter, and how to tailor senior cover for metro hospital costs today.

Why Metropolitan Senior Living Changes the Cover You Need?

Metro healthcare is convenient, but it can be expensive in small, surprising ways. A routine admission can involve multiple specialists, frequent diagnostics, and hospital billing that quickly climbs.

- Specialist consultations pile up faster than you expect.

- Tests and scans are frequent, even for mild symptoms.

- Hospital packages include extras that quietly raise your bill.

- One admission can trigger follow-ups, medicines, and rehab.

What Zones Mean in Health Insurance

In many policies, “zones” are used to group cities by typical healthcare costs. Metro cities are often in higher-cost zones, while smaller cities are in lower-cost zones.

Where Zone Limits can Affect Claims

Zone restrictions are usually not obvious at the buying stage. They tend to show up when you claim, especially if your policy was priced for a lower-cost zone, but treatment is provided at a metro hospital.

You may notice this through:

- Higher out-of-pocket spending even after approval

- Deductions linked to room eligibility and related hospital charges

- Reduced reimbursement for certain expenses when the policy applies zone-linked limits

How a Zone Upgrade Helps Senior Citizens in Metro Cities

A zone upgrade is designed to align your coverage with a higher-cost zone, typically the one that includes metro cities. In simple terms, it aims to make your policy more metro-ready, so your claim settlement is less likely to be affected by city-based cost differences.

When a Zone Upgrade is Worth Considering

A zone upgrade is often useful if the senior citizen:

- Lives in a metro city for most of the year

- Prefers treatment at large hospital chains or specialist centres

- Travels frequently between cities for family support

- Wants flexibility to choose hospitals without worrying about zone-related deductions

How to Customise a Senior Plan Beyond Zone Upgrades

Zone upgrades work best when the rest of the policy structure supports senior needs. Once zone fit is sorted, look at features that protect day-to-day affordability and reduce common deduction triggers.

Consider these customisation angles:

- Room eligibility flexibility, because room category choices can affect associated hospital charges

- Coverage for consumables is offered, since items used during hospitalisation can add up

- Post-hospital support benefits were available, especially if home recovery care is part of the plan design

- A clear approach to co-payment terms, because many senior policies include shared cost clauses that should be understood up front

How to Choose the Best Health Insurance Policy for Senior Citizens in India

When people look for the best health insurance policy for senior citizens, the comparison should go beyond the premium and sum insured. The strongest plans for metro living are usually the ones with clearer rules that reduce ambiguity during claims.

While evaluating options, focus on:

- How zones are defined and how your city is classified

- What changes when you opt for a zone upgrade

- Whether the room eligibility rules are strict or flexible

- Whether common senior claim triggers have limits you can live with

- How dependable does the cashless network feel for the hospitals you would realistically visit

Common Mistakes to Avoid

Small oversights can undo the value of an otherwise good policy. This is especially true for metro claims, where billing structures are less forgiving.

Avoid these common mistakes:

- Buying a plan based on a non-metro premium without checking the zone applicability

- Ignoring room eligibility rules and assuming any room category will be covered similarly

- Treating add-ons as marketing rather than matching them to likely expenses

- Skipping the policy wording, especially the parts that explain deductions and limits

Final Thoughts

Zone upgrades are not a niche feature for senior citizens in metro cities. They can be a core customisation that aligns your policy with real hospital pricing and reduces claim-stage deductions. If you want cover that feels reliable when it matters, start by getting the zone fit right, then customise the policy around the senior’s treatment habits and hospital preferences.

Selling your home can feel overwhelming, especially if it’s the first time you’ve ever done it. There are so many steps involved from preparing the properties and negotiating with the buyers. Understanding a few important basics makes the process so much smoother and less stressful. If your goal is settling the house quickly, the right preparation and decisions can make a big difference to you. So let’s take a look at 4 important things that you need to know when you’re selling your house.

First impressions really do matter.

The first impression that your home receives from potential buyers can influence their decision strongly from the moment they walk in. Many buyers form an opinion within minutes of seeing a property, and that’s why it’s important to make your home look clean, welcoming and well maintained. You can clean every room, remove any clutter and consider a fresh coat of paint if the walls look worn. Mow the lawn, trim the plants, and make sure that the exterior looks as good as the interior. Small details like good lighting and tidy spaces can also have a big impact on your sale.

Price your home correctly.

One of the important decisions that you’re going to make when selling your house is setting the right price for it. If you price the house too high, it may stay on the market longer than you expect. Buyers may even avoid viewing it because it seems outside their budget. On the other hand, pricing it too low could mean losing potential value. Research similar homes that have recently sold in your area to get a realistic idea of the market. Many sellers also work with real estate agents who can provide a professional valuation. A competitive, fair price can attract more buyers and create strong interest in your property.

Marketing really does make a difference.

Good marketing helps your home to reach more potential buyers. Today, many people start their home search online, which means high quality photos and clear descriptions are very important. Making sure that your listing highlights the best features of your house, including a renovated kitchen or a large backyard, is important. The more visibility your home has, the more likely it is that the right buyer will find it.

Be prepared for negotiations.

Once buyers start showing interest, negotiations often follow quickly. A buyer may offer a lower price, request any repairs, or ask for a certain condition before completing the purchase. Being prepared for these discussions helps you to make better decisions. It’s helpful to know your priorities in advance. For example, you may be willing to negotiate on price but not on the timeline, or vice versa. Working with a real estate professional can also help during this stage because they’ll guide you through the offers, counter offers, and contracts.

This doesn’t have to be a complicated process, so just pay attention to it carefully and you can attract the right buyer and move on to the next chapter with confidence.

Tracking equipment condition sounds straightforward when you have a small portfolio. But once lease volume grows, condition records often end up scattered across spreadsheets, inspection forms, maintenance logs, emails, and contract files. That makes it hard to answer simple but important questions: What condition was the asset in at delivery? What happened during the lease term? What damage, servicing, or wear should be recorded at return? This is exactly why equipment lessors look for a system that combines asset tracking with lease operations in one place. SOFT4Leasing describes equipment leasing software as a platform for managing the full lease lifecycle—contracts, asset tracking, payments, compliance, and reporting—in one system.

The first requirement is a single asset record that stays connected to the lease from beginning to end. If condition details live outside the lease record, teams lose context fast. Operations may know the maintenance history, but finance may not see the cost impact, and account managers may not know whether the asset’s condition affects renewal, replacement, or return charges. A centralized leasing platform solves that by linking the equipment asset to the contract, usage history, and related service activity. SOFT4Leasing specifically emphasizes asset tracking and full lifecycle management as core capabilities for equipment and fleet leasing operations.

Condition tracking during the lease period is not just about logging breakdowns. It also includes maintenance events, usage history, inspections, repairs, and other changes that influence asset value and customer service. If that information is not captured continuously, lessors are forced to reconstruct the story later—usually when the asset comes back in worse shape than expected. SOFT4Leasing’s fleet and leasing materials highlight tracking asset history, mileage or usage, maintenance and repairs, residual values, and profitability, which reflects the kind of structured recordkeeping needed to monitor condition over time.

Maintenance and service events are especially important because they show not only the current condition of the asset but also how it has been managed during the lease. A piece of equipment that has been regularly serviced and properly documented is far easier to evaluate at return than one with incomplete records. SOFT4Leasing’s platform is presented as supporting full-service lease management, including contracts, maintenance, and billing, which makes it relevant for lessors that need condition tracking tied directly to operational and financial workflows.

Return management is where condition tracking becomes financially critical. At end of term, lessors need to compare the returned asset against expected condition, assess wear and damage, and determine whether repairs, charges, refurbishments, or resale actions are needed. This process becomes inconsistent when delivery condition, service history, and return inspections are stored in separate tools. SOFT4Leasing highlights managing acquisitions, deliveries, maintenance and repairs, and end-of-term resale or disposal from one workspace, which is exactly the kind of setup that supports consistent return evaluation.

A system like SOFT4Leasing helps because it connects contracts, asset records, maintenance activity, and reporting in one place. Its broader feature set includes lease automation, fleet management, full-service leasing, and asset history tracking, which together give lessors a more complete view of each leased item throughout its lifecycle. That means teams can review the original lease, check how the equipment was used and serviced, and assess return condition without piecing information together manually.

The operational benefit is clarity. Service teams can update asset history as events happen. Lease managers can see how those events affect active agreements. Finance can connect repairs and condition issues to asset profitability and end-of-term outcomes. Management gets stronger reporting on asset health, residual value exposure, and portfolio performance. SOFT4Leasing consistently frames its product as an all-in-one leasing platform designed to centralize leasing data and improve control, which is exactly what condition tracking requires as portfolios scale.

In the end, tracking equipment condition throughout the lease period and at return is not just about documenting wear and tear. It is about creating a continuous, connected asset history that supports better servicing, cleaner returns, more accurate charges, and smarter resale decisions. For lessors looking to manage that process in one system, SOFT4Leasing is a strong fit because it combines lease lifecycle management with asset tracking, maintenance visibility, and end-of-term control.

Are you worried about the cost of living crisis? You’re far from alone here. A lot of people are struggling to keep costs in control due to rising levels of inflation as well as problems relating to the growing conflicts around the world. So, let’s take a look at some of the key steps that you can take to get your finances back on track when you are struggling.

Sell Assets

You might have items and assets that you can sell off to make a large chunk of money. This can be used to pay off any debts or bills that are bringing you down. It might be that you have an old car that you aren’t using anymore. A scrap car buyer will certainly be interested in buying your car off you. Even if you don’t make much, it is better than nothing. Think of other assets you have laying around, collectors items for instance. Get these seen to by an expert in the field, or even list them on online marketplaces.

Use An Accounting App

If you are struggling with your monthly bills then you might benefit from using an accounting app. This will input all your data and information into one place, it will then give you suggestions on how you can save money. It could make suggestions like switching your energy providers or moving to another tariff. Do your research here as there are some great free ones so you aren’t adding to your existing problems.

Speak To Your Creditors

Another way you can manage growing costs is to speak to your creditors, this is becoming increasingly popular thanks to the cost of living crisis. If you owe money to creditors each month and this is getting out of control then you can ask to cut back on these payments. If for example, you have a credit card and you can’t keep up with the payments then you can speak to creditors about a token payment. This is much less than the amount you will currently be paying, but a small payment is better than no payment at all.

Go Green

Finally, think about ways you can go more green. Believe it or not, going green is a great way of saving money and managing growing costs. Lowering your overall energy consumption is a natural way of going green and you will thank yourself when your monthly bills come through. Installing LED lights bulbs is great, not only for your home and the environment, but also your wallet. Shop around as these can vary massively from seller to seller. Something that can also slowly add up over time is your bills from leaving appliances on stand by. It is important to fully turn these off when not in use, your television is a great example of this.

So there you have it, several ways you can manage your costs more effectively. Making small changes now can make a world of difference to your bills and high costs.

It takes a lot of time and effort — not to mention money — to get your hands on a commercial property. With that said, you can argue that it’s only once you’re installed that the real work begins. All types of property investment can benefit from having a proactive owner, but it’s especially relevant to commercial property, in which the adage you get out what you put in very much applies.

Getting started on the right footing sets your commercial property venture up for success. In this post, we’re going to outline some of the key steps to take within the first twelve months of holding the asset.

Finalize Comprehensive Insurance

Your commercial property insurance is the safety net against catastrophe. No one ever expects things to go wrong, but when they do, they have the capacity to put a serious dent in your investment.

Many new owners carry over the policy from the previous owner, but that will have been appropriate for their needs, not yours. Reviewing existing policies and making adjustments is key to making sure that you’re fully protected. It’s recommended to work with an insurance expert who specialises in commercial property insurance, rather than a general insurance agent.

Establish Your Property Management Systems

Having a strong property management system in place early on can help to prevent problems down the line. The longer you take to establish these systems, the more likely it is that you’ll spend more time than you’d like solving problems, rather than managing your assets correctly.

New commercial property owners often make the mistake of waiting for things to go wrong before they begin thinking about how things should be done. In most cases, you’ll find that hiring a property manager is the right way to go, though it’s also possible to manage it yourself with the right resources. Whatever you decide, do so early.

Conduct a Thorough Inspection

You’ll have completed an inspection of the property when carrying out your due diligence before purchase. However, while those inspections are excellent at identifying large problems, they’re not as thorough as many people expect. Minor issues often get left out due to time constraints.

That’s why most professionals recommend carrying out a more thorough inspection once you’re in ownership of the property. Doing so will allow you to make a comprehensive list of the aspects of the building that are in good shape, which are not, and which may pose problems down the line.

Ultimately, it’s a lot easier to handle an issue when it’s minor and can be repaired/replaced without disruption, rather than waiting until it experiences catastrophic failure and must be replaced immediately.

Work With Tax Professionals

Anything that helps to improve cash flow is recommended, and for that, there’s arguably no better strategy than maximizing your tax deductions. All too often, new commercial property owners take the same approach to their property tax as they do to their personal tax, not realizing that there are many strategies that can help to lower their tax burden, which in turn improves cash flow. One effective strategy is to accelerate tax deductions with cost segregation to year one instead of spreading deductions over 39 years. While you can use this strategy at any point, you’ll get the most benefit if you do so within the first twelve months.

Establish Your Maintenance Schedule

It’s easy to overlook the importance of developing and sticking to a maintenance schedule, but it can have profoundly positive long-term benefits, since it helps to avoid large-scale problems that have the potential to destroy investment value.

After all, it’s a lot cheaper to spend $500 to fix a minor problem, rather than spending $10,000 to replace the whole system two years down the line. Maintenance work isn’t glamorous, but it’s the backbone of making sure that your investment stays in tip-top condition.

It’s recommended to start building your capital expenditure reserves as soon as you have your hands on the keys. By putting away 10% of gross rents, you’ll avoid the problem that many commercial property owners experience, which is struggling to find the cash for repairs.

Start Building Your Relationships

Great commercial property management runs on relationships — with the tenants, with repair people, and with the professionals in the background who keep your business running smoothly. Focusing on nurturing these relationships, rather than seeing them as simply transactional, really can make a big difference to how well your first twelve months (and beyond) go. Ultimately, if the relationships are solid, then everyone benefits.

Its been developing for over a decade. The rise of social media was the first major shift in this direction towards Big Tech functioning like a colonial empire of centuries past. Recent quotes from AI executives like Sam Altman simply expose that the transformation is complete. Big Tech looks at the people of the world the same way the British Empire used to see the people across its worldwide empire. We exist for extraction and are expendable. It is a bleak way to look at things, but I also think its critical to see things in this way as we try to determine the best way to protect our money and happiness in the modern world.

Different Tactics, but Same Attitude

The empires of centuries past were obviously overtly oppressive and weren’t apologetic about extracting resources from their colonies at the expense of the people there. They came in with weapons and subdued the people. These were empires of harsh force, but the end goal was to extract wealth from far off lands where the people could be viewed differently from the homeland.

If the modern world of Big Tech, its obviously not going to be physical oppression that is the tactic used. That is not how the world works now, but also its not the best tactic for extraction of wealth. Its much more lucrative to mine for attention and data. In the digital world, its much easier to colonize consumers than it is to go conquer land for resources.

This attitude of Big Tech has been laid bare recently due to the rise of AI. Now the path for money for many of these companies is to replace the jobs that many people hold. The cold statements that continue to flow from AI company CEOs show a very clear colonial view of the people they would be displacing. They don’t care about the job losses. They are simply talking to their investors in the same way a British merchant would talk about profiting from a far off colony in the 1800s.

The part that comes off so bizarre is that these CEOs are talking about fellow citizens of the same country they inhabit, but that is where the truth comes out. These CEOs inhabit the Silicon Valley and its clearer than ever that they don’t view themselves as part of the greater nation or world at all.

Social Media and the Cultural Takeover

Another major aspect of old colonial rule was imposing the colonial culture on the world. This is still seen in our modern day as aspects of British culture are very prevalent all over the globe. The impact of social media wasn’t necessarily an intentional cultural export, but it has still had the same effect. People are increasingly unhappy at the isolated and polarized world, but at the end of the day that culture serves Big Tech. Isolated, angry people are great for engagement and for impulse purchasing.

I often wonder how much of the current culture is an unintentional consequence of the growth of the digital age or if these companies have worked to steer it in this direction. One thing we definitely do know is that as the culture of tech took over, the companies did not work to stop it and only paid lip service to its challenges. The damage of social media to young people is well documented and the prevalence of scams on Facebook is known to be a large portion of the revenue.

In both of these instances, Big Tech stays in line with what serves the extraction economy and hasn’t really stepped up to shift in any meaningful ways. Due to the financial incentives, no one should expect this trend to change and most likely there will be continued advances in this cultural takeover. It doesn’t help tech companies profit if people leave their phones at home for a long hike or spend an evening playing board games with friends. These things go against the culture that serves the empire. Isolation and anger feed the empire and so we shouldn’t be surprised to see it get worse.

The Never Ending Extraction Economy

Watching sports over the past few months in the runup to the Super Bowl, the Big Tech extraction economy was coming at all of us aggressively. It was constant ads for Doordash, Uber Eats and gambling. At the end of the day, all of these things are designed simply to move money out of communities across the country and into the arms of Big Tech. The key element of this economy is constantly throwing things out that are okay in small doses, but easily get out of control.

Getting Doordash when you are sick or injured is one thing, but it has become another element of the Big Tech cultural takeover. Its increasingly common for people to order food delivery and I know for many families its a sizable monthly bill that they would probably like to see going into investments. Restaurants get squeezed by these services and its also been written about that the money for drives isn’t great either. Doordash and Uber Eats started at a much lower price point with huge subsidies from investors, but now that they have expanded they are continuing to squeeze more money out of the system.

Gambling sites and now prediction markets like Kalshi depend on the fact that a certain percentage of the population will not be able to control their betting which will lead to massive profits. These type of sites are the most clear example of how the Big Tech Empire operates. They offer something that is a trap for a fair amount of people, but its not actually forcing anything so its deemed okay.

As articles flow out each week about the massive challenges facing young people today, I keep thinking about Doordash and Draft Kings and wonder how many people, particularly 20 something men would be in a much better place without having hundreds of dollars siphoned off each month.

The increasing flow of doomer stories about how AI is going to take all the jobs only feeds these extraction methods because its hard to save for a future that looks impossible. Its just life in the Big Tech colonies: steady feed of doomscrolling stories, plenty of images of people looking happier than you and constant ads popping up to give you easy places to blow your money.

Resistance isn’t Futile

As a father of two teenage kids, I think a lot about how the world is moving and what it will look like for then to lead a fulfilling life in a world that is increasingly being bent to the will of Big Tech. However, there is actually more hope than this post has shared up to this point. The biggest point of hope is that Big Tech doesn’t directly oppress the way empires of the past did. Big Tech is simply betting on the fact that enough people will get caught up in its apps to feed its profits. They don’t care about the people avoiding them because there will likely always be enough getting caught.

My wife and I started with limiting our kids screen time and exposure to social media, but I soon realized that i needed something similar for myself. I ended up putting limits on my time on Youtube and X, just to limit how much it was impacting my brain. We have fought to schedule time with friends and always have a book we are reading.

I have a personal crusade against our family using food delivery apps. If the delivery apps are out of the picture, it forces us to do things that are frankly more life giving. Cooking at home is way more healthy and going out to a restaurant is way better for getting into conversation, but both take a lot of effort.

In terms of the final battle against AI, I keep a conversation going with our kids about all the jobs that are going to be around in the future. So many jobs that center on dealing with people or building things in the real world will continue to exist and will frankly thrive in a world with AI. The biggest thing I’m hoping to give them is a picture of a world that will still be a great place to live and that they can build a life in.

There has been quite a bit of commotion about the fact that the average age of a first time home buyer in the US has risen to 40 based on the latest data available. This average age has been moving up for years as homes become more expensive, but also due to families forming later in life. When this number gets discussed it is mostly from the negative perspective, but it is worth stepping back and looking at this from a fresh perspective. The world is undergoing a major shift as people migrate towards the economic engine cities which come with sky high housing costs. There is also a significant shift towards getting married and starting families later in life.

In this new climate, it is worth simply evaluating if 40 is actually the right age to purchase a first property? Is this the right balance between benefiting from the lower cost to rent in many cities, but ending up in a home that you can eventually pay off.

Life Takes Longer To Launch in the Modern World

Aside from those who work in tech or finance, the process of working up to a solid salary takes some time. Its a balance of getting experience and finding where you can add the most value in whatever profession you choose. Most people have false starts in one way or another. For most of my friends, their 20s was largely a feeling out period of trying out the different aspects of their chosen field or realizing that they needed to shift to something new. This sorting period isn’t expected and is frankly incredibly disappointing to many, but its common.

This aspect of career development seems to be causing Gen Z tons of grief because it doesn’t present a linear path to making the kind of money that fits with owning a home. College is far from an automatic step and it adds on student loans to the equation. When you are fresh out of college and only making $50K a year, it looks impossible, but it just needs space to breathe. For most, 30 is just too young to think about saving enough for a down payment, and that is okay.

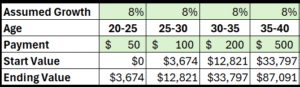

Here are a couple scenarios that show how a person can gradually increase their savings as they grow their income. The first assumes a steady increase between 20-40. It doesn’t look great at 30, but between 35 and 40 the combo of increased savings and compounding really kick in. This is actually pretty conservative returns at 8% a year and it still gets to $87K to put towards a home (or just keep rolling in an index fund).

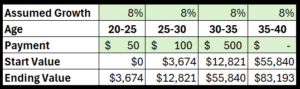

This next scenario represents a couple who knows they want to have kids and so puts more down in their early 30s, but doesn’t save at all for 5 years when the kids are little. This still puts them in a spot to buy a house as the first kid starts school.

No money goes in from 35-40, but it still gets up to $83K. That is more than enough for a solid down payment in many parts of the country. It also shows that you can get to some decent savings without huge monthly savings rates. These numbers would be very approachable for two incomes renting a reasonable place.

Why Buy a House at all?

If you are in your late 30s and you’ve actually started getting a nice nest egg invested in the stock market it would make sense to just keep riding with that plan. If you want to stay in a big city where homes are extremely expensive then this could be a good idea. The reason to buy a home starts with entering a season of life where you want to be stable for a while.

Real estate has historically been a good investment when held for a long time. If you think you will be moving around and jumping to new jobs, then it doesn’t actually make much sense. If you have school age kids or will in the coming years, then having a stable location becomes much more appealing.

This first aspect of buying a home connects with the needs of the moment, but the most important reason to buy a home relates more to the eventual goal of retirement. If you buy a home at 40, then with some additional principal payments each year you can actually set your sites on paying it off. This is a huge deal for thinking about the shift into living off your investments. If you are still renting at 60 or 65, it puts all of your well being at the hands of your investment portfolio. If you have a paid off house, you have a much lower burden and also a separate source of potential money for the future. Paying off a house is the ultimate hedge on the markets and this shouldn’t be missed even though stocks provide more annual returns.

If you are investing in a 401K and putting some extra on paying off a home, this is in my opinion the best way to get ready for retirement. A paid off house takes much of the risk out of future potential black swan events for the stock market or even the housing market.

Putting Down Roots is Bigger than Just Money

In the previous section I’ve laid out the financial side of why buying one home and paying it off would be valuable from a financial perspective, but there is a more important side to this. The idea of really putting roots down in a community has far more potential benefit than just the financial. If you mentally plant yourself and start paying a home down, then its easier to invest in neighbors and in your local city. This is part of a remedy to the disconnected existence that is so common in modern life. When everyone is passing through its easy to stay aloof, but when you have planted, it can’t help but shift your mentality.

In the culture of the United States, there is a major difference to a neighborhood where most people own their homes and are looking to stay long term. It is incredibly pronounced when you move from a major city where people are highly transient to any smaller metro where people tend to settle down to raise kids.

This is the last major reason that it makes the most sense to target 40 to buy a first home: you need to be ready to settle down. People aren’t settling down to have kids at 28 anymore. Those days are long gone and that is okay. The idea of locking into an area and truly investing in that community is something I hope everyone finds at some point. That is still incredibly connected to buying a home and even though it takes longer these days, it still something worth pursuing.