When you’re navigating the job market or budgeting for your future, knowing what your annual salary translates to in terms of a monthly wage can be incredibly helpful.

In this article, we’ll break down the math and explore what $66,000 a year means on a monthly basis after tax.

We’ll also dive into topics such as post-tax income and whether $66,000 a year can be considered a good salary. Plus, we’ll share tips on how you can potentially increase your hourly wage.

Let’s get into the details now of how much $66,000 a year is a month after taxes.

$66,000 a Year is How Much a Month After Taxes?

Understanding your take-home pay is crucial when planning your finances. The amount you receive after taxes depends on various factors, including your tax filing status, deductions, and the state you reside in.

On average, individuals can expect to pay around 20-30% or more of their income in federal and state income taxes. Let’s take some data from the IRS website on what your tax rate will be according to your income. This does not account for any of the factors listed above.

- 37% for incomes over $578,125 ($693,750 for married couples filing jointly)

- 35% for incomes over $231,250 ($462,500 for married couples filing jointly)

- 32% for incomes over $182,100 ($364,200 for married couples filing jointly)

- 24% for incomes over $95,375 ($190,750 for married couples filing jointly)

- 22% for incomes over $44,725 ($89,450 for married couples filing jointly)

- 12% for incomes over $11,000 ($22,000 for married couples filing jointly)

So at a $66,000 annual income, we will assume a tax rate of 22%.

$66,000 (annual income) x 22% (tax rate) = $14,520

So, after taxes, you would have approximately $51,480 left as your annual income.

To calculate your monthly income after taxes, you can divide $51,480 by 12 (since there are 12 months in a year):

$51,480 (annual income after tax) / 12 (months) = $4,290

So, at a yearly salary of $66,000, your monthly income after taxes would be approximately $4,290.

While this is a decent estimate, your monthly after-tax income can be different depending on a variety of factors.

Factors that Determine Your After-Tax Income

Your monthly after-tax income can vary depending on a multitude of factors, including:

- Tax Filing Status: Your filing status, such as single, married filing jointly, married filing separately, or head of household, can impact your tax liability and ultimately affect your after-tax income.

- Tax Deductions: The deductions you claim, such as the standard deduction or itemized deductions for expenses like mortgage interest, property taxes, and charitable contributions, can reduce your taxable income and lower your tax bill.

- Tax Credits: Tax credits directly reduce the amount of tax you owe, potentially leading to a lower tax liability and higher after-tax income. Common tax credits include the Earned Income Tax Credit (EITC), Child Tax Credit, and education-related credits.

- State and Local Taxes: The amount of state and local taxes you owe can vary based on your state of residence and local tax rates. Some states have no income tax, while others impose state income taxes in addition to federal taxes.

- Additional Withholdings: If you choose to have additional taxes withheld from your paycheck, either voluntarily or to cover other tax liabilities such as self-employment taxes, it can affect your after-tax income.

- Retirement Contributions: Contributions to retirement accounts such as a 401(k) or Traditional IRA can reduce your taxable income, potentially lowering your tax liability and increasing your after-tax income.

- Other Deductions and Adjustments: Various other deductions and adjustments to income, such as student loan interest deduction, tuition and fees deduction, or contributions to Health Savings Accounts (HSAs), can impact your taxable income and ultimately affect your after-tax income.

Overall, your monthly after-tax income is influenced by a complex interplay of factors related to your income, deductions, credits, and tax withholding preferences.

Understanding these factors and their implications can help you better manage your finances and plan for your financial future.

Next, let’s look at if $66,000 a year is a good salary.

Is $66,000 a Year a Good Salary?

Whether $66,000 a year is considered a good salary depends on various factors, including your location, cost of living, and personal financial goals. In some areas with a lower cost of living, $66,000 can provide a comfortable life. However, in more expensive cities, it may not stretch as far.

To determine if it’s sufficient for your needs, consider your monthly expenses, such as housing, utilities, transportation, groceries, and savings goals.

Additionally, factors like job benefits, opportunities for advancement, and job satisfaction play a significant role in evaluating the overall value of your wage.

Let’s take a look at how a $66,000 a year salary compares to others in the United States.

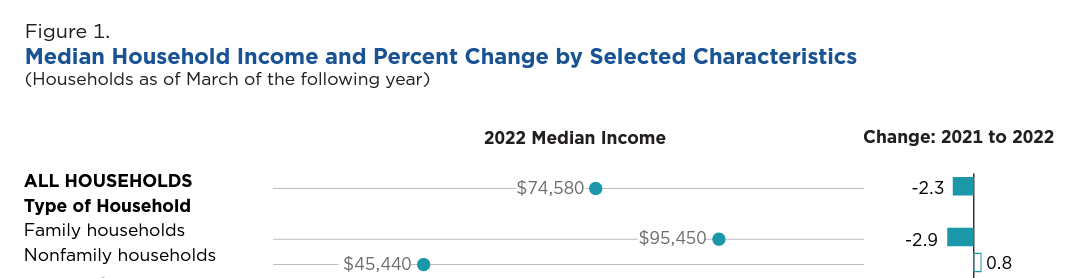

According to data from the US Census Bureau for 2022, the median income for Nonfamily households in the United States was approximately $45,440 – which means that half of all individuals earned more than this amount, and half earned less.

So, if you have a salary of $66,000, you have a salary that is in the top 50 percent of all earners in the United States. With annual pay of over $45,400, you are doing well and are part of a above-average group of earners in the United States.

How to Increase Your Income

When aiming to increase your income and bolster your financial resources, it’s crucial to consider a range of effective strategies:

- Skill Development: Invest in enhancing your existing skills or acquiring new ones that are highly valued in your industry. Keeping pace with evolving trends and technologies can significantly boost your marketability and earning potential.

- Negotiation: Don’t shy away from negotiating your wage when starting a new job or during performance evaluations. Demonstrating your value to employers and advocating for fair compensation can lead to substantial salary increases over time.

- Further Education: Explore opportunities for additional education or certifications that can augment your qualifications and increase your worth in the job market. Continuing education demonstrates your commitment to professional growth and can open doors to higher-paying roles.

- Job Switch: Consider transitioning to a different job or company if it presents opportunities for a significant salary bump. Assess the market demand for your skills and explore job openings that offer competitive compensation packages and room for advancement.

- Freelancing or Part-Time Work: Explore part-time job opportunities or freelance work to supplement your primary income. Online platforms like Fiverr and Upwork provide avenues to showcase your skills and secure freelance projects that align with your expertise and interests.

- Start a Side Hustle: Launching a side hustle can be a lucrative way to generate additional income streams. Explore a variety of gig economy apps and platforms that cater to different skill sets and interests. From dog walking and food delivery to photography and secret shopping, there’s a plethora of opportunities to leverage your talents and earn extra cash.

By diversifying your income sources and leveraging your skills and expertise, you can take proactive steps to increase your income after taxes and achieve greater financial stability and success.

Remember to assess each strategy’s feasibility and alignment with your long-term goals before taking action.

Will a Salary of $66,000 Help Me Become Rich?

Earning a salary of $66,000 annually can serve as a stepping stone toward building wealth and achieving financial stability.

However, whether this income level translates into being ‘rich’ depends on a multitude of factors that shape your financial journey.

Let’s dive into these considerations in detail:

- Financial Goals:

- Defining what “rich” means to you is paramount. It could entail achieving financial security to cover living expenses and retirement comfortably or accumulating substantial wealth. Your specific financial aspirations will dictate your perception of wealth and guide your financial decisions.

- Lifestyle Choices:

- Your spending habits and lifestyle choices wield significant influence over your ability to amass wealth. Even with a modest salary, excessive spending or debt accumulation can impede your path to financial prosperity. Prioritizing budgeting, practicing mindful spending, and living below your means are crucial habits to cultivate.

- Savings and Investments:

- Wealth accumulation often entails saving a significant portion of your income and making prudent investment choices. With a $66,000 salary, it is certainly possible to save and invest. Consider allocating funds to retirement accounts, exploring investment avenues such as stocks or real estate, and diversifying your portfolio to maximize growth potential.

- Debt Management:

- Effectively managing and reducing debt is pivotal for building wealth. Whether it’s student loans, credit card debt, or mortgages, high-interest debt can hinder your financial progress. Prioritize debt repayment to free up resources for saving and investing.

- Cost of Living:

- The cost of living in your area significantly impacts your financial outlook. In regions with a high cost of living, making ends meet and saving for the future may pose greater challenges, even with a decent salary. Adjust your financial plan accordingly to navigate these circumstances effectively.

- Investment Strategy:

- Your investment strategy plays a crucial role in wealth accumulation. Consider factors such as asset allocation, risk tolerance, and long-term planning when formulating your investment approach. Seeking guidance from a financial advisor can provide valuable insights to optimize your investment decisions.

- Time Horizon:

- Building substantial wealth requires patience and consistency over time. The longer your investment horizon, the greater the potential for growth through compounding returns. Embrace a long-term perspective and stay committed to your financial goals.

In summary, while a $66,000 salary offers a solid foundation for building wealth, achieving financial success goes beyond income alone.

Define your financial aspirations, adopt prudent financial habits, and craft a comprehensive financial plan tailored to your goals to embark on the path toward true financial prosperity.

How to Reduce My Taxes if I Make $66,000

Navigating the tax landscape effectively can help individuals earning $66,000 maximize their take-home pay and reduce their tax burden.

Here are several detailed strategies to consider:

- Take Advantage of Tax Deductions:

- Explore available tax deductions to lower your taxable income. Common deductions include contributions to retirement accounts (such as a Traditional IRA or 401(k)), mortgage interest, property taxes, charitable donations, and eligible medical expenses. Keep meticulous records of deductible expenses throughout the year to ensure you claim all applicable deductions at tax time.

- Utilize Tax Credits:

- Tax credits directly reduce your tax liability dollar-for-dollar, making them particularly valuable. Consider tax credits such as the Earned Income Tax Credit (EITC), which is designed to assist low-to-moderate-income individuals and families. Other credits, such as the Child Tax Credit or the Saver’s Credit for retirement contributions, may also be available to you based on your circumstances.

- Contribute to Retirement Accounts:

- Contributing to tax-advantaged retirement accounts not only helps you save for the future but also provides immediate tax benefits. Contributions to a Traditional IRA or employer-sponsored retirement plan (such as a 401(k) or 403(b)) are typically tax-deductible, reducing your taxable income for the year. Aim to maximize your contributions to these accounts within IRS limits to take full advantage of the tax benefits they offer.

- Explore Tax-Advantaged Savings Vehicles:

- Consider utilizing tax-advantaged savings vehicles such as Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs). Contributions to an HSA are tax-deductible, and withdrawals for qualified medical expenses are tax-free, providing a triple tax advantage. Similarly, contributions to an FSA for healthcare or dependent care expenses are made with pre-tax dollars, reducing your taxable income.

- Claim Education-related Tax Benefits:

- If you’re pursuing higher education or supporting a dependent’s education expenses, explore available tax benefits. The American Opportunity Tax Credit and the Lifetime Learning Credit can help offset the costs of tuition, fees, and other qualified education expenses, reducing your tax liability.

- Consider Tax-efficient Investments:

- When investing, opt for tax-efficient investment strategies to minimize taxable gains and income. Focus on investments with favorable tax treatment, such as long-term capital gains and qualified dividends, which are taxed at lower rates than ordinary income. Additionally, consider investing in tax-exempt municipal bonds or tax-advantaged retirement accounts to reduce your taxable investment income.

By implementing these tax reduction strategies strategically, individuals earning $66,000 can optimize their tax situation, retain more of their hard-earned income, and achieve greater financial flexibility and stability.

Be sure to consult with a tax professional or financial advisor to tailor these strategies to your specific circumstances and objectives.

Final Thoughts

In conclusion, understanding the significance of your monthly after-tax income offers valuable insights into your overall financial health.

It’s more than just a numerical figure; rather, it serves as a pivotal indicator of how well your earnings align with your financial objectives, lifestyle preferences, and the cost of living in your area.

By understanding and effectively managing your after-tax income, you can make informed financial decisions, pursue your goals with confidence, and strive for greater financial stability and success in the long run.

By: Chris Bemis

When you’re navigating the job market or budgeting for your future, knowing what your annual salary translates to in terms of a monthly wage can be incredibly helpful.

In this article, we’ll break down the math and explore what $65,000 a year means on a monthly basis after tax.

We’ll also dive into topics such as post-tax income and whether $65,000 a year can be considered a good salary. Plus, we’ll share tips on how you can potentially increase your hourly wage.

Let’s get into the details now of how much $65,000 a year is a month after taxes.

$65,000 a Year is How Much a Month After Taxes?

Understanding your take-home pay is crucial when planning your finances. The amount you receive after taxes depends on various factors, including your tax filing status, deductions, and the state you reside in.

On average, individuals can expect to pay around 20-30% or more of their income in federal and state income taxes. Let’s take some data from the IRS website on what your tax rate will be according to your income. This does not account for any of the factors listed above.

- 37% for incomes over $578,125 ($693,750 for married couples filing jointly)

- 35% for incomes over $231,250 ($462,500 for married couples filing jointly)

- 32% for incomes over $182,100 ($364,200 for married couples filing jointly)

- 24% for incomes over $95,375 ($190,750 for married couples filing jointly)

- 22% for incomes over $44,725 ($89,450 for married couples filing jointly)

- 12% for incomes over $11,000 ($22,000 for married couples filing jointly)

So at a $65,000 annual income, we will assume a tax rate of 22%.

$65,000 (annual income) x 22% (tax rate) = $14,300

So, after taxes, you would have approximately $50,700 left as your annual income.

To calculate your monthly income after taxes, you can divide $50,700 by 12 (since there are 12 months in a year):

$50,700 (annual income after tax) / 12 (months) = $4,225

So, at a yearly salary of $65,000, your monthly income after taxes would be approximately $4,225.

While this is a decent estimate, your monthly after-tax income can be different depending on a variety of factors.

Factors that Determine Your After-Tax Income

Your monthly after-tax income can vary depending on a multitude of factors, including:

- Tax Filing Status: Your filing status, such as single, married filing jointly, married filing separately, or head of household, can impact your tax liability and ultimately affect your after-tax income.

- Tax Deductions: The deductions you claim, such as the standard deduction or itemized deductions for expenses like mortgage interest, property taxes, and charitable contributions, can reduce your taxable income and lower your tax bill.

- Tax Credits: Tax credits directly reduce the amount of tax you owe, potentially leading to a lower tax liability and higher after-tax income. Common tax credits include the Earned Income Tax Credit (EITC), Child Tax Credit, and education-related credits.

- State and Local Taxes: The amount of state and local taxes you owe can vary based on your state of residence and local tax rates. Some states have no income tax, while others impose state income taxes in addition to federal taxes.

- Additional Withholdings: If you choose to have additional taxes withheld from your paycheck, either voluntarily or to cover other tax liabilities such as self-employment taxes, it can affect your after-tax income.

- Retirement Contributions: Contributions to retirement accounts such as a 401(k) or Traditional IRA can reduce your taxable income, potentially lowering your tax liability and increasing your after-tax income.

- Other Deductions and Adjustments: Various other deductions and adjustments to income, such as student loan interest deduction, tuition and fees deduction, or contributions to Health Savings Accounts (HSAs), can impact your taxable income and ultimately affect your after-tax income.

Overall, your monthly after-tax income is influenced by a complex interplay of factors related to your income, deductions, credits, and tax withholding preferences.

Understanding these factors and their implications can help you better manage your finances and plan for your financial future.

Next, let’s look at if $65,000 a year is a good salary.

Is $65,000 a Year a Good Salary?

Whether $65,000 a year is considered a good salary depends on various factors, including your location, cost of living, and personal financial goals. In some areas with a lower cost of living, $65,000 can provide a comfortable life. However, in more expensive cities, it may not stretch as far.

To determine if it’s sufficient for your needs, consider your monthly expenses, such as housing, utilities, transportation, groceries, and savings goals.

Additionally, factors like job benefits, opportunities for advancement, and job satisfaction play a significant role in evaluating the overall value of your wage.

Let’s take a look at how a $65,000 a year salary compares to others in the United States.

According to data from the US Census Bureau for 2022, the median income for Nonfamily households in the United States was approximately $45,440 – which means that half of all individuals earned more than this amount, and half earned less.

So, if you have a salary of $65,000, you have a salary that is in the top 50 percent of all earners in the United States. With annual pay of over $45,400, you are doing well and are part of a above-average group of earners in the United States.

How to Increase Your Income

When aiming to increase your income and bolster your financial resources, it’s crucial to consider a range of effective strategies:

- Skill Development: Invest in enhancing your existing skills or acquiring new ones that are highly valued in your industry. Keeping pace with evolving trends and technologies can significantly boost your marketability and earning potential.

- Negotiation: Don’t shy away from negotiating your wage when starting a new job or during performance evaluations. Demonstrating your value to employers and advocating for fair compensation can lead to substantial salary increases over time.

- Further Education: Explore opportunities for additional education or certifications that can augment your qualifications and increase your worth in the job market. Continuing education demonstrates your commitment to professional growth and can open doors to higher-paying roles.

- Job Switch: Consider transitioning to a different job or company if it presents opportunities for a significant salary bump. Assess the market demand for your skills and explore job openings that offer competitive compensation packages and room for advancement.

- Freelancing or Part-Time Work: Explore part-time job opportunities or freelance work to supplement your primary income. Online platforms like Fiverr and Upwork provide avenues to showcase your skills and secure freelance projects that align with your expertise and interests.

- Start a Side Hustle: Launching a side hustle can be a lucrative way to generate additional income streams. Explore a variety of gig economy apps and platforms that cater to different skill sets and interests. From dog walking and food delivery to photography and secret shopping, there’s a plethora of opportunities to leverage your talents and earn extra cash.

By diversifying your income sources and leveraging your skills and expertise, you can take proactive steps to increase your income after taxes and achieve greater financial stability and success.

Remember to assess each strategy’s feasibility and alignment with your long-term goals before taking action.

Will a Salary of $65,000 Help Me Become Rich?

Earning a salary of $65,000 annually can serve as a stepping stone toward building wealth and achieving financial stability.

However, whether this income level translates into being ‘rich’ depends on a multitude of factors that shape your financial journey.

Let’s dive into these considerations in detail:

- Financial Goals:

- Defining what “rich” means to you is paramount. It could entail achieving financial security to cover living expenses and retirement comfortably or accumulating substantial wealth. Your specific financial aspirations will dictate your perception of wealth and guide your financial decisions.

- Lifestyle Choices:

- Your spending habits and lifestyle choices wield significant influence over your ability to amass wealth. Even with a modest salary, excessive spending or debt accumulation can impede your path to financial prosperity. Prioritizing budgeting, practicing mindful spending, and living below your means are crucial habits to cultivate.

- Savings and Investments:

- Wealth accumulation often entails saving a significant portion of your income and making prudent investment choices. With a $65,000 salary, it is certainly possible to save and invest. Consider allocating funds to retirement accounts, exploring investment avenues such as stocks or real estate, and diversifying your portfolio to maximize growth potential.

- Debt Management:

- Effectively managing and reducing debt is pivotal for building wealth. Whether it’s student loans, credit card debt, or mortgages, high-interest debt can hinder your financial progress. Prioritize debt repayment to free up resources for saving and investing.

- Cost of Living:

- The cost of living in your area significantly impacts your financial outlook. In regions with a high cost of living, making ends meet and saving for the future may pose greater challenges, even with a decent salary. Adjust your financial plan accordingly to navigate these circumstances effectively.

- Investment Strategy:

- Your investment strategy plays a crucial role in wealth accumulation. Consider factors such as asset allocation, risk tolerance, and long-term planning when formulating your investment approach. Seeking guidance from a financial advisor can provide valuable insights to optimize your investment decisions.

- Time Horizon:

- Building substantial wealth requires patience and consistency over time. The longer your investment horizon, the greater the potential for growth through compounding returns. Embrace a long-term perspective and stay committed to your financial goals.

In summary, while a $65,000 salary offers a solid foundation for building wealth, achieving financial success goes beyond income alone.

Define your financial aspirations, adopt prudent financial habits, and craft a comprehensive financial plan tailored to your goals to embark on the path toward true financial prosperity.

How to Reduce My Taxes if I Make $65,000

Navigating the tax landscape effectively can help individuals earning $65,000 maximize their take-home pay and reduce their tax burden.

Here are several detailed strategies to consider:

- Take Advantage of Tax Deductions:

- Explore available tax deductions to lower your taxable income. Common deductions include contributions to retirement accounts (such as a Traditional IRA or 401(k)), mortgage interest, property taxes, charitable donations, and eligible medical expenses. Keep meticulous records of deductible expenses throughout the year to ensure you claim all applicable deductions at tax time.

- Utilize Tax Credits:

- Tax credits directly reduce your tax liability dollar-for-dollar, making them particularly valuable. Consider tax credits such as the Earned Income Tax Credit (EITC), which is designed to assist low-to-moderate-income individuals and families. Other credits, such as the Child Tax Credit or the Saver’s Credit for retirement contributions, may also be available to you based on your circumstances.

- Contribute to Retirement Accounts:

- Contributing to tax-advantaged retirement accounts not only helps you save for the future but also provides immediate tax benefits. Contributions to a Traditional IRA or employer-sponsored retirement plan (such as a 401(k) or 403(b)) are typically tax-deductible, reducing your taxable income for the year. Aim to maximize your contributions to these accounts within IRS limits to take full advantage of the tax benefits they offer.

- Explore Tax-Advantaged Savings Vehicles:

- Consider utilizing tax-advantaged savings vehicles such as Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs). Contributions to an HSA are tax-deductible, and withdrawals for qualified medical expenses are tax-free, providing a triple tax advantage. Similarly, contributions to an FSA for healthcare or dependent care expenses are made with pre-tax dollars, reducing your taxable income.

- Claim Education-related Tax Benefits:

- If you’re pursuing higher education or supporting a dependent’s education expenses, explore available tax benefits. The American Opportunity Tax Credit and the Lifetime Learning Credit can help offset the costs of tuition, fees, and other qualified education expenses, reducing your tax liability.

- Consider Tax-efficient Investments:

- When investing, opt for tax-efficient investment strategies to minimize taxable gains and income. Focus on investments with favorable tax treatment, such as long-term capital gains and qualified dividends, which are taxed at lower rates than ordinary income. Additionally, consider investing in tax-exempt municipal bonds or tax-advantaged retirement accounts to reduce your taxable investment income.

By implementing these tax reduction strategies strategically, individuals earning $65,000 can optimize their tax situation, retain more of their hard-earned income, and achieve greater financial flexibility and stability.

Be sure to consult with a tax professional or financial advisor to tailor these strategies to your specific circumstances and objectives.

Final Thoughts

In conclusion, understanding the significance of your monthly after-tax income offers valuable insights into your overall financial health.

It’s more than just a numerical figure; rather, it serves as a pivotal indicator of how well your earnings align with your financial objectives, lifestyle preferences, and the cost of living in your area.

By understanding and effectively managing your after-tax income, you can make informed financial decisions, pursue your goals with confidence, and strive for greater financial stability and success in the long run.

When you’re navigating the job market or budgeting for your future, knowing what your annual salary translates to in terms of a monthly wage can be incredibly helpful.

In this article, we’ll break down the math and explore what $64,000 a year means on a monthly basis after tax.

We’ll also dive into topics such as post-tax income and whether $64,000 a year can be considered a good salary. Plus, we’ll share tips on how you can potentially increase your hourly wage.

Let’s get into the details now of how much $64,000 a year is a month after taxes.

$64,000 a Year is How Much a Month After Taxes?

Understanding your take-home pay is crucial when planning your finances. The amount you receive after taxes depends on various factors, including your tax filing status, deductions, and the state you reside in.

On average, individuals can expect to pay around 20-30% or more of their income in federal and state income taxes. Let’s take some data from the IRS website on what your tax rate will be according to your income. This does not account for any of the factors listed above.

- 37% for incomes over $578,125 ($693,750 for married couples filing jointly)

- 35% for incomes over $231,250 ($462,500 for married couples filing jointly)

- 32% for incomes over $182,100 ($364,200 for married couples filing jointly)

- 24% for incomes over $95,375 ($190,750 for married couples filing jointly)

- 22% for incomes over $44,725 ($89,450 for married couples filing jointly)

- 12% for incomes over $11,000 ($22,000 for married couples filing jointly)

So at a $64,000 annual income, we will assume a tax rate of 22%.

$64,000 (annual income) x 22% (tax rate) = $14,080

So, after taxes, you would have approximately $49,920 left as your annual income.

To calculate your monthly income after taxes, you can divide $49,920 by 12 (since there are 12 months in a year):

$49,920 (annual income after tax) / 12 (months) = $4,160

So, at a yearly salary of $64,000, your monthly income after taxes would be approximately $4,160.

While this is a decent estimate, your monthly after-tax income can be different depending on a variety of factors.

Factors that Determine Your After-Tax Income

Your monthly after-tax income can vary depending on a multitude of factors, including:

- Tax Filing Status: Your filing status, such as single, married filing jointly, married filing separately, or head of household, can impact your tax liability and ultimately affect your after-tax income.

- Tax Deductions: The deductions you claim, such as the standard deduction or itemized deductions for expenses like mortgage interest, property taxes, and charitable contributions, can reduce your taxable income and lower your tax bill.

- Tax Credits: Tax credits directly reduce the amount of tax you owe, potentially leading to a lower tax liability and higher after-tax income. Common tax credits include the Earned Income Tax Credit (EITC), Child Tax Credit, and education-related credits.

- State and Local Taxes: The amount of state and local taxes you owe can vary based on your state of residence and local tax rates. Some states have no income tax, while others impose state income taxes in addition to federal taxes.

- Additional Withholdings: If you choose to have additional taxes withheld from your paycheck, either voluntarily or to cover other tax liabilities such as self-employment taxes, it can affect your after-tax income.

- Retirement Contributions: Contributions to retirement accounts such as a 401(k) or Traditional IRA can reduce your taxable income, potentially lowering your tax liability and increasing your after-tax income.

- Other Deductions and Adjustments: Various other deductions and adjustments to income, such as student loan interest deduction, tuition and fees deduction, or contributions to Health Savings Accounts (HSAs), can impact your taxable income and ultimately affect your after-tax income.

Overall, your monthly after-tax income is influenced by a complex interplay of factors related to your income, deductions, credits, and tax withholding preferences.

Understanding these factors and their implications can help you better manage your finances and plan for your financial future.

Next, let’s look at if $64,000 a year is a good salary.

Is $64,000 a Year a Good Salary?

Whether $64,000 a year is considered a good salary depends on various factors, including your location, cost of living, and personal financial goals. In some areas with a lower cost of living, $64,000 can provide a comfortable life. However, in more expensive cities, it may not stretch as far.

To determine if it’s sufficient for your needs, consider your monthly expenses, such as housing, utilities, transportation, groceries, and savings goals.

Additionally, factors like job benefits, opportunities for advancement, and job satisfaction play a significant role in evaluating the overall value of your wage.

Let’s take a look at how a $64,000 a year salary compares to others in the United States.

According to data from the US Census Bureau for 2022, the median income for Nonfamily households in the United States was approximately $45,440 – which means that half of all individuals earned more than this amount, and half earned less.

So, if you have a salary of $64,000, you have a salary that is in the top 50 percent of all earners in the United States. With annual pay of over $45,400, you are doing well and are part of a above-average group of earners in the United States.

How to Increase Your Income

When aiming to increase your income and bolster your financial resources, it’s crucial to consider a range of effective strategies:

- Skill Development: Invest in enhancing your existing skills or acquiring new ones that are highly valued in your industry. Keeping pace with evolving trends and technologies can significantly boost your marketability and earning potential.

- Negotiation: Don’t shy away from negotiating your wage when starting a new job or during performance evaluations. Demonstrating your value to employers and advocating for fair compensation can lead to substantial salary increases over time.

- Further Education: Explore opportunities for additional education or certifications that can augment your qualifications and increase your worth in the job market. Continuing education demonstrates your commitment to professional growth and can open doors to higher-paying roles.

- Job Switch: Consider transitioning to a different job or company if it presents opportunities for a significant salary bump. Assess the market demand for your skills and explore job openings that offer competitive compensation packages and room for advancement.

- Freelancing or Part-Time Work: Explore part-time job opportunities or freelance work to supplement your primary income. Online platforms like Fiverr and Upwork provide avenues to showcase your skills and secure freelance projects that align with your expertise and interests.

- Start a Side Hustle: Launching a side hustle can be a lucrative way to generate additional income streams. Explore a variety of gig economy apps and platforms that cater to different skill sets and interests. From dog walking and food delivery to photography and secret shopping, there’s a plethora of opportunities to leverage your talents and earn extra cash.

By diversifying your income sources and leveraging your skills and expertise, you can take proactive steps to increase your income after taxes and achieve greater financial stability and success.

Remember to assess each strategy’s feasibility and alignment with your long-term goals before taking action.

Will a Salary of $64,000 Help Me Become Rich?

Earning a salary of $64,000 annually can serve as a stepping stone toward building wealth and achieving financial stability.

However, whether this income level translates into being ‘rich’ depends on a multitude of factors that shape your financial journey.

Let’s dive into these considerations in detail:

- Financial Goals:

- Defining what “rich” means to you is paramount. It could entail achieving financial security to cover living expenses and retirement comfortably or accumulating substantial wealth. Your specific financial aspirations will dictate your perception of wealth and guide your financial decisions.

- Lifestyle Choices:

- Your spending habits and lifestyle choices wield significant influence over your ability to amass wealth. Even with a modest salary, excessive spending or debt accumulation can impede your path to financial prosperity. Prioritizing budgeting, practicing mindful spending, and living below your means are crucial habits to cultivate.

- Savings and Investments:

- Wealth accumulation often entails saving a significant portion of your income and making prudent investment choices. With a $64,000 salary, it is certainly possible to save and invest. Consider allocating funds to retirement accounts, exploring investment avenues such as stocks or real estate, and diversifying your portfolio to maximize growth potential.

- Debt Management:

- Effectively managing and reducing debt is pivotal for building wealth. Whether it’s student loans, credit card debt, or mortgages, high-interest debt can hinder your financial progress. Prioritize debt repayment to free up resources for saving and investing.

- Cost of Living:

- The cost of living in your area significantly impacts your financial outlook. In regions with a high cost of living, making ends meet and saving for the future may pose greater challenges, even with a decent salary. Adjust your financial plan accordingly to navigate these circumstances effectively.

- Investment Strategy:

- Your investment strategy plays a crucial role in wealth accumulation. Consider factors such as asset allocation, risk tolerance, and long-term planning when formulating your investment approach. Seeking guidance from a financial advisor can provide valuable insights to optimize your investment decisions.

- Time Horizon:

- Building substantial wealth requires patience and consistency over time. The longer your investment horizon, the greater the potential for growth through compounding returns. Embrace a long-term perspective and stay committed to your financial goals.

In summary, while a $64,000 salary offers a solid foundation for building wealth, achieving financial success goes beyond income alone.

Define your financial aspirations, adopt prudent financial habits, and craft a comprehensive financial plan tailored to your goals to embark on the path toward true financial prosperity.

How to Reduce My Taxes if I Make $64,000

Navigating the tax landscape effectively can help individuals earning $64,000 maximize their take-home pay and reduce their tax burden.

Here are several detailed strategies to consider:

- Take Advantage of Tax Deductions:

- Explore available tax deductions to lower your taxable income. Common deductions include contributions to retirement accounts (such as a Traditional IRA or 401(k)), mortgage interest, property taxes, charitable donations, and eligible medical expenses. Keep meticulous records of deductible expenses throughout the year to ensure you claim all applicable deductions at tax time.

- Utilize Tax Credits:

- Tax credits directly reduce your tax liability dollar-for-dollar, making them particularly valuable. Consider tax credits such as the Earned Income Tax Credit (EITC), which is designed to assist low-to-moderate-income individuals and families. Other credits, such as the Child Tax Credit or the Saver’s Credit for retirement contributions, may also be available to you based on your circumstances.

- Contribute to Retirement Accounts:

- Contributing to tax-advantaged retirement accounts not only helps you save for the future but also provides immediate tax benefits. Contributions to a Traditional IRA or employer-sponsored retirement plan (such as a 401(k) or 403(b)) are typically tax-deductible, reducing your taxable income for the year. Aim to maximize your contributions to these accounts within IRS limits to take full advantage of the tax benefits they offer.

- Explore Tax-Advantaged Savings Vehicles:

- Consider utilizing tax-advantaged savings vehicles such as Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs). Contributions to an HSA are tax-deductible, and withdrawals for qualified medical expenses are tax-free, providing a triple tax advantage. Similarly, contributions to an FSA for healthcare or dependent care expenses are made with pre-tax dollars, reducing your taxable income.

- Claim Education-related Tax Benefits:

- If you’re pursuing higher education or supporting a dependent’s education expenses, explore available tax benefits. The American Opportunity Tax Credit and the Lifetime Learning Credit can help offset the costs of tuition, fees, and other qualified education expenses, reducing your tax liability.

- Consider Tax-efficient Investments:

- When investing, opt for tax-efficient investment strategies to minimize taxable gains and income. Focus on investments with favorable tax treatment, such as long-term capital gains and qualified dividends, which are taxed at lower rates than ordinary income. Additionally, consider investing in tax-exempt municipal bonds or tax-advantaged retirement accounts to reduce your taxable investment income.

By implementing these tax reduction strategies strategically, individuals earning $64,000 can optimize their tax situation, retain more of their hard-earned income, and achieve greater financial flexibility and stability.

Be sure to consult with a tax professional or financial advisor to tailor these strategies to your specific circumstances and objectives.

Final Thoughts

In conclusion, understanding the significance of your monthly after-tax income offers valuable insights into your overall financial health.

It’s more than just a numerical figure; rather, it serves as a pivotal indicator of how well your earnings align with your financial objectives, lifestyle preferences, and the cost of living in your area.

By understanding and effectively managing your after-tax income, you can make informed financial decisions, pursue your goals with confidence, and strive for greater financial stability and success in the long run.

In the world of personal finance and career aspirations, the phrase “five figures” carries a weighty significance. It’s a benchmark that many strive to achieve, a milestone signaling financial success and stability.

But what exactly does it mean to earn five figures? More specifically, how much is 5 figures?

Simply put, 5 figures refers to a number with five digits. 5 figures covers the amounts from $10,000 to $99,999.

But, the question “how much is 5 figures?” is more complicated than just the simple answer.

In this article, we look at the intricacies of this term, demystifying what lies within the definition of five figures.

From its numerical definition to its implications on earnings and lifestyle, let’s explore the ins and outs of “how much is 5 figures?”

What is 5 Figures?

In salary discussions, the term “figure” takes on a specific meaning. While in mathematics, a figure denotes any digit or number, in the context of earnings, only the dollar amount on your paycheck is considered.

Let’s break it down with examples:

Suppose your annual income amounts to $73,500. In this case, your salary falls within the five-figure range, earning you the title of a five-figure earner.

In another example, if your yearly earnings soar to $1,250,000, congratulations, you’ve entered the illustrious world of seven figures or 1 million dollars a year, making you a seven-figure earner.

If you have a net worth of $500,000, you have a six-figure net worth.

How Much is 5 Figures?

Understanding the term “5 figures” is pivotal in grasping the scale of earnings it encompasses. Essentially, when we say “5 figures,” we’re referring to numerical values comprised of five digits.

This range spans from $10,000, the starting point, to $99,999, the upper limit. This range encompasses various income levels and is a common milestone for individuals in their careers.

Let’s explore some examples:

- A graphic designer earning $60,000 per year has a five-figure income. This income level reflects the designer’s expertise and experience in the field, positioning them within the five-figure bracket and providing financial stability in their career.

- A registered nurse with an annual salary of $75,000 falls within the five-figure bracket. As healthcare professionals, registered nurses play a crucial role in patient care, and their earnings reflect the value they bring to their profession.

- A marketing manager making $90,000 annually also earns a five-figure income. Marketing managers are responsible for developing and implementing strategies to promote products or services, and their salary reflects their leadership and expertise in driving business growth.

These examples demonstrate the diverse range of occupations that fall within the five-figure income bracket, showcasing the value of skills, experience, and expertise in achieving financial success.

How Much is 5 Figures After Taxes

Understanding your take-home pay is crucial when planning your finances. The amount you receive after taxes depends on various factors, including your tax filing status, deductions, and the state you reside in.

On average, individuals can expect to pay around 20-30% or more of their income in federal and state income taxes. Let’s take some data from the IRS website on what your tax rate will be according to your income. This does not account for any of the factors listed above.

- 37% for incomes over $578,125 ($693,750 for married couples filing jointly)

- 35% for incomes over $231,250 ($462,500 for married couples filing jointly)

- 32% for incomes over $182,100 ($364,200 for married couples filing jointly)

- 24% for incomes over $95,375 ($190,750 for married couples filing jointly)

- 22% for incomes over $44,725 ($89,450 for married couples filing jointly)

- 12% for incomes over $11,000 ($22,000 for married couples filing jointly)

If you are making 5 figures, then you will be in the lower tax brackets.

Below are a few examples of different tax situations based on level of income in the 5 figure range.

- Annual Income: $40,000

- Tax Bracket: 12%

- Estimated Tax: $4,800

- Take-Home Pay: $35,200

- Annual Income: $75,000

- Tax Bracket: 22%

- Estimated Tax: $18,000

- Take-Home Pay: $57,000

- Annual Income: $97,000

- Tax Bracket: 24%

- Estimated Tax: $23,280

- Take-Home Pay: $73,720

These estimates provide a general idea of the take-home pay for individuals earning five-figure incomes after taxes. However, it’s important to note that actual amounts may vary depending on individual circumstances, deductions, and other factors.

Additionally, the progressive nature of the tax system means that higher incomes are subject to higher tax rates, resulting in a lower percentage of income retained after taxes compared to lower income levels.

How Much a Month is 5 Figures a Year?

Determining the monthly income equivalent of a five-figure annual salary is essential for budgeting and financial planning.

To calculate this, we’ll divide the annual income by 12 months to find the monthly amount.

Let’s explore detailed examples for different five-figure salary levels:

- Annual Income: $60,000

- Monthly Income: $60,000/12 = $5,000

- Annual Income: $75,000

- Monthly Income: $75,000/12 = $6,250

- Annual Income: $90,000

- Monthly Income: $90,000/12 = $7,500

These examples highlight how the monthly income from a five-figure annual salary varies depending on the specific earnings level. It’s important to note that these figures represent gross income before taxes and deductions.

As we looked at in the previous section, actual take-home pay may differ based on factors such as tax withholding, retirement contributions, and other deductions.

Understanding the monthly equivalent of a five-figure salary is crucial for budgeting, saving, and planning expenses effectively.

Is it Good if You Make 5 Figures?

According to data from the US Census Bureau for 2022, the median income for Nonfamily households in the United States was approximately $45,440 – which means that half of all individuals earned more than this amount, and half earned less.

So, if you have a salary of 5 figures, you might be doing well but need to compare yourself to the chart above.

Examples of 5 Figure Salary Jobs

For jobs, there exists a diverse array of occupations that offer salaries falling within the five-figure range, typically ranging from $50,000 to $90,000 annually. Let’s explore five examples of such jobs:

- Software Developer:

- Software developers play a pivotal role in designing, testing, and maintaining computer programs and applications. With the increasing demand for technological solutions across industries, software developers command salaries in the five-figure range. Depending on experience and expertise, software developers can earn between $60,000 to $90,000 annually.

- Registered Nurse:

- Registered nurses provide critical healthcare services, including patient care, medication administration, and treatment coordination. Due to the essential nature of their work and the ongoing demand for healthcare professionals, registered nurses typically earn salaries ranging from $50,000 to $80,000 annually.

- Marketing Manager:

- Marketing managers are responsible for developing and implementing marketing strategies to promote products or services, drive sales, and enhance brand visibility. With their leadership skills and expertise in market analysis, marketing managers command salaries in the five-figure range, often ranging from $60,000 to $90,000 annually.

- Financial Analyst:

- Financial analysts assess economic trends, analyze financial data, and provide insights to help organizations make informed investment decisions. Given the specialized skill set and expertise required for this role, financial analysts typically earn salaries ranging from $60,000 to $80,000 annually.

- Civil Engineer:

- Civil engineers design, plan, and oversee construction projects, such as bridges, roads, and buildings, to ensure structural integrity and compliance with regulations. With their expertise in engineering principles and project management, civil engineers command salaries in the five-figure range, typically ranging from $60,000 to $90,000 annually.

These examples showcase a range of professions across different industries that offer competitive salaries within the five-figure range. Each of these roles requires specialized skills, education, and experience, making them desirable career paths for individuals seeking financial stability and professional growth.

Next, let’s talk about how you can increase your income to 5 figures if you aren’t making 5 figures.

How to Increase Your Income to 5 Figures

If you’re aiming to elevate your income to five figures, there are various effective strategies you can explore:

- Skill Development: Invest in enhancing your existing skills or acquiring new ones that are highly sought after in your industry. Continuous learning and skill improvement can significantly boost your earning potential.

- Negotiation: Don’t underestimate the power of negotiation when it comes to your salary. Whether you’re starting a new job or undergoing performance evaluations, confidently advocate for fair compensation that aligns with your value and contributions.

- Further Education: Consider pursuing advanced degrees, certifications, or specialized training programs that can enhance your qualifications and increase your marketability in the job market. Higher levels of education often correlate with higher earning potential.

- Job Switch: Sometimes, transitioning to a different job or company can result in a substantial salary increase. Explore opportunities in your field or related industries that offer competitive compensation packages and room for career growth.

- Freelancing or Part-Time Work: Supplement your primary income by taking on freelance projects or part-time work opportunities. Online platforms like Fiverr, Upwork, and TaskRabbit offer a plethora of gigs across various industries that allow you to leverage your skills and expertise for additional income.

- Start a Side Hustle: Launching a side hustle can be a lucrative way to generate extra income outside of your regular job. Explore a range of gig economy opportunities, such as dog walking/sitting, food delivery, photography, mystery shopping, and more.

By implementing these strategies and actively seeking opportunities to increase your income, you can work towards achieving your goal of earning a five-figure salary and securing financial stability for the future.

Can You Get Rich Making 5 Figures?

Earning a five-figure income can serve as a solid foundation for wealth building and financial success.

However, whether it leads to true wealth, or what some may consider being ‘rich,’ hinges on several crucial factors.

Let’s dive into these considerations:

- Financial Goals:

- Defining what “rich” means to you is essential. For some, it’s about achieving financial security and having enough to cover living expenses and retirement comfortably. For others, it may involve accumulating significant wealth. Your unique financial goals will shape your perception of wealth.

- Lifestyle Choices:

- Your spending habits and lifestyle choices profoundly impact your ability to accumulate wealth. Regardless of your income level, excessive spending or accumulating debt can impede your journey toward financial prosperity. Adopting budgeting techniques, practicing mindful spending, and living within your means are pivotal.

- Savings and Investments:

- Building wealth necessitates saving a substantial portion of your income and making astute investments. A higher income affords you the opportunity to save and invest more, accelerating your wealth accumulation. Consider contributing to retirement accounts, delving into stocks or real estate, and diversifying your investment portfolio.

- Debt Management:

- Managing and reducing debt, whether it’s student loans, credit card debt, or mortgages, is critical for building wealth. High-interest debt can impede your financial progress, so prioritizing debt repayment is crucial.

- Cost of Living:

- The cost of living in your area significantly influences your ability to save and invest. In regions with a high cost of living, it may be more challenging to accumulate wealth, even with a substantial income.

- Investment Strategy:

- Your investment strategy, including asset allocation, risk tolerance, and long-term planning, plays a pivotal role in wealth accumulation. Seeking guidance from a financial advisor can aid in making informed investment decisions aligned with your financial goals.

- Time Horizon:

- Building significant wealth requires time and consistent effort. The longer your investment horizon, the greater the potential for wealth accumulation through compounding returns.

In summary, a 5-figure income provides a solid foundation for building wealth, but it’s not the salary alone that determines your financial success.

Becoming ‘rich’ is a subjective goal, so it’s essential to define what it means for you and create a financial plan to pursue it.

Final Thoughts

In conclusion, understanding the concept of “five figures” is not merely about numbers but signifies a significant milestone in one’s financial journey.

From the starting point of $10,000 to just shy of $100,000, a five-figure income represents substantial earning potential and financial stability for individuals across various professions and industries.

Whether it’s through specialized skills, advanced education, or years of experience, attaining a five-figure salary is a testament to dedication and hard work.

However, it’s essential to recognize that earning five figures is not the ultimate measure of success, and financial well-being encompasses more than just income. Effective budgeting, prudent financial management, and pursuing passions and interests beyond monetary gains are equally important aspects of a fulfilling life.

By understanding the significance of five figures and embracing a holistic approach to finances, individuals can strive for both prosperity and fulfillment in their personal and professional endeavors.

When you’re navigating the job market or budgeting for your future, knowing what your annual salary translates to in terms of a monthly wage can be incredibly helpful.

In this article, we’ll break down the math and explore what $63,000 a year means on a monthly basis after tax.

We’ll also dive into topics such as post-tax income and whether $63,000 a year can be considered a good salary. Plus, we’ll share tips on how you can potentially increase your hourly wage.

Let’s get into the details now of how much $63,000 a year is a month after taxes.

$63,000 a Year is How Much a Month After Taxes?

Understanding your take-home pay is crucial when planning your finances. The amount you receive after taxes depends on various factors, including your tax filing status, deductions, and the state you reside in.

On average, individuals can expect to pay around 20-30% or more of their income in federal and state income taxes. Let’s take some data from the IRS website on what your tax rate will be according to your income. This does not account for any of the factors listed above.

- 37% for incomes over $578,125 ($693,750 for married couples filing jointly)

- 35% for incomes over $231,250 ($462,500 for married couples filing jointly)

- 32% for incomes over $182,100 ($364,200 for married couples filing jointly)

- 24% for incomes over $95,375 ($190,750 for married couples filing jointly)

- 22% for incomes over $44,725 ($89,450 for married couples filing jointly)

- 12% for incomes over $11,000 ($22,000 for married couples filing jointly)

So at a $63,000 annual income, we will assume a tax rate of 22%.

$63,000 (annual income) x 22% (tax rate) = $13,860

So, after taxes, you would have approximately $49,140 left as your annual income.

To calculate your monthly income after taxes, you can divide $49,140 by 12 (since there are 12 months in a year):

$49,140 (annual income after tax) / 12 (months) = $4,095

So, at a yearly salary of $63,000, your monthly income after taxes would be approximately $4,095.

While this is a decent estimate, your monthly after-tax income can be different depending on a variety of factors.

Factors that Determine Your After-Tax Income

Your monthly after-tax income can vary depending on a multitude of factors, including:

- Tax Filing Status: Your filing status, such as single, married filing jointly, married filing separately, or head of household, can impact your tax liability and ultimately affect your after-tax income.

- Tax Deductions: The deductions you claim, such as the standard deduction or itemized deductions for expenses like mortgage interest, property taxes, and charitable contributions, can reduce your taxable income and lower your tax bill.

- Tax Credits: Tax credits directly reduce the amount of tax you owe, potentially leading to a lower tax liability and higher after-tax income. Common tax credits include the Earned Income Tax Credit (EITC), Child Tax Credit, and education-related credits.

- State and Local Taxes: The amount of state and local taxes you owe can vary based on your state of residence and local tax rates. Some states have no income tax, while others impose state income taxes in addition to federal taxes.

- Additional Withholdings: If you choose to have additional taxes withheld from your paycheck, either voluntarily or to cover other tax liabilities such as self-employment taxes, it can affect your after-tax income.

- Retirement Contributions: Contributions to retirement accounts such as a 401(k) or Traditional IRA can reduce your taxable income, potentially lowering your tax liability and increasing your after-tax income.

- Other Deductions and Adjustments: Various other deductions and adjustments to income, such as student loan interest deduction, tuition and fees deduction, or contributions to Health Savings Accounts (HSAs), can impact your taxable income and ultimately affect your after-tax income.

Overall, your monthly after-tax income is influenced by a complex interplay of factors related to your income, deductions, credits, and tax withholding preferences.

Understanding these factors and their implications can help you better manage your finances and plan for your financial future.

Next, let’s look at if $63,000 a year is a good salary.

Is $63,000 a Year a Good Salary?

Whether $63,000 a year is considered a good salary depends on various factors, including your location, cost of living, and personal financial goals. In some areas with a lower cost of living, $63,000 can provide a comfortable life. However, in more expensive cities, it may not stretch as far.

To determine if it’s sufficient for your needs, consider your monthly expenses, such as housing, utilities, transportation, groceries, and savings goals.

Additionally, factors like job benefits, opportunities for advancement, and job satisfaction play a significant role in evaluating the overall value of your wage.

Let’s take a look at how a $63,000 a year salary compares to others in the United States.

According to data from the US Census Bureau for 2022, the median income for Nonfamily households in the United States was approximately $45,440 – which means that half of all individuals earned more than this amount, and half earned less.

So, if you have a salary of $63,000, you have a salary that is in the top 50 percent of all earners in the United States. With annual pay of over $45,400, you are doing well and are part of a above-average group of earners in the United States.

How to Increase Your Income

When aiming to increase your income and bolster your financial resources, it’s crucial to consider a range of effective strategies:

- Skill Development: Invest in enhancing your existing skills or acquiring new ones that are highly valued in your industry. Keeping pace with evolving trends and technologies can significantly boost your marketability and earning potential.

- Negotiation: Don’t shy away from negotiating your wage when starting a new job or during performance evaluations. Demonstrating your value to employers and advocating for fair compensation can lead to substantial salary increases over time.

- Further Education: Explore opportunities for additional education or certifications that can augment your qualifications and increase your worth in the job market. Continuing education demonstrates your commitment to professional growth and can open doors to higher-paying roles.

- Job Switch: Consider transitioning to a different job or company if it presents opportunities for a significant salary bump. Assess the market demand for your skills and explore job openings that offer competitive compensation packages and room for advancement.

- Freelancing or Part-Time Work: Explore part-time job opportunities or freelance work to supplement your primary income. Online platforms like Fiverr and Upwork provide avenues to showcase your skills and secure freelance projects that align with your expertise and interests.

- Start a Side Hustle: Launching a side hustle can be a lucrative way to generate additional income streams. Explore a variety of gig economy apps and platforms that cater to different skill sets and interests. From dog walking and food delivery to photography and secret shopping, there’s a plethora of opportunities to leverage your talents and earn extra cash.

By diversifying your income sources and leveraging your skills and expertise, you can take proactive steps to increase your income after taxes and achieve greater financial stability and success.

Remember to assess each strategy’s feasibility and alignment with your long-term goals before taking action.

Will a Salary of $63,000 Help Me Become Rich?

Earning a salary of $63,000 annually can serve as a stepping stone toward building wealth and achieving financial stability.

However, whether this income level translates into being ‘rich’ depends on a multitude of factors that shape your financial journey.

Let’s dive into these considerations in detail:

- Financial Goals:

- Defining what “rich” means to you is paramount. It could entail achieving financial security to cover living expenses and retirement comfortably or accumulating substantial wealth. Your specific financial aspirations will dictate your perception of wealth and guide your financial decisions.

- Lifestyle Choices:

- Your spending habits and lifestyle choices wield significant influence over your ability to amass wealth. Even with a modest salary, excessive spending or debt accumulation can impede your path to financial prosperity. Prioritizing budgeting, practicing mindful spending, and living below your means are crucial habits to cultivate.

- Savings and Investments:

- Wealth accumulation often entails saving a significant portion of your income and making prudent investment choices. With a $63,000 salary, it is certainly possible to save and invest. Consider allocating funds to retirement accounts, exploring investment avenues such as stocks or real estate, and diversifying your portfolio to maximize growth potential.

- Debt Management:

- Effectively managing and reducing debt is pivotal for building wealth. Whether it’s student loans, credit card debt, or mortgages, high-interest debt can hinder your financial progress. Prioritize debt repayment to free up resources for saving and investing.

- Cost of Living:

- The cost of living in your area significantly impacts your financial outlook. In regions with a high cost of living, making ends meet and saving for the future may pose greater challenges, even with a decent salary. Adjust your financial plan accordingly to navigate these circumstances effectively.

- Investment Strategy:

- Your investment strategy plays a crucial role in wealth accumulation. Consider factors such as asset allocation, risk tolerance, and long-term planning when formulating your investment approach. Seeking guidance from a financial advisor can provide valuable insights to optimize your investment decisions.

- Time Horizon:

- Building substantial wealth requires patience and consistency over time. The longer your investment horizon, the greater the potential for growth through compounding returns. Embrace a long-term perspective and stay committed to your financial goals.

In summary, while a $63,000 salary offers a solid foundation for building wealth, achieving financial success goes beyond income alone.

Define your financial aspirations, adopt prudent financial habits, and craft a comprehensive financial plan tailored to your goals to embark on the path toward true financial prosperity.

How to Reduce My Taxes if I Make $63,000

Navigating the tax landscape effectively can help individuals earning $63,000 maximize their take-home pay and reduce their tax burden.

Here are several detailed strategies to consider:

- Take Advantage of Tax Deductions:

- Explore available tax deductions to lower your taxable income. Common deductions include contributions to retirement accounts (such as a Traditional IRA or 401(k)), mortgage interest, property taxes, charitable donations, and eligible medical expenses. Keep meticulous records of deductible expenses throughout the year to ensure you claim all applicable deductions at tax time.

- Utilize Tax Credits:

- Tax credits directly reduce your tax liability dollar-for-dollar, making them particularly valuable. Consider tax credits such as the Earned Income Tax Credit (EITC), which is designed to assist low-to-moderate-income individuals and families. Other credits, such as the Child Tax Credit or the Saver’s Credit for retirement contributions, may also be available to you based on your circumstances.

- Contribute to Retirement Accounts:

- Contributing to tax-advantaged retirement accounts not only helps you save for the future but also provides immediate tax benefits. Contributions to a Traditional IRA or employer-sponsored retirement plan (such as a 401(k) or 403(b)) are typically tax-deductible, reducing your taxable income for the year. Aim to maximize your contributions to these accounts within IRS limits to take full advantage of the tax benefits they offer.

- Explore Tax-Advantaged Savings Vehicles:

- Consider utilizing tax-advantaged savings vehicles such as Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs). Contributions to an HSA are tax-deductible, and withdrawals for qualified medical expenses are tax-free, providing a triple tax advantage. Similarly, contributions to an FSA for healthcare or dependent care expenses are made with pre-tax dollars, reducing your taxable income.

- Claim Education-related Tax Benefits:

- If you’re pursuing higher education or supporting a dependent’s education expenses, explore available tax benefits. The American Opportunity Tax Credit and the Lifetime Learning Credit can help offset the costs of tuition, fees, and other qualified education expenses, reducing your tax liability.

- Consider Tax-efficient Investments:

- When investing, opt for tax-efficient investment strategies to minimize taxable gains and income. Focus on investments with favorable tax treatment, such as long-term capital gains and qualified dividends, which are taxed at lower rates than ordinary income. Additionally, consider investing in tax-exempt municipal bonds or tax-advantaged retirement accounts to reduce your taxable investment income.

By implementing these tax reduction strategies strategically, individuals earning $63,000 can optimize their tax situation, retain more of their hard-earned income, and achieve greater financial flexibility and stability.

Be sure to consult with a tax professional or financial advisor to tailor these strategies to your specific circumstances and objectives.

Final Thoughts

In conclusion, understanding the significance of your monthly after-tax income offers valuable insights into your overall financial health.

It’s more than just a numerical figure; rather, it serves as a pivotal indicator of how well your earnings align with your financial objectives, lifestyle preferences, and the cost of living in your area.

By understanding and effectively managing your after-tax income, you can make informed financial decisions, pursue your goals with confidence, and strive for greater financial stability and success in the long run.

When you’re navigating the job market or budgeting for your future, knowing what your annual salary translates to in terms of a monthly wage can be incredibly helpful.

In this article, we’ll break down the math and explore what $62,000 a year means on a monthly basis after tax.

We’ll also dive into topics such as post-tax income and whether $62,000 a year can be considered a good salary. Plus, we’ll share tips on how you can potentially increase your hourly wage.

Let’s get into the details now of how much $62,000 a year is a month after taxes.

$62,000 a Year is How Much a Month After Taxes?

Understanding your take-home pay is crucial when planning your finances. The amount you receive after taxes depends on various factors, including your tax filing status, deductions, and the state you reside in.

On average, individuals can expect to pay around 20-30% or more of their income in federal and state income taxes. Let’s take some data from the IRS website on what your tax rate will be according to your income. This does not account for any of the factors listed above.

- 37% for incomes over $578,125 ($693,750 for married couples filing jointly)

- 35% for incomes over $231,250 ($462,500 for married couples filing jointly)

- 32% for incomes over $182,100 ($364,200 for married couples filing jointly)

- 24% for incomes over $95,375 ($190,750 for married couples filing jointly)

- 22% for incomes over $44,725 ($89,450 for married couples filing jointly)

- 12% for incomes over $11,000 ($22,000 for married couples filing jointly)

So at a $62,000 annual income, we will assume a tax rate of 22%.

$62,000 (annual income) x 22% (tax rate) = $13,640

So, after taxes, you would have approximately $48,360 left as your annual income.

To calculate your monthly income after taxes, you can divide $48,360 by 12 (since there are 12 months in a year):

$48,360 (annual income after tax) / 12 (months) = $4,030

So, at a yearly salary of $62,000, your monthly income after taxes would be approximately $4,030.

While this is a decent estimate, your monthly after-tax income can be different depending on a variety of factors.

Factors that Determine Your After-Tax Income

Your monthly after-tax income can vary depending on a multitude of factors, including:

- Tax Filing Status: Your filing status, such as single, married filing jointly, married filing separately, or head of household, can impact your tax liability and ultimately affect your after-tax income.

- Tax Deductions: The deductions you claim, such as the standard deduction or itemized deductions for expenses like mortgage interest, property taxes, and charitable contributions, can reduce your taxable income and lower your tax bill.

- Tax Credits: Tax credits directly reduce the amount of tax you owe, potentially leading to a lower tax liability and higher after-tax income. Common tax credits include the Earned Income Tax Credit (EITC), Child Tax Credit, and education-related credits.

- State and Local Taxes: The amount of state and local taxes you owe can vary based on your state of residence and local tax rates. Some states have no income tax, while others impose state income taxes in addition to federal taxes.

- Additional Withholdings: If you choose to have additional taxes withheld from your paycheck, either voluntarily or to cover other tax liabilities such as self-employment taxes, it can affect your after-tax income.

- Retirement Contributions: Contributions to retirement accounts such as a 401(k) or Traditional IRA can reduce your taxable income, potentially lowering your tax liability and increasing your after-tax income.

- Other Deductions and Adjustments: Various other deductions and adjustments to income, such as student loan interest deduction, tuition and fees deduction, or contributions to Health Savings Accounts (HSAs), can impact your taxable income and ultimately affect your after-tax income.

Overall, your monthly after-tax income is influenced by a complex interplay of factors related to your income, deductions, credits, and tax withholding preferences.

Understanding these factors and their implications can help you better manage your finances and plan for your financial future.

Next, let’s look at if $62,000 a year is a good salary.

Is $62,000 a Year a Good Salary?

Whether $62,000 a year is considered a good salary depends on various factors, including your location, cost of living, and personal financial goals. In some areas with a lower cost of living, $62,000 can provide a comfortable life. However, in more expensive cities, it may not stretch as far.

To determine if it’s sufficient for your needs, consider your monthly expenses, such as housing, utilities, transportation, groceries, and savings goals.

Additionally, factors like job benefits, opportunities for advancement, and job satisfaction play a significant role in evaluating the overall value of your wage.

Let’s take a look at how a $62,000 a year salary compares to others in the United States.

According to data from the US Census Bureau for 2022, the median income for Nonfamily households in the United States was approximately $45,440 – which means that half of all individuals earned more than this amount, and half earned less.

So, if you have a salary of $62,000, you have a salary that is in the top 50 percent of all earners in the United States. With annual pay of over $45,400, you are doing well and are part of a above-average group of earners in the United States.

How to Increase Your Income

When aiming to increase your income and bolster your financial resources, it’s crucial to consider a range of effective strategies:

- Skill Development: Invest in enhancing your existing skills or acquiring new ones that are highly valued in your industry. Keeping pace with evolving trends and technologies can significantly boost your marketability and earning potential.